%20to%20SMB%20Clients%20(1).png)

5 Benefits of Offering B2B BNPL(Buy Now, Pay Later) to SMB Clients

The Challenge: You want to tap into the Small and Midsize Business (SMB) segment—but your SaaS pricing and standard payment terms are pushing them away.

SMBs (often called SMEs) make up 99% of all businesses—and the B2B segment among them represents a trillion-dollar market. If you've built a high-value product for modern companies, you can't afford to overlook this segment.

But SMBs buy differently: lean teams, short planning cycles, and tight cash flow.

So when you ask them to pay upfront for a high-ticket product?

- Deals stall in procurement

- Budget objections kill urgency

- Discounts become the only way to keep deals alive

You're not protecting revenue—you're slowing it down.

So think about it:

How many qualified SMBs are dropping off simply because they can't pay all at once? Probably more than you realize.

What if they could pay on their own terms while you still get paid upfront? That's exactly what B2B Buy Now, Pay Later (BNPL)—done right with a partner like Ratio—makes possible.

Here are five reasons it pays off.

Five Benefits of Offering B2B BNPL to SMB Clients with a BNPL Partner Like Ratio

In a recent post, we broke down the benefits of offering B2B BNPL to enterprise clients. But those dynamics shift when selling to SMBs—because SMBs operate under a different financial and decision-making structure.

Enterprise sales get stuck in long processes—procurement, legal, and multiple approvals.

SMBs move quickly. But they're more fragile. One upfront payment request can shut the deal down.

That's why BNPL doesn't just work for SMBs—it works even better. And with a partner like Ratio, it becomes a real growth tool.

Here are five big benefits sellers unlock when offering BNPL via Ratio to SMB clients:

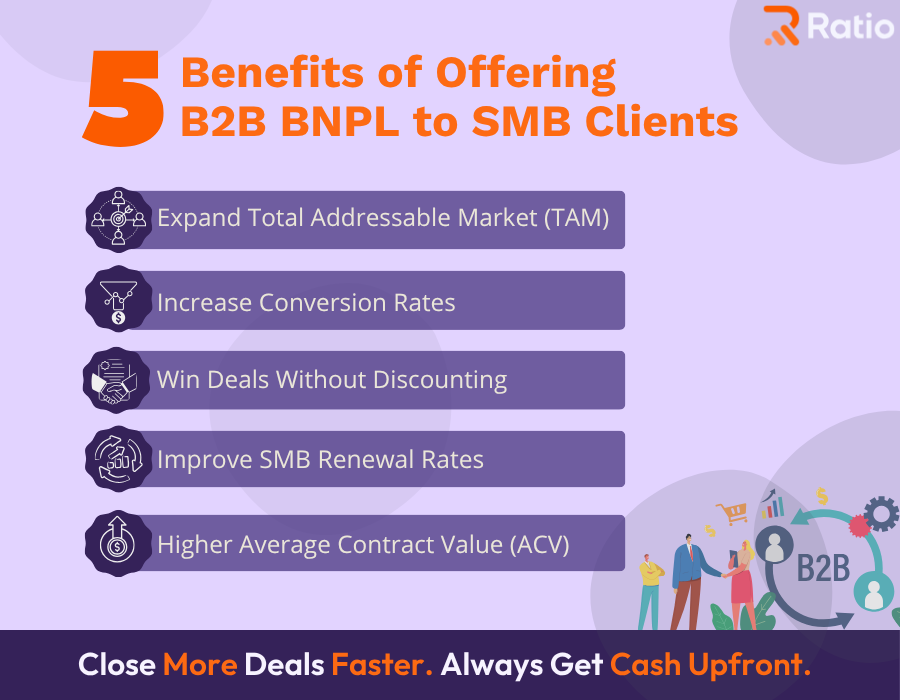

- Expand Total Addressable Market (TAM) With Flexible Payments

- Increase Conversion Rates by Eliminating Cash Flow as a Barrier

- Win Deals Without Discounting or Compromising Margins

- Drive Higher Average Contract Value (ACV) Through Affordability-Led Upselling

- Improve SMB Renewal Rates by Reducing Financial Friction

Let's take a closer look at each:

1. Expand Total Addressable Market (TAM) With Flexible Payments

What's happening:

SaaS vendors unintentionally exclude a massive segment of the SMB market simply by requiring full upfront payments. While these buyers want enterprise-grade tools, tight cash flow or planning cycles make high-commitment purchases feel inaccessible. They self-select out not because of poor fit, but because of payment structure. The result: your TAM stays smaller than it should be.

What BNPL Unlocks:

BNPL removes the structural barrier blocking access to cash-constrained SMBs. By offering flexible terms at the point of sale, you make your product financially viable for an entirely new class of buyers, expanding your market and increasing the top-of-funnel.

Ratio Advantage:

Embedded BNPL directly in your CRM or CPQ — reps can offer flexible payment plans within the quote flow, no redirects or external portals.

Instant buyer underwriting — Ratio uses EIN-based identity and AI-powered credit models to assess eligibility in seconds.

Configurable financing control — sellers can absorb, split, or pass on the financing cost and still receive 100% of the contract value upfront with zero repayment risk.

Example:

A Fleet Management Tech Provider (FM) wanted to reach smaller logistics firms—but most couldn't pay upfront. After implementing Ratio Boost, FM offered embedded BNPL at checkout. This eliminated financing delays, made pricing manageable for smaller buyers, and preserved FM's capital. The result: 25% growth in conversions and revenue uplifted with zero balance sheet exposure.

2. Increase Conversions by Eliminating Delays in Buyer Financing

What's happening:

When faced with large upfront payments, SMBs often pursue external financing, including SBA 7(a) loans to cover software costs. But approvals can take 60–90 days and involve heavy paperwork. Most SMBs won't wait. They either delay the decision or abandon it entirely. You're not losing deals due to lack of demand — you're losing them to inaccessible capital.

What BNPL Unlocks:

BNPL eliminates the need for slow, external financing. Buyers get access to monthly or deferred payment plans inside the quote flow enabling them to act while urgency is high and friction is low.

Ratio Advantage:

Embedded BNPL experience — buyers view and select payment plans inside your quote flow without being redirected to third-party lenders.

Real-time approvals — Ratio delivers financing decisions in seconds, backed by a ~$411M capital pool — so you get paid upfront every time.

Example:

By embedding Ratio's BNPL at the point of sale, DearDoc eliminated payment delays that stalled deals — increasing close rates by 20-30% and converting interest into same-day signatures.

3. Win Deals Without Heavy Discounting or Compromising Margins

What's happening:

Sales reps often default to discounting when buyers push back on price. We have seen discounts of 10–30% are now perceived as routine especially on annual contracts. But this quickly eats into margin.

Take a $10,000 SaaS deal with a 40% margin. A 20% discount means you're giving up $2,000, but your profit drops by half, from $4,000 to $2,000.

The damage doesn't stop there: discounts reset buyer expectations, encourage repeated negotiations, and attract customers who churn once the "deal" expires.

What BNPL Unlocks:

BNPL gives buyers a way to afford full-price contracts. Instead of offering discounts, sellers present structured payment plans that make high-value deals manageable — preserving pricing integrity while removing the cost barrier.

Ratio Advantage:

Multi-year deal support — Close larger, longer-term contracts by offering structured payment schedules, eliminating the need for discounts.

Discount guardrails — Ratio enforces pre-configured discounting rules, ensuring that only strategic deals receive concessions. All others default to BNPL, preserving price integrity across your pipeline.

Risk-based flexibility — Enable sellers to automatically extend more favorable terms to creditworthy buyers while limiting flexibility for higher-risk counterparts.

4. Drive Higher Average Contract Value (ACV) Through Affordability-Led Upselling

What's happening:

When making purchasing decisions, SMBs often downgrade to lower-tier plans. Not because your premium offering lacks value but because they can't justify the upfront expense. Even highly motivated buyers choose "just enough for now" over "what they really need," shrinking deal size at the last minute.

What BNPL Unlocks:

BNPL enables reps to upsell higher-tier plans, longer terms, or more seats by spreading the cost over time. Buyers say yes to more value — not less — because they're no longer blocked by a single large upfront payment. As a result, sellers grow ACV without changing price or pushing finance to make exceptions.

Ratio Advantage:

Plan-level upsell enablement — Ratio lets reps present flexible financing at the feature, seat, or term level — enabling buyers to say yes to premium tiers they'd otherwise skip.

Quote-stage scenario selling — Reps can show side-by-side monthly payments for different plans, making upgrades feel incremental and budget-friendly.

No need for pre-approval — Ratio underwrites buyers in real-time, so reps can upsell on the spot — without waiting for CFO or finance sign-off.

If upsell-ready accounts are still downsizing at renewal, this guide unpacks how to reduce downsells and maximize SaaS renewals.

5. Improve SMB Renewal Rates by Reducing Financial Friction

What's happening:

SMB churn at renewal is high upto a 60% revenue rate. It rarely signals dissatisfaction but is driven by operational friction and value misalignment.

- Buyers feel overcharged for features they don't use — with no usage summaries, renewals feel blind.

- Annual lump-sum payments trigger hesitation, even when ROI is clear.

- With no finance team, a founder juggling 10 roles can easily defer forms and approvals.

- With so many SaaS alternatives, switching seems painless — especially when competitors offer "switch and save" pricing like this one.

- Surprise increases without justification create pushback, especially if the pricing model already feels opaque.

In short: SMBs don't churn for one reason. They churn because renewal feels like a decision — not a continuation.

What BNPL Unlocks:

Instead of forcing SMBs to re-justify a large upfront payment, it lets them continue on flexible terms that match how they operate — steady cash flow, no budget spikes, no re-approvals.

Want more deeper tactics to reduce churn at the renewal stage? Here are 5 proven ways to protect SaaS renewals and reduce churn friction.

Ratio Advantage:

Renewal-stage BNPL — Offer flexible payment plans at the point of renewal, not just at new sales, keeping continuity friction-free.

Stored buyer profiles — Ratio retains prior underwriting data, so renewal offers require no requalification or rework.

Upfront revenue, again — Even on renewed terms, you get paid in full at renewal while your SMB customer pays over time.

While the benefits of offering B2B BNPL to SMB clients are clear, not all BNPL solutions are created equal.

Not sure what to look for? Focus on these five critical factors when choosing a B2B BNPL provider for SaaS sales.

To fully unlock BNPL potential, you need a partner built for the fast-moving, resource-constrained world of SMB buying — one that embeds seamlessly into your quote-to-cash motion and turns payment friction into revenue acceleration.

That's what Ratio Boost was built for.

We've already seen how Ratio drives conversions, renewals, and margin protection. Now, let's take a final look at what makes it the best BNPL platform for high-ticket B2B SaaS.

What Makes Ratio the Trusted B2B BNPL Choice for High-Ticket SMB Sales

"Ratio fills a need in the Robotics-as-a-Service industry that no one else does. By providing flexibility to our customers, we have landed deals that we would have lost to customer budget constraints."

— Nohtal Partansky, Founder & CEO, Sorting Robotics

Many high-intent buyers don't say "no" — they say "not now" because they can't manage the upfront cost. That's exactly the challenge Sorting Robotics faced.

Ratio Boost changed that. It turned stalled deals into signed contracts — helping them convert budget objections into wins.

Along with the core BNPL benefits we've already covered, Ratio adds even more:

AI-powered pricing & approvals — Instantly tailor terms using real-time buyer intent signals and historical patterns with Co-Pilot (coming soon). It provides a deal probability score and next-best actions to maximize close rates.

Fewer tools, faster sales — Quoting, payments, and collections in one seamless platform with a B2C-style checkout experience.

Choosing the right BNPL partner isn't about who offers payment plans. It's about who understands how you sell — and builds for the way your buyers buy.

Ready to see what Ratio can unlock in your pipeline? Book a demo and turn buyer friction into closed revenue.

FAQs

1. What to Look for When Selecting a B2B BNPL Partner?

Choose a provider that offers:

- Flexible payment options (monthly, quarterly, custom)

- Fast approval processes (ideally real-time)

- Seamless CRM and billing integration

- Robust credit risk assessment (AI-enhanced if possible)

- Built-in collections management

These features ensure better cash flow, higher deal velocity, and reduced operational friction. You can read the full breakdown👉 here.

2. Who are the Top B2B BNPL Providers in the USA?

Leading providers include:

- Ratio – Embedded BNPL with full quote-to-cash software

- Capchase – Financing-first with BNPL and revenue-based funding

- Vartana – Checkout-driven sales financing for enterprise tech

- Tranch – BNPL for SaaS/service contracts (2–12 month terms)

- Resolve – Net 30/60/90 solutions, spun out from Affirm

- TreviPay – Enterprise trade credit with deep ERP integration

Each specializes in different workflows—select based on your sales model. Compare top B2B BNPL providers

3. Is BNPL Only Useful for Net-New Deals, or Can It Be Applied to Renewals and Expansions?

BNPL can and should be used across the full customer lifecycle. Ratio supports embedded financing for renewals, upsells, and multi-year contract expansions — allowing buyers to commit to longer terms without upfront cash spikes. It helps sellers retain revenue continuity while improving expansion ACV.

Want to deepen your playbook? Explore five ways to reduce downselling during SaaS renewals.

4. Can We Control Who Sees BNPL Offers — or Is It Presented to All Prospects by Default?

Yes, you can customize eligibility rules. Ratio allows sellers to define parameters based on buyer profile, deal size, or risk tier — so reps can selectively extend BNPL offers or default to upfront terms for certain segments. This ensures BNPL is a strategic lever, not a blanket policy.

.png)