Watch our Masterclass |

Reduce Cash Flow & Working Capital Issues Without Pissing Off Your Sales Team!

Recording Available

11 AM PT / 2 PM ET

Every SaaS operator we've talked to hits the same wall: the deal closes, the contract is signed — and then the process falls apart. Quote-to-cash is supposed to connect quoting, billing, payments, and collections into one coherent motion. In practice, legacy tools treat these as disconnected steps, and that gap costs real revenue. This guide covers where those systems fall short, what to look for instead, and how to evaluate your options in 2026. If you want to close the gap between signature and cash without rebuilding your stack, Ratio Boost is a must.

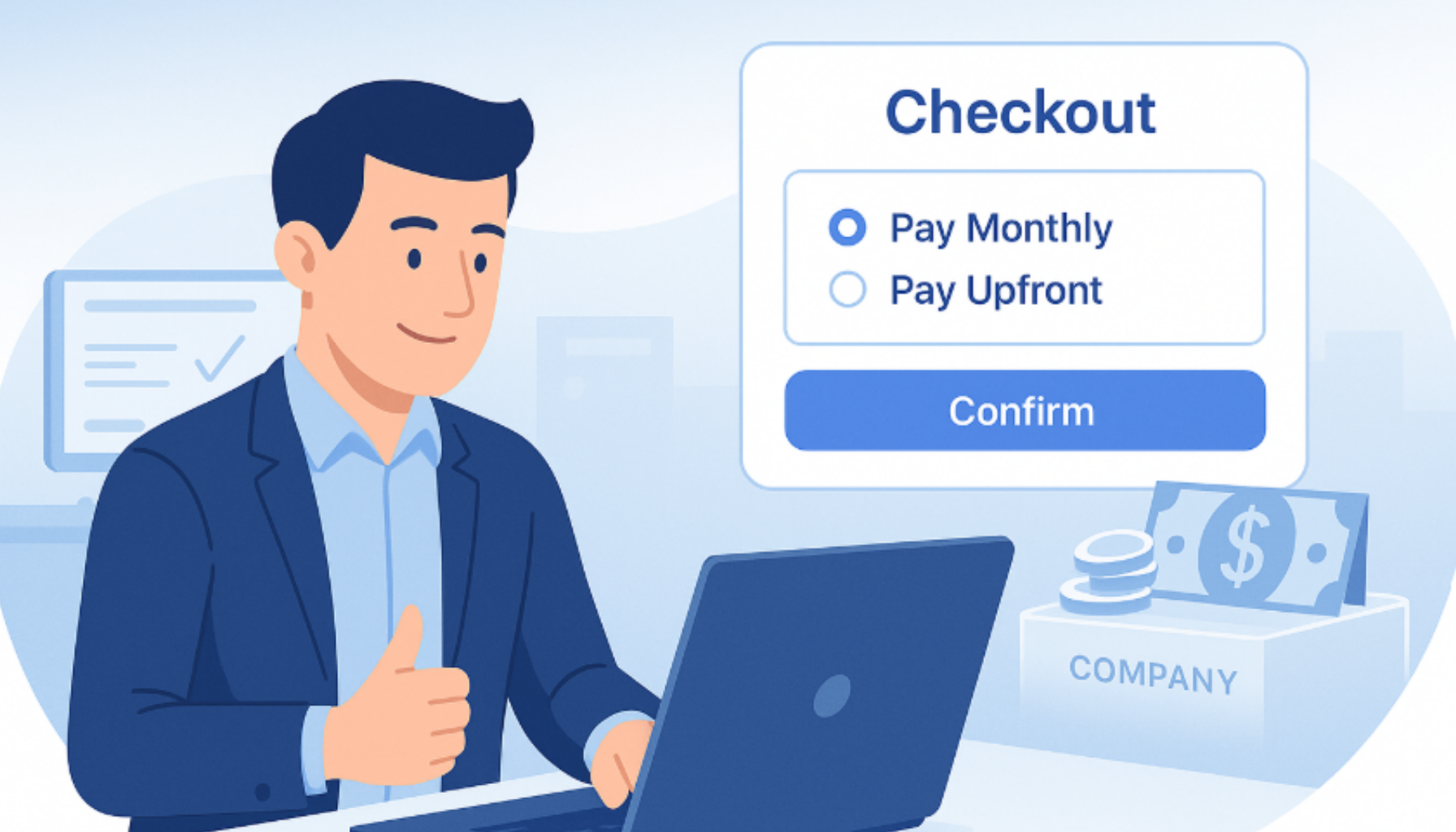

Stripe has served you well, but as your SaaS deals grow more complex with longer terms, milestone billing, and cash flow constraints, you may be searching for Stripe billing alternatives. In this post, we’ll explore whether you really need to switch or if extending Stripe with tools like Ratio for offering buyer-friendly terms, quote-to-cash automation, and Day-1 cash, is the smarter path forward.

Most quote-to-cash software speeds up quoting, but not cash in hand. This post ranks five Q2C solutions by revenue impact: which ones help you close faster, protect ACV, and get paid upfront without discounting or delays.

.png)

If you’re searching for high-rated CPQ software for quote-to-cash, this guide breaks down the top tools B2B SaaS teams trust most. You’ll also see why many are now switching to Ratio to close deals faster and collect revenue without delays.

SaaS companies lose revenue when deals stall over payment friction. Embedded finance platforms let B2B companies offer flexible terms while collecting cash upfront, boosting conversions, removing discount pressure, and accelerating growth. This guide compares the top embedded finance platforms built for B2B SaaS in 2025 and how to choose the one that best fits your sales motion.

.png)

The Challenge: Revenue’s up, but you can’t fund what’s next. Sales are closing. ARR is rising. But when it’s time to hire, expand, or invest, cash isn’t there yet. In SaaS, working capital isn’t just a finance metric. It’s your ability to fund growth, stay flexible, and absorb shocks. At its core, it answers: Do we have enough cash on hand to make our next move?

.png)

🚨 The Hidden Risk: SaaS sellers are quietly financing their buyers—and it’s draining their growth. To close deals, teams offer net terms, monthly billing, or deferred starts. Buyers get flexibility. But sellers? They deliver value now and wait —sometimes months—to get paid in full. It feels like sales enablement, but it’s something else: funding customer affordability out of your own cash flow. Without structure, it erodes margins, slows collections, and increases risk. 🕒 CAC payback stretches 💸 Discounts pile up 📉 Churn, defaults, and forecasting issues grow

.png)

The Challenge: You’re growing, you’ve invested in tools—and yet, everything feels harder to manage. As your company grows, so do the tools. Sales adds a quoting platform to move faster. Finance brings in a billing system to manage revenue. RevOps implements dashboards to track performance. Each team chooses what works for them. In fact, teams use an average of 10 tools to close deals. But none of it works together.

.png)

The Challenge: Your Q2C Stack Is Fully Automated—But Cash Is Still Delayed. Modern SaaS leaders have poured tens of millions into Quote-to-Cash (Q2C) systems. No surprise, the market is projected to grow from $2.8B in 2024 to nearly $5.9B by 2033. On paper, the promise is compelling: faster quotes, fewer errors, streamlined billing. But here’s the catch—these platforms optimize internal workflows, not external outcomes. They assume buyers can pay. They do nothing to ensure the cash actually arrives. And without cash, revenue isn’t real.

The Challenge: You close the deal—but cash doesn’t follow. Revenue gets booked, but collecting it happens later—often manually, with no clear owner. As volume grows, so do aging invoices, missed follow-ups, and stalled cash flow. This isn’t just inefficient—it’s expensive. A 2025 benchmark found that 22.2% of fast-growing SaaS companies lose over 10% of ARR to late payments and defaults—not churn, but customers under contract. That gap between revenue and realization isn’t just a finance issue. It’s a growth constraint.

.png)

The Hidden Growth Barrier: SaaS revenue is growing—but cash isn't keeping up. Sales teams are closing more deals—offering discounts and flexible payment terms to win logos. But Finance is left asking: “How much of that ARR is actually usable cash—right now?” Too often, the answer is: not much.

%20to%20SMB%20Clients%20(1).png)

The Challenge: You want to tap into the Small and Midsize Business (SMB) segment—but your SaaS pricing and standard payment terms are pushing them away. SMBs (often called SMEs) make up 99% of all businesses—and the B2B segment among them represents a trillion-dollar market. If you’ve built a high-value product for modern companies, you can’t afford to overlook this segment. But SMBs buy differently: lean teams, short planning cycles, and tight cash flow.

The Challenge: You believe upfront payments are good for your SaaS business—until you realize they’re costing you deals. SaaS companies love upfront payments. All cash in, risk out. What's not to like? But in B2B SaaS—where the average deal can run from $4,800 to $220,000—how you ask to get paid can speed things up or stop them cold. Asking for full payment upfront often leads to the following: CFO pushback on lump-sum invoices, procurement demands for installments, or sales discounts just to keep the deal alive

Over the past few years, I have observed a major shift unfolding in B2B payments—driven by what can only be described as the consumerization of enterprise purchasing. While the global B2B payments market is projected to surpass $124 trillion by 2028, the systems behind these transactions remain outdated. Rigid terms, clunky approvals, and manual workflows persist—even as buyer expectations evolve rapidly.

Challenge: SaaS deals should be closing, but somehow they’re just... not. You’ve seen it happen: The demo lands. The buyer’s excited. Everything points to a quick close. Then... silence. Sure, sometimes buyers hesitate. But often, even motivated buyers get stuck — bogged down in finance approvals, rigid contracts, and inflexible payment terms. It’s the broken quote-to-cash (Q2C) process quietly killing deals that should have been won.

B2B BNPL helps SaaS and technology sellers get paid upfront while buyers pay over time. It reduces friction in sales, protects margins, and eliminates credit risk. This guide covers what B2B BNPL is, how it works, common pitfalls, provider comparisons, and how to embed it into your revenue stack.

Challenge: Why Do SaaS Deals Keep Slipping Late in the Cycle? Procurement slowdowns. Budget objections. Delayed approvals. Even great SaaS sales teams lose high-intent deals to timing friction and payment constraints. The business impact is real: 🔻 Delayed revenue recognition 📉 Missed quarterly targets 💸 Forecast volatility and uneven cash flow 🧩 Pipeline bloat from deals stuck in limbo Flexible payment terms help, but most solutions still leave sellers waiting to get paid and exposed to collection risk.

%20(2).png)

Why B2B BNPL is suddenly on every SaaS leader's radar: flexible payment terms used to slow deals down. Now they help close them faster. Feels like a brain shock, right? But here’s the thing - SaaS sales teams want to: close faster, preserve runway, and avoid giving discounts. B2B Buy Now Pay Later (BNPL) is solving all three and is, therefore, showing up in more sales cycles, from self-serve onboarding to six-figure contracts.

.png)

Challenge: Why Does Your SaaS Sales Process Feel Stuck? Sales reps spend just 30% of their time selling. The rest is lost to chasing approvals and tweaking quotes. Negotiations drag the sales cycles, demoralize the reps, and often lead to: ❌Lost deals ❌Unpredictable revenue ❌Cash flow problems The right CPQ simplifies quoting, streamlines approvals, aligns pricing with buyer expectations, and speeds up deal closures.

.png)

The Challenge: Using a CPQ but not seeing the expected boost in deal closure rates and velocity. CPQ was meant to fix stalled deals. So why aren’t you closing more? You’ve optimized pricing, automated quotes, and streamlined approvals. But deals still get stuck. Not because of the quoting process but because of what happens after the quote is sent.

Clawing back commissions is like awarding a trophy—then snatching it away. A deal closes, a rep gets paid, but if the customer cancels, defaults, renegotiates, churns, or commits fraud, revenue drops, commissions are clawed back, and the sales team’s morale takes a hit. While 53% of SaaS companies use clawbacks to recover lost revenue, clawbacks are frustrating for the sales teams. Moreover, frequent clawbacks are a symptom of deeper inefficiencies in the sales processes.

Think your cash burn is under control? Investors may not agree. In today’s market, efficiency is the new growth and SaaS CEOs who can’t prove it are being left behind. In fact, in a survey, 82% of investors highlighted efficiency as their top priority. Burn multiple has become the SaaS industry’s ultimate test of operational discipline. It’s not just about growing your ARR anymore—it’s about how much growth you deliver for every dollar spent.

.png)

In my years working with B2B companies, I’ve seen the push to offer flexible payment terms (like monthly options for SaaS or 60-90-day cycles for enterprise contracts) to close deals faster. While it seems like a win-win—clients appreciate the flexibility, and sales teams close more contracts—without proper management, it can quietly drain resources and disrupt operations.

.png)

The economic downturn has hit businesses very hard. And economists say there's the threat of a global recession on the horizon. To survive, many companies are being forced to keep a tight lid on their budgets and limit upfront cash payments for tools. So, SaaS vendors are considering adopting financial solutions that help accommodate their customers' financial difficulties. This is important, especially for small and medium SaaS companies that lack the advantages—a competitive moat and massive marketing and sales teams—big companies have that enable them to insist on annual and multiyear subscriptions.

.png)

Venture capital funding has dropped 53% year-over-year, and banks have tightened lending policies, increasing interest rates amid financial downturns and bank failures. On top of this, customers are favoring subscription payments over upfront bulk payments, limiting company cash flow. However, companies need to raise funds to spur growth. This article will explore the pros and cons of funding options and how to optimize capital structure.

.png)

In Q2 2023, venture funding took a sharp dive, dropping 18% quarter over quarter and 49% year over year. This downturn has made alternative financing options like revenue-based financing (RBF) and true sale-based financing (TBF) more appealing than ever. These options offer quick approvals and access to capital, providing a viable alternative to traditional venture funding.

.png)

Price serves as the critical deciding factor for consumers in 80% of markets, making it an essential element to consider in your SaaS business model. High prices may discourage prospects, while low prices could raise doubts about your product's quality. Sadly, these pricing perceptions often shift focus away from the robust return on investment that a well-executed SaaS solution can provide. For SaaS vendors, striking the right pricing balance is critical: overprice and lose potential deals, or underprice and risk sustainability. One study reveals that pricing can swing profitability by 12.7%, making it more impactful than other growth strategies.

.png)

The average customer acquisition cost (CAC) for B2B software-as-a-service (SaaS) companies is $239, but it can be as high as $1,450. So, companies prioritize customer retention to lower the CAC and maintain a healthy customer lifetime value (CLV) to CAC1 ratio. Downselling becomes a go-to strategy in this pursuit. It helps you retain churn-prone customers—especially when they're churning due to the high cost or underutilization of the ongoing subscription plan. However, downselling isn’t a smart strategy when it comes to revenue.

.png)

Many tech enterprises favor annual billing for SaaS, drawn by its cash flow benefits. However, upfront payments can deter budget-conscious buyers. And the immediate alternative—annual agreements with monthly payments—pose risks like non-payments and cancellations. In response, SaaS enterprises often resort to discounting. While it does enable the SaaS sales teams to close more deals, it also chips away at long-term revenue and profit margins.

%20(1).png)

Discounting to overcome pricing objections and stretching payment terms to close deals—classic sales tactics, right? Every salesperson has relied on these at some point to hit targets. But here’s the problem: while these strategies might get deals across the finish line, they often come at a hidden cost to your business. Margins shrink, cash flow suffers, and you’re left dealing with collections headaches, the risk of client defaults, and the fallout from weak underwriting decisions.

.png)

Not all B2B BNPL providers are created equal. Some can take too long to approve a BNPL request. Others have AI-powered underwriting to give instant approvals. Some have clunky technology that slows down your sales. Others are so seamless they make B2B BNPL feel like B2C. Some can’t scale with your business as you grow. Others have deep pockets to support you every step of the way. Some do the bare minimum. Others are constantly innovating to give you actionable sales insights. Choosing the right B2B BNPL (Buy Now, Pay Later) provider isn’t easy.

Are you offering payment flexibility to your customers all on your own? It’s time to rethink. When you offer it on your own, you bear the burden of delayed payments, operational strain, and financial risk. However, when you offer payment flexibility with a B2B BNPL partner, you get upfront capital, streamlined operations, and reduced risk.

.png)

Closing a B2B deal isn't a sprint—it's a marathon, often spanning three to six months to cross the finish line. B2B buyers meticulously scrutinize every detail to ensure they’re making a wise investment. For large enterprises, there is a complex approval chain for expensive purchases, whereas startups and SMBs battle budget limits. Despite your sales team's best efforts, deals can stall if prospects find better offers, or they may shift priorities if they can't afford the products at closing time.

With the average customer acquisition cost (CAC) for SaaS businesses ranging from $76 to $519 per customer, it has become a critical metric for SaaS entrepreneurs. Yet, many find themselves grappling with the challenge of balancing cost-effectiveness with sustainable growth. While conventional methods like optimizing marketing spend or refining targeting strategies may offer initial relief, relying solely on these approaches can inadvertently constrain scalability and inhibit long-term profitability.

In Q3 2023, venture capital investment in fintech companies dropped 36% to $6 billion, a blow to B2B SaaS entrepreneurs amid tighter venture financing and stricter banking rules. The surge in subscription models further tightens cash flow. Businesses are adapting to diverse financing approaches.

The SaaS industry is worth approximately $195 billion, and the US SaaS industry is set to grow by over 2x by 2025. Conclusion? The SaaS market is on fire! But with that comes several challenges — lack of funding, poor product adoption, etc. — the reason why 90% of SaaS start-ups fail to achieve the desired level of success.

.png)

As a SaaS Value Added Reseller, you're no stranger to the financial challenges of the industry. Issues such as managing cash flow, tackling high costs of acquiring customers, and scaling effectively in a fiercely competitive market are all part of the job. The risk of vendor lock-in also affects your finances, highlighting the need for financial agility.

Are you tired of chasing delayed payments and worrying about your company's cash flow? If so, you're not alone. 55% of all B2B invoiced sales are overdue in the United States at the moment, while an average 9% of all credit-based B2B sales are affected by bad debts. These figures highlight the urgent need for businesses to reconsider their approach to payments. Late B2B payments and increasing debt severely impact a company's financial health, jeopardizing its existence.

BCC Research reveals a striking growth in the Revenue-Based Financing (RBF) market: from $2.3 billion in 2022 to an anticipated $154 billion by 2030. This surge is hardly surprising, considering how revenue-based loans are revolutionizing the way businesses finance their expansion. These loans present a groundbreaking approach: repayment terms are linked to a business's recurring revenue.

Gartner predicts a whopping $232 billion in global SaaS spending by 2024. Yet, only some SaaS firms consistently hit growth rates above 30-40%. How do they do this? It’s due to the 'Rule of 40'. This rule demonstrates that a SaaS firm's revenue growth and free cash flow margin, when combined, should at least be 40%. So, a company growing at 30% should show a 10% free cash flow margin.

McKinsey predicts a whopping 3000% growth in subscription e-commerce by 2025. However, as businesses offer subscription-based payments, it can lead to cash flow challenges. In response to this growing demand, vendors seek solutions that allow payment flexibility without disrupting their sales processes, all while maintaining a steady cash flow.

The global revenue-based financing market size is projected to reach over $42MM by 2027. And why not? Recurring Revenue Financing (RRF) is, after all, a compelling alternative for businesses looking to secure quick growth capital without the drawbacks of traditional financing.

SaaS companies facing high burn rates and limited working capital should aim to target a 12- to 18-month runway to effectively manage their accelerated cash consumption. To maintain financial stability, businesses often turn to traditional funding options such as venture capital or loans, which can be fiercely competitive and come with strings attached.

In today's dynamic B2B financial landscape, offering flexible payment options isn't just a convenience—it's a necessity. The reason is the surging demand for subscription-based payments. However, while offering payment flexibility opens doors to improved client relationships and cash flow management, it isn't without challenges. A mishap in introducing or managing these flexible payment solutions can potentially eat into as much as 10% of a business’s monthly revenue.

As e-commerce flourishes, B2B Buy Now, Pay Later (BNPL) isn't just trending; it's transforming how major merchants operate. A 2022 McKinsey report noted that a solid 65% of B2B companies are now all-in on online sales. Taking cues from the B2C world, the surge in B2B BNPL services is evident.

Capchase is a prominent Revenue-Based Financing (RBF) platform providing businesses with upfront capital based on recurring revenues. It converts predictable MRR into ARR, providing companies with fast, flexible funding upfront without debt or dilution.

Many SaaS founders and CEOs focus more on driving rapid growth than they do on their long-term prospects — because after all, they assume, if you’re growing fast enough then the capital will keep flowing in and you’ll soon find your way to a strong exit. Growth is the key to success.

It’s a tough time to be in the software business. That’s partly because investors aren’t opening their wallets quite as readily as they used to. But things aren’t just hard because investors are feeling a bit jittery.

Usage-based SaaS pricing is all the rage — but while customers love the idea of only paying for the cloud services they actually consume, that can all too easily turn into sticker shock when customers get their first bill and realize they used more than they’d anticipated. That’s a real problem for SaaS companies.

When you’re selling SaaS software, clearly it’s important to figure out what your product is really worth. One way to do that is to think about how much value you deliver, compare it to the competition, and set prices accordingly. That’s the way most vendors operate, and it has served the industry pretty well.