.png)

Deal Signed, No Cash in the Bank! Guess the Missing Piece in Your SaaS Quote-to-Cash Process

| TL;DR - It's not enough to get the SaaS deal signed—you need to get paid. But most Quote-to-Cash (Q2C) workflows stop at the quote, leaving sales teams chasing cash for months. This post unpacks why signed quotes don't guarantee revenue, how sales teams try to patch the gap, and why embedded financing is the missing piece in your Q2C. Later, we'll also look at how Ratio Boost closes the loop—turning "Closed Won" into "Cash in Hand." |

🚨 The Challenge: Your Q2C Stack Is Fully Automated—But Cash Is Still Delayed

Modern SaaS leaders have poured tens of millions into Quote-to-Cash (Q2C) systems. No surprise, the market is projected to grow from $2.8B in 2024 to nearly $5.9B by 2033.

On paper, the promise is compelling: ⚡faster quotes, fewer errors, streamlined billing. But here's the catch—these platforms optimize internal workflows, not external outcomes. They assume buyers can pay. They do nothing to ensure the cash actually arrives.

💰 And without cash, revenue isn't real.

In fact—forget revenue. Without cash, can we honestly say these Q2C systems are delivering on what they claim?

❌ It's a false promise. Automation doesn't equal realization.

So, what's missing in the Q2C system is clear. Let's now take a closer look to understand what most SaaS companies are doing today to patch this cash gap—even with modern Q2C stacks in place.

Spoiler: Many of these workarounds might feel like progress—but they quietly backfire.

(Must-Know: 6 Signs Your Quote-to-Cash Is Broken—and How to Fix It to Unlock SaaS Growth)

Workarounds SaaS Sellers Use to Patch the Q2C Cash Gap

Despite Q2C automation, cash delays remain the norm.

Average Day Sale Outstanding (DSO) across SaaS? 54+ days—and rising. Even big names like Salesforce wait over four months to collect.

So, teams stop questioning the process.

They blame the subscription model… and assume delayed cash is just how SaaS works.

To cope, they create workarounds from offering heavy discounts on annual payments, selling signed contracts to opting for loans.

But these aren't solutions. They're short-term survival tactics.

And they quietly eat away at what you're trying to protect: margins, momentum, and control.

Let's break them down 👇

1. Offering Steep Discounts for Upfront Annual Payment

🧩 What it's used for:

To create urgency and lock in cash fast, particularly near quarter-end, by incentivizing buyers to prepay annual contracts. In a real-world email (see below), Salesforce reps offer "discounted pricing" and "year-end incentives" to encourage fast decisions before fiscal year-end. The message: act now, or miss out.

💡 Why it seems smart:

Reps offer 10–30% (and sometimes higher) discounts to overcome procurement objections or budget hesitations. It "greases the wheels" of high-ticket deals, especially when budgets are tight or fiscal deadlines loom.

⚠️ Why it backfires:

- Trains customers to wait for discounts—undermining full-price deals and renewal pricing.

- Shrinks margin and LTV: Heavily discounted customers have been shown to generate 30% lower lifetime value than non-discounted ones.

- Sets dangerous expectations: Discounts become normalized, making upsells and renewals harder to price fairly.

- Attracts churn-prone buyers: Price-sensitive customers are more likely to leave once discounts expire.

2. Capturing Payment Details Pre-Signature (CC/ACH Authorization)

🧩 What it's used for:

To trigger cash instantly upon contract close—by capturing credit card or ACH authorization before signature. This is mostly seen in SMB SaaS or Product-Led Growth (PLG) motions where deal sizes are small and speed matters.

💡 Why it seems smart:

- Collapses the gap between "Closed Won" and "Paid."

- Gives sales and finance visibility into real-time cash flow.

- Enables one-click activation and reduces ops friction for low-ticket deals.

⚠️ Why it backfires (in most B2B sales):

- Not scalable to enterprise or mid-market: 95% of business buyers prefer invoicing over card-based payment.

- Adds procurement friction: Larger buyers expect Purchase Orders (POs), terms, and finance reviews.

- Creates compliance risk: Storing payment details requires PCI-DSS systems and introduces liability.

- Doesn't change actual cash speed for vendors reliant on manual invoice processing.

In summary, forcing pre-signature payment info can introduce deal friction and isn't scalable outside of smaller SaaS contexts, often negating the intended cash-flow benefit.

3. Selling Invoices or Signed Contracts (Invoice Factoring)

🧩 What it's used for:

To turn signed deals or invoices into instant cash—before the buyer pays—by selling receivables to a third-party factoring firm.

💡 Why it seems smart:

With half of B2B invoices going overdue and SaaS DSOs averaging 54+ days, teams try to unlock working capital from what's already "booked." Factoring offers upfront liquidity—typically 70–90% of the invoice value within days—without waiting out Net-30/60/90 terms.

⚠️ Why it backfires:

- It's expensive: Factoring fees range from 1–5% per month, meaning a $100K invoice could cost you $10K+ annually just to access cash early.

- Recourse risk: In many arrangements, if the customer defaults, you still owe—creating liability despite paying fees.

- Customer experience risk: A third-party now chases your client for payment. That loss of control can strain trust, especially for high-touch SaaS relationships.

- Signal to market: Reliance on factoring may raise eyebrows with investors—signaling a cash flow fragility, not strength.

💡What We Recommend Instead:

Instead of paying high fees, losing control, or taking on recourse risk, smart SaaS teams are rethinking how they turn signed deals into capital.

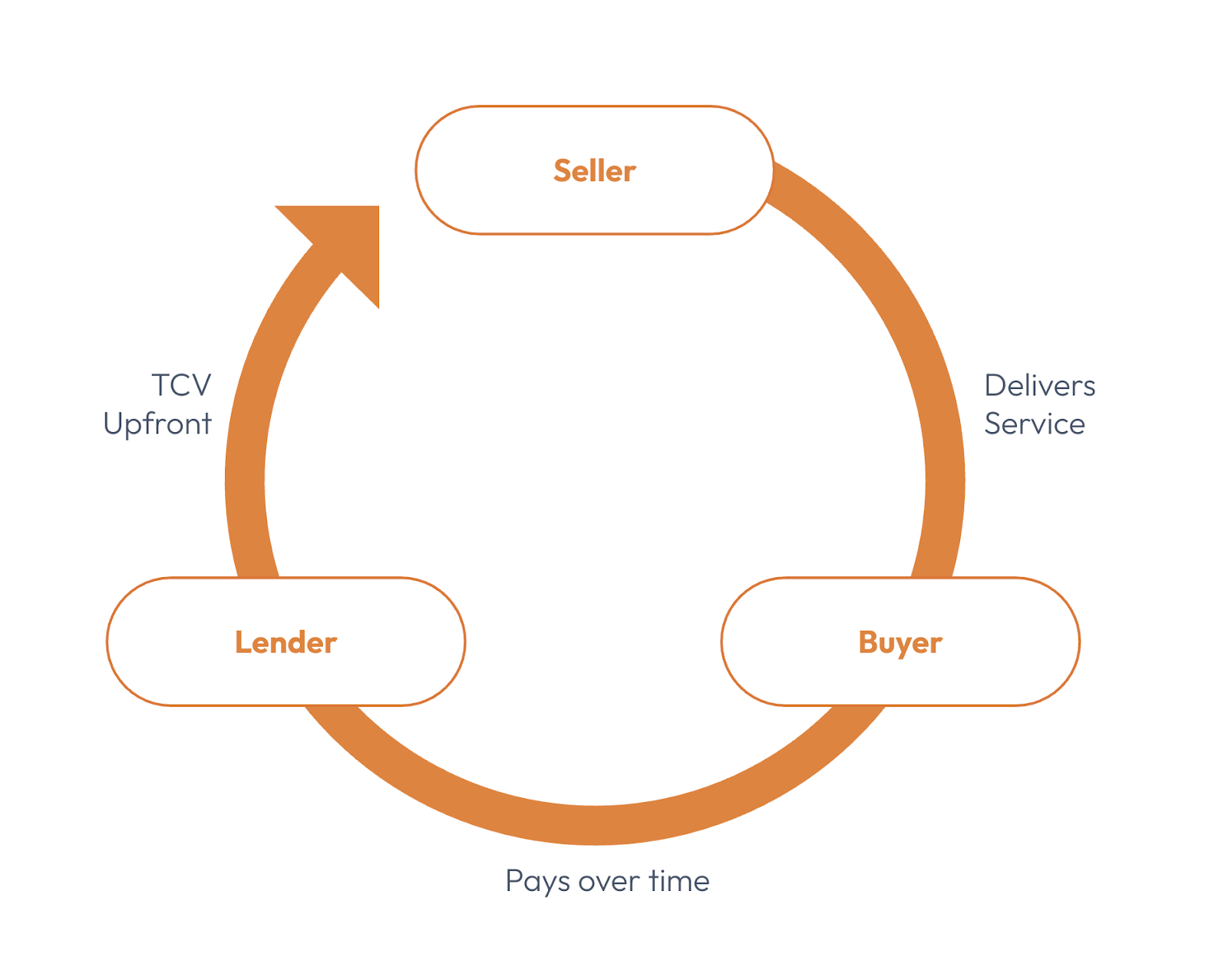

One option that's gaining traction: Ratio Trade. It's not factoring. It's True-Sale based financing—you convert signed contracts into upfront cash without taking on debt or chasing collections.

✅ Up to 80% of contract value on Day 1

✅ No recourse, no dilution, no repayment pressure

✅ You stay in control—Ratio never touches your customer relationship

💡 With Ratio Trade, your signed revenue powers your next move—hiring, ads, runway extension, you choose. If this sounds interesting, you can even calculate how much your annual deals would cost with Trade before committing.

4. Taking Short-Term Loans (Bridge Capital)

🧩 What it's used for:

To bridge the gap between booked revenue and delayed cash collection—especially when payroll, vendor payments, or growth plans can't wait.

💡 Why it seems smart:

Bridge loans, credit lines, or merchant cash advances offer immediate liquidity. When a big deal is signed, but cash hasn't arrived, this seems like a quick fix—particularly for founders avoiding dilution.

⚠️ Why it backfires:

- Interest eats your margin: With rising rates, loan costs have surged. In 2023, 58% of U.S. small businesses cited high interest as the biggest challenge in accessing credit. Even short-term loans can carry double-digit Annual Percentage Rates (APRs), quietly eroding your gross margin.

- Repayment pressure limits flexibility: Many loans require aggressive repayment schedules, with 6% of owners reporting terms were too tight. You may need to divert future cash toward debt service rather than reinvestment.

- Adds founder risk: Bridge loans often come with personal guarantees or collateral requirements, putting founders' assets on the line—especially in early-stage ventures.

- Creates cash illusion: You're not solving the root problem (slow payers); you're borrowing from tomorrow to survive today. Nearly 70% of U.S. entrepreneurs reported using debt or personal savings due to late-paying customers. That's not growth. That's survival.

5. Using Revenue-Based Financing (RBF)

🧩 What it's used for:

To access upfront capital without giving up equity—especially when traditional loans or delayed receivables leave a funding gap.

💡 Why it seems smart:

RBF flexes with revenue: repay a fixed amount (e.g., 1.2× to 1.5× of the funded capital) as a percentage of monthly income. No dilution, no fixed monthly burden, and it aligns with business performance.

⚠️ Why it backfires:

- Expensive capital: Even moderate RBF deals (e.g., $100K at 1.2× payback) can translate to 20–40%+ APR—significantly higher than venture debt or bank loans. If growth is fast, the effective rate spikes even more.

- Cash flow drag: A share of every dollar earned goes to the funder. That limits your ability to reinvest in sales, hiring, or products.

- Forecasting friction: Repayment timelines shift with revenue, making planning harder and introducing volatility into your cash model.

- Opportunity cost: You're surrendering a future revenue stream—often the very capital you need to grow.

📊 Fact: Analysts estimate startups pay 20–50% premiums on RBF advances over the repayment term. That's venture-level return pricing without investor support.

While these are some of the many ways SaaS sellers use to fund growth with a Q2C stack that doesn't advance cash upfront one thing is now clear: They're not the missing piece your Q2C system needs. They're short-term workarounds that quietly backfire.

That's why every B2B SaaS finance leader should seriously consider the true cost of short-term cash workarounds before relying on them.

Must Read: The Pros and Cons of Short-Term Financing Every SaaS Company Should Weigh Before Taking Cash

So, what's the real fix?

It's time to rethink your Q2C architecture—not just in terms of workflow automation but also cash flow intelligence.

Up next: How embedded financing can complete your quote-to-cash stack—and why Ratio Boost is the platform built for that transformation.

The Q2C Fix SaaS Teams Have Been Missing: Embedded Financing Built Into the Workflow

At this point, the pattern is clear: Sales teams aren't just following signed deals—they're chasing cash.

And despite having robust Q2C systems, in SaaS, where DSOs regularly stretch, even the most automated Q2C stacks leave finance teams plugging cash flow gaps with discounts, debt, or delayed investments.

Embedded Financing changes that.

Unlike traditional capital solutions that live outside your revenue infrastructure, embedded financing is integrated inside the quoting and contracting workflow—activating cash flow the moment a deal closes.

And no—it's not just a software integration. It requires a financing partner purpose-built for SaaS revenue models. That's exactly what Ratio Boost delivers.

Here's why it's the upgrade your revenue engine has been missing:

- 💸 Flexible Payment Terms for Buyers—Without Payment Delays for You

Ratio Boost embeds B2B Buy Now, Pay Later (BNPL) options directly into your quoting process. Buyers can split payments over time—monthly, quarterly, or deferred—but you still get paid upfront because Ratio underwrites and finances the deal immediately after signature.

- ⚡ Close Bigger Deals, Faster—Without Discounting

Remove price objections without sacrificing margins. With flexible terms embedded at the quote stage, buyers gain payment flexibility while you maintain deal velocity and full contract value—no need to offer discounts to close. - 🧠 Preserve Equity. Skip Debt.

Unlike traditional financing, Ratio Boost is non-dilutive and off-balance-sheet. There are no repayments, no covenants, and no personal guarantees—just clean cash flow to fund growth without giving up ownership or taking on liabilities. - 🔁 Recycle Capital, Fast

With upfront cash at deal close, you can reinvest immediately—whether into CAC-heavy channels, product expansion, or hiring. No more waiting out 12-month contracts just to access revenue you've already earned.

Ratio doesn't just fund contracts—it embeds directly into your existing sales stack and operates invisibly inside your Q2C motion.

Here's how the workflow looks like:

1️⃣ Access Ratio from your CRM or CPQ

Launch Ratio Boost natively within Salesforce, HubSpot, or any CPQ. No new systems. No workflow disruption.

2️⃣ Select or add a buyer

Pull buyer info directly from your CRM. Ratio handles background verification—no EINs or documents required.

3️⃣ Customize the payment plan

Offer 12, 24, or 36-month terms. Set payment cadence and choose who covers financing fees—your team, the buyer, or a split. A real-time preview shows what the buyer will see.

4️⃣ Submit for an instant credit check

Ratio underwrites most deals in seconds using AI. No forms. No manual effort.

5️⃣ Buyer reviews and signs

They receive a secure link, compare plans, and sign electronically. No emails or PDFs to manage.

6️⃣ Buyer activates payments

ACH setup is digital and instant. Ratio handles reminders and confirmations.

7️⃣ You receive up to 96% upfront

Once the agreement is finalized, Ratio wires funds—usually within 1–3 business days.

8️⃣ Ratio manages repayment

Automated invoicing, reminders, and collections—fully off your plate.

9️⃣ Track status in real-time

Sales, RevOps, and Finance can monitor everything from one dashboard.

🔟 Repeat deals instantly

No requalification. No re-entering details. Renewals and upsells happen in seconds.

SaaS platforms embedding financial services into their product experience have already proven the upside: a 70% uplift in monetization and a 97% increase in customer satisfaction, according to SaaStr.

Now is the time to capitalize on this advantage.

While there are many players in embedded finance today, only a few are purpose-built for B2B SaaS—and even fewer integrate seamlessly across the entire quote-to-cash workflow.

That's what makes Ratio different.

Let's break down why Ratio is the upgrade your workflow—and your working capital—needs.

Why Ratio Boost Is the Embedded Financing Engine Your Q2C Stack Has Been Missing

"Ratio's platform allows us to close deals in minutes. Sales & Finance love the all-in-one platform from proposal to cash. With Ratio we will 2–3x ARR this year, while collecting the cash upfront."

— Joe Brown, CEO @ DearDoc

When Joe Brown said this, he wasn't alone. From early-stage SaaS teams to scaling enterprise platforms, more and more companies are embedding Ratio Boost directly into their sales stack—not just to automate workflows but to unlock capital at the exact moment a deal is signed.

Here's what makes Ratio Boost the go-to financing engine (apart from what we have discussed above) for modern SaaS:

🔹 $411M Capital Pool, Purpose-Built for SaaS

This isn't a lending add-on. Ratio is backed by institutional capital facilities designed specifically to fund recurring revenue. That means high availability, fast deployment, and pricing aligned with SaaS business models—not bank covenants.

🔹 Real-Time Credit Decisions

Buyers are underwritten instantly using Ratio's proprietary risk engine. No docs. No delays. Your sales velocity stays high, even when buyers need flexibility.

🔹 Non-Dilutive, Risk-Off for Sellers

You get up to 96% of the contract value upfront. No debt. No recourse. No chasing payments. Ratio handles all collections—so your finance team can focus on strategy, not Account Receivables (AR).

Bottom line: You've automated your Q2C process. Now, it's time to fund it. Ratio Boost turns signed quotes into capital—with the infrastructure, intelligence, and scale SaaS companies need to win.

🔗 Get started today and see how it works for your Q2C workflow.

FAQs

1. Isn't Embedded Financing Just Another Form of Debt or Factoring?

Not at all. Traditional debt adds liability to your balance sheet. Factoring requires chasing invoices and often introduces a third party into your customer relationship.

Ratio is neither. It's a non-dilutive, risk-off, and true-sale financing model. You get paid upfront for the full contract value, Ratio takes on repayment risk, and your customer experience stays fully in your control. No loans. No liabilities. No collections burden.

2. Will Our Customers Know Ratio Is Involved? Does It Change Their Buying Experience?

Only if you want them to. Ratio Boost is seller-first and white-labeled—your brand stays front and center. Buyers see a secure, branded interface to select payment options and sign—no redirects, no external branding, no confusion.

Ratio manages credit and collections invisibly in the background while you retain full control of the customer relationship and renewal cycles.

3. How Much Lift Does This Q2C with Embedded Financing Add to Our Sales or Finance Team's Workflow?

Virtually none. Ratio Boost integrates natively into Salesforce, HubSpot, and major CPQs—so reps can offer financing with a single click. Finance teams get real-time visibility into deal flow and cash movement with zero added AR effort.

If your team can send a quote, they can activate financing—no new systems, no learning curve.

4. What Happens If a Customer Defaults After We've Already Been Paid by Ratio?

That's Ratio's problem—not yours. Once the deal is signed and funded, your business is no longer exposed to the risk of buyer default. You've already been paid. There's no clawback, no recourse, and no balance sheet impact. That's what makes Ratio a risk-off model—ideal for SaaS teams focused on scale, not collections.

.png)