Top 5 Flexible Financing Options SaaS Companies Can Choose From in 2025

The Challenge: You're scaling, but your monetization model delays cash, while your capital needs are immediate.

You've built recurring revenue. But monthly billing, net terms, and deferred starts slow down actual cash collection. Buyers want flexibility. You offer it—because it helps close deals.

But while revenue grows, cash lags behind. Customer Acquisition Cost (CAC), Go-To-Market (GTM) spend, and headcount hit early—before the money lands.

You could raise another equity round, but that dilutes ownership. You could go to a bank, but most don’t underwrite ARR—and the process is slow, rigid, and paperwork-heavy.

That’s why leading SaaS teams are turning to flexible financing: capital solutions structured around ARR and contracts, designed to fund growth without dilution or fixed repayment pressure.

In this post, we’ll break down five flexible financing options SaaS companies can choose from in 2025. And why quote-to-cash with embedded financing may be the most scalable model you’re not using yet.

Five Flexible Financing Options Every Scaling SaaS Business Should Know

We’ve previously broken down four SaaS financing options for growth-stage startups—a guide for capital that moves with your sales motion.

But if you're scaling fast, you need financing that adapts to how your SaaS business actually works.

That’s where flexible financing comes in: capital solutions built around recurring revenue, contract value, and customer payment behavior.

So what are your options?

These are seven flexible financing options every scaling SaaS team should have on their radar:

- Quote-to-Cash with Embedded Financing

- Revenue-Based Financing (RBF)

- ARR (Annual Recurring Revenue) Financing / Contract Advances

- Subscription Line of Credit

- Venture Debt with SaaS-Friendly Terms

- Receivables Financing / Invoice Factoring

- SaaS Term Loans from Fintech Lenders

Let’s explore each option and the trade-offs that come with it. That way, you can choose the right fit for your SaaS growth.

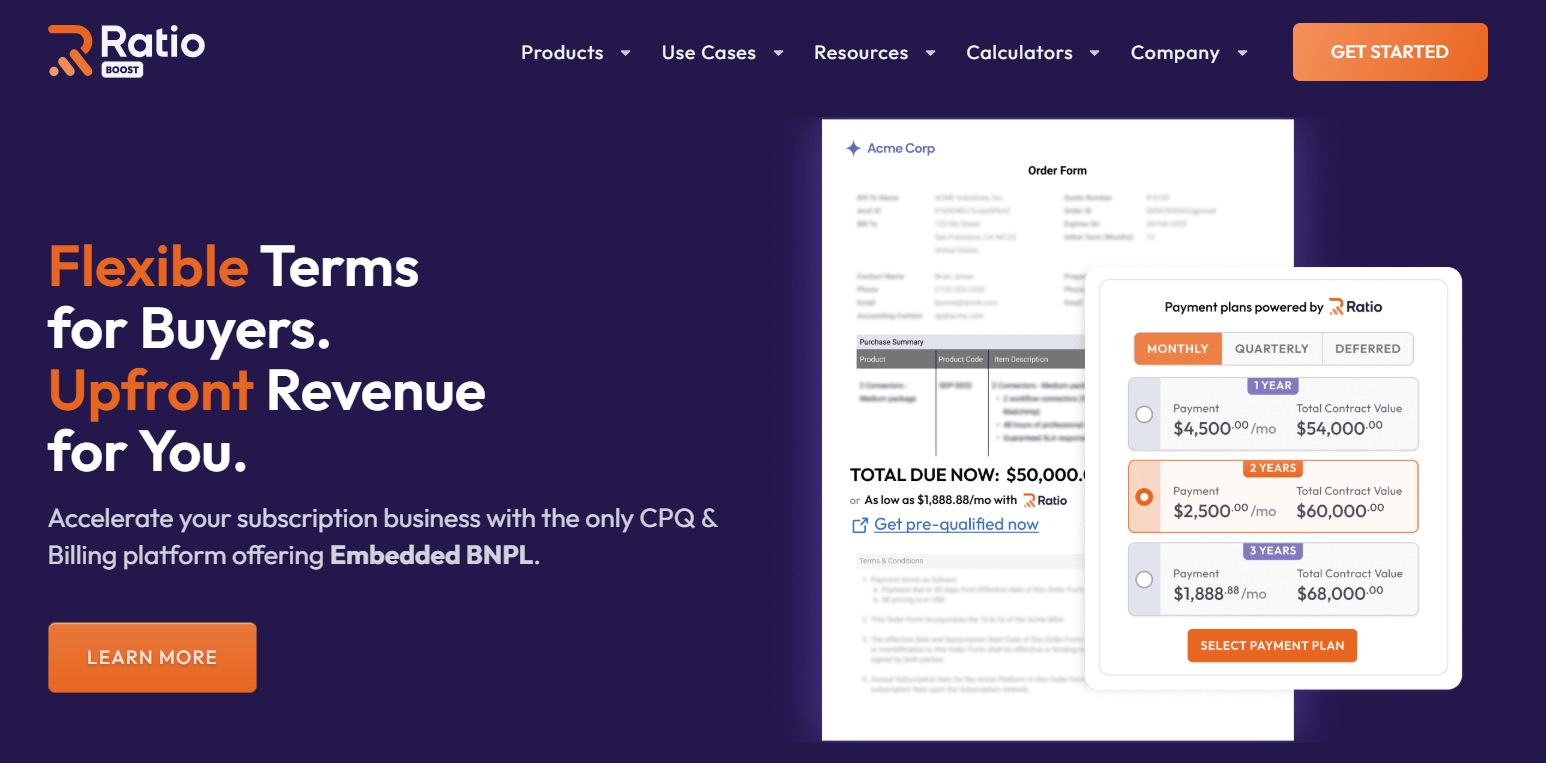

#1. Quote-to-Cash (Q2C) with Embedded Financing

Quote-to-Cash with embedded financing is a go-to-market-aligned capital strategy that allows SaaS companies to get paid upfront on annual or multi-year contracts. No more waiting for payment, offering discounts, or changing billing terms.

Unlike legacy financing approaches that kick in after a deal closes, Q2C with embedded financing integrates directly into your quoting process. When a buyer receives a quote, they’re offered flexible payment options—monthly, quarterly, or deferred—right at the point of sale. A third-party financier (like Ratio Boost) underwrites the buyer in real time, pays the seller up to 96% of the total contract value within days, and then collects from the buyer over time.

It’s financing that mirrors how SaaS sales actually work: fast-moving, relationship-driven, and margin-conscious.

And it’s increasingly becoming the default approach for SaaS teams who want to scale without sacrificing liquidity, ownership, or sales velocity.

How it works

Here’s how it looks inside a modern sales motion:

Step 1: Your sales rep generates a deal quote using your existing CPQ, CRM, or proposal software.

Step 2: Embedded financing adds flexible payment terms directly to the quote. The buyer sees monthly, quarterly, or custom options side-by-side.

Step 3: Ratio runs an instant background check on the buyer—using EIN, payment history, and other signals—to approve financing within seconds.

Step 4: The buyer selects their payment plan, signs the agreement, and completes a brief payment setup (via e-signature + ACH).

Step 5: Ratio wires you the full contract value (minus a financing fee) within 1–3 business days.

Step 6: You’re out of the loop from there. Ratio handles invoicing, collections, and reminders according to the buyer’s chosen plan.

Step 7: Your RevOps team can track health, collections, and renewals—all within your CRM.

To know in much detail, you can find here in our step-by-step guide for how Ratio’s B2B BNPL actually works.

Example

Let’s say you close a $72,000 annual SaaS contract with an enterprise client. The buyer prefers to pay monthly—$6,000/month—but your team needs capital upfront to fund GTM campaigns.

With Q2C embedded financing, the buyer selects “$6,000/month for 12 months” from the quote. Ratio approves the buyer in seconds. And there you receive $69,120 within 48 hours (minus a 4% fee charged by Ratio). And now Ratio collects from the buyer monthly and handles all billing touchpoints.

The result? You preserve your pricing, reduce deal friction, and turn bookings into working capital—without dilution, repayment schedules, or balance sheet risk.

Learn how Quote-to-Cash with embedded financing drives revenue impact in our guide to the Top 5 Q2C platforms for B2B SaaS →

Pros (Why SaaS Teams Choose It)

- Accelerates cash conversion without changing your billing model

Instead of waiting 30–90 days (or more) for enterprise payments, you convert signed deals into cash within days—even if you bill monthly or offer net terms. This shortens your cash cycle without changing how you sell, letting you reinvest into CAC, onboarding, or GTM without slowing down.

Type image caption here (optional)

- Preserves equity and financial flexibility

This isn’t a loan. There’s no repayment liability, no equity dilution, and no balance sheet complexity. It’s non-dilutive, off-balance-sheet capital that keeps founders in control—and finance teams agile.

- Reduces discounting pressure

When buyers push back on upfront payments, sellers often resort to discounts. With embedded financing, you keep your price point and give buyers the flexibility they want. That preserves both top-line revenue and gross margin.

- Streamlines procurement and shortens sales cycles

Procurement redlines and CFO approvals often stall deals. With embedded financing inside the quote, buyers get instant term flexibility—without escalations or contract rewrites. That reduces friction and closes deals faster.

- Built for GTM and RevOps scale

Ratio integrates directly into Salesforce, HubSpot, and CPQ platforms. That means no new tools, no manual approvals, and full visibility into deal status, collections, and renewals—all from your existing CRM.

- Control over who pays the financing fee

You decide whether to absorb the fee, pass it to the buyer, or split it. That flexibility helps protect your margin while still closing the deal.

Cons (What to watch for)

- Not all buyers will qualify: While most enterprise and mid-market buyers are approved quickly, early-stage or high-risk companies may not pass underwriting. Make sure reps are prepared with a fallback option (like internal net terms or milestone billing) to keep momentum.

- Requires light CRM or CPQ setup: To embed financing directly in your quote flow, you’ll need to configure it in your CRM or CPQ. Providers like Ratio offer plug-and-play integrations but plan a little DevOps or RevOps bandwidth upfront, especially if your team uses custom quoting logic.

- Best fit for fixed-term contracts: Embedded financing works best with annual or multi-year contracts where terms and billing are predictable. If your SaaS product is heavily usage-based or milestone-driven, you may need to customize the structure for ideal results.

Top Quote-to-Cash (Q2C) with Embedded Financing Providers

While several Q2C platforms support B2B SaaS workflows, Ratio Boost stands out as the only one with built-in embedded financing capabilities—designed to turn quotes into upfront cash without disrupting your sales motion.

Want to see how it compares?

Check out our blog: Top 5 Quote-to-Cash Software Platforms for B2B SaaS in 2025 (Ranked by Revenue Impact) to explore why Ratio Boost is the most revenue-aligned Q2C option for scaling SaaS teams.

#2. Revenue-Based Financing (RBF)

Revenue-Based Financing (RBF) is a non-dilutive, flexible financing option where a SaaS company receives upfront funding in exchange for a fixed percentage of future monthly revenue. Repayments automatically scale with performance—higher when revenue is strong, lower when it’s not.

There are no fixed repayments, equity dilution, or collateral requirements. Instead, you repay until a predefined cap (typically 1.2x–1.6x the original amount) is met.

This model works best for SaaS businesses with healthy MRR, low churn, and predictable revenue flow—especially when raising equity or qualifying for debt isn’t ideal.

How it works

- You connect your billing or revenue data (e.g., Stripe, QuickBooks, ChartMogul) to the RBF platform.

- A capital provider evaluates your MRR, churn, burn rate, and runway.

- Upon approval, you receive a lump-sum advance (e.g., $500K).

- A fixed % of monthly revenue (e.g., 5–10%) is automatically repaid until you hit the agreed cap (e.g., 1.5x = $750K).

- Once the cap is reached, the repayment ends—clean exit.

Pros (Why SaaS Teams Choose It)

- Non-dilutive growth capital with repayment flexibility

No equity loss, no fixed-term stress. You retain control while aligning repayments to revenue flow. - Built for recurring revenue businesses

MRR-based underwriting makes RBF accessible to SaaS startups that are post-product-market fit but pre-profit. - Great fit for CAC-heavy GTM initiatives

Use it to fund paid acquisition, sales hiring, or onboarding—where the payback period is short and predictable. - Scales with your momentum

As revenue increases, so does repayment speed—allowing you to recycle capital faster and unlock additional tranches.

Cons (What to watch for)

- Cost compounds with scale

A 1.5x repayment cap can equate to a 30–50% effective APR, depending on your growth. Fast-growing teams may repay the obligation faster—at a higher cost. - Always-on revenue cut

Until fully repaid, a share of your revenue is diverted monthly. That can limit reinvestment capacity as you scale. - May not fit unpredictable revenue models

If your cash flow is irregular or driven by large one-off contracts, the repayment structure may misalign with actual inflows. - Terms vary across providers

Some add hidden fees, minimums, or revenue floors. Always calculate the true cost—not just the cap.

Top Revenue-Based Financing Providers

- Capchase – RBF funding with real-time revenue tracking and flexible advance limits.

- Pipe – Offers trading of future recurring revenue for upfront cash.

- Founderpath – Built specifically for bootstrapped SaaS founders seeking non-dilutive capital.

- Arc – Combines banking services with revenue-based advances for SaaS companies.

- Lighter Capital – Longtime RBF provider with flexible options for growth-stage tech startups.

#3. ARR (Annual Recurring Revenue) Financing / Contract Advances

ARR Financing converts your signed contracts (or entire customer base) into upfront non-dilutive capital—without needing to wait for invoicing, collections, or renewal.

The model is designed around your contracted revenue, not your bank balance or past receipts.

For example, if you have a signed 3-year, $600K SaaS deal, a contract advance provider (like Ratio Trade) may advance you up to $500K of that value upfront, depending on risk and term length.

This helps you pull cash forward and reinvest it immediately. While still billing your customers as usual.

How it works

- You connect your CRM, CPQ, or billing system to the platform (e.g., Salesforce, HubSpot, Stripe).

- The provider analyzes your customer contracts, billing cadence, and churn risk.

- Based on your ARR strength, you get an upfront capital offer—often 70–90% of the total contract value.

- You continue collecting revenue from your customers as usual, while the provider is repaid over time from those inflows.

- The advance is off-balance-sheet, with flexible repayment terms tied to your cash inflows (or set schedules, depending on the provider).

Pros (Why SaaS Teams Choose It)

- Turns booked ARR into instant cash

Convert committed—but unpaid—contract value into upfront working capital to reinvest in GTM, hiring, or expansion without waiting on billing cycles. - Non-dilutive and off-balance-sheet

There’s no equity dilution, and it doesn't show up as debt. That keeps your cap table clean and financials flexible. - Works well with annual or multi-year billing

If your sales motion includes 12–36 month contracts, you can unlock significant cash in advance—often faster and cheaper than venture or revenue-based financing. - Flexible repayment aligned with revenue inflows

You don’t need to change your pricing model or billing cadence. Ratio structures repayments around how and when your customers actually pay. - Preserves customer experience

Buyers still pay you directly. No factoring, no third-party involvement in collections—just a seamless backend capital unlock.

Cons (What to watch for)

- Strong contract quality required

Advance offers are based on deal size, customer creditworthiness, retention history, and billing terms. The stronger your ARR health, the more you can unlock. - Not ideal for usage-based or monthly contracts

If your revenue is heavily consumption-based or short-term, this model may require more customization or deliver lower advance rates. - Repayment structures vary

Some providers require rigid repayments regardless of collection. Be sure to assess whether repayment aligns with your billing flow. - Not a replacement for pipeline funding

Contract advances only work on signed deals—not pipeline or forecasted opportunities. Use this in tandem with other tools like Ratio Boost if you need pre-signature capital.

Top Contract Advance Providers

- Ratio Trade – Purpose-built for B2B SaaS teams, with real-time CRM and billing integrations. Offers up to 90% contract value upfront and flexible structures that align with your ARR and billing model.

→ Explore how Ratio Trade unlocks ARR liquidity without debt or dilution → - Capchase – Offers advance capital against contracted revenue with flexible repayment. Strong for later-stage SaaS companies.

- Arc – Combines banking tools and contract advances for SaaS, with customizable repayment options.

- Founderpath – Known for fast turnaround and founder-friendly tools, especially for bootstrapped startups.

#4. Subscription Line of Credit

A Subscription Line of Credit (SaaS Line of Credit) is a revolving credit facility specifically structured for subscription-based businesses. It allows B2B SaaS companies to draw capital against their recurring revenue base without needing to sell equity or pledge hard assets.

Unlike traditional credit lines (which rely on fixed collateral), this model underwrites your Monthly Recurring Revenue (MRR), churn, and growth trends to offer flexible access to capital that scales as you grow.

How it works

- You apply with revenue metrics (MRR, net retention, CAC, churn, etc.)

- A provider evaluates your data and approves a credit limit (e.g., up to 4–6x of MRR)

- You draw funds when needed—no fixed disbursement

- Interest accrues only on the drawn amount (typical rates range 10–18%)

- You repay and reuse the credit line as needed—just like a business credit card

Pros (Why SaaS Teams Choose It)

- On-demand capital that scales with ARR

Unlike a one-time loan or advance, this line of credit grows as your MRR increases—ensuring long-term financing agility. - Pay only for what you use

There’s no obligation to draw the full amount. You can pull funds only when necessary, which keeps financing costs efficient. - Flexible and recurring

Perfect for recurring needs like hiring cycles, product sprints, or temporary working capital gaps—without reapplying or renegotiating terms. - Built around SaaS metrics

No need for hard collateral or profitability. Approval is based on your subscription health—not your balance sheet. - Preserve equity and control

No dilution or board involvement. You maintain ownership while getting the liquidity needed to scale.

Cons (What to watch for)

- Requires strong revenue data

Lenders look for consistent MRR, low churn, and decent unit economics. Early-stage or volatile startups may struggle to qualify. - Interest adds up over time

Rates can be high (10–18% APR), especially if the drawn amount isn’t paid back quickly. - Shorter terms for repayment

While revolving, these lines may include periodic renewals or performance-based reviews that affect continued access. - Not ideal for long-term capital needs

If you need funds for an extended runway or multi-year expansion, a term loan or equity round may be more appropriate.

Top Subscription Line of Credit Providers

- SaaS Capital – Pioneer in ARR-backed credit lines. Offers up to 6x MRR to qualifying SaaS businesses.

- Founderpath – Offers recurring revenue lines of credit, ideal for bootstrapped or early-stage SaaS.

- Lighter Capital – Provides both revenue-based financing and subscription-based lines of credit with flexible terms.

- Tamarack Technology – Known for customized subscription finance facilities for B2B SaaS with strong revenue profiles.

#5. Venture Debt with SaaS-Friendly Terms

Venture Debt is a structured loan offered alongside or just after an equity raise, providing additional non-dilutive capital to extend runway, accelerate growth, or bridge to your next funding round.

When structured specifically for SaaS companies, venture debt includes longer interest-only periods, covenant-light agreements, and repayment flexibility that aligns better with subscription revenue models.

Unlike traditional loans, venture debt is designed to complement venture capital, not replace it. It’s offered based on your last equity raise (typically 20–40% of your last round) and your current revenue strength.

It’s best suited for growth-stage SaaS companies that have raised institutional capital and want to avoid immediate dilution while preserving optionality for future equity rounds.

How it works

- You raise a VC round (e.g., $5M Series A).

- A venture debt provider offers you $1–2M in non-dilutive debt, repayable over 3–5 years.

- You draw funds upfront or in milestones (e.g., after hitting $2M ARR).

- You pay interest monthly, followed by principal + interest after an initial interest-only period.

- Some providers may include warrants (minor equity sweeteners) or light covenants.

Pros (Why SaaS Teams Choose It)

- Extends runway without immediate dilution

You avoid giving up more equity when valuations are lower and preserve cap table strength for later rounds. - Ideal for post-raise expansion

When paired with equity, it boosts your war chest for hiring, GTM, or acquisitions—without overfunding through equity alone. - Predictable, structured repayment

Unlike RBF or revenue-tied models, you know exactly how much and when you’ll repay—simplifying finance planning. - Backed by strong venture confidence

Because lenders bet on your latest raise and cap table strength, this financing signals market confidence.

Cons (What to watch for)

- Requires a recent VC raise

If you haven’t raised institutional capital recently, you may not qualify—or the terms will be less favorable. - Fixed repayment, regardless of performance

You’re expected to repay on a set schedule, even if growth slows. That creates pressure if your metrics stall. - Can include warrants or fees

Some lenders request small equity kickers (typically 0.5–1.5%)—which, while minor, still dilute over time. - Covenants may limit flexibility

While SaaS-friendly, some loans include clauses around revenue targets, burn rate, or default triggers.

Top Venture Debt Providers for SaaS

- SVB (Silicon Valley Bank) – Longtime leader in SaaS-focused venture debt, now stabilized and serving tech with tailored terms.

- Hercules Capital – Large-scale lender supporting growth-stage SaaS with custom venture debt facilities.

- TriplePoint Capital – Offers flexible structures and tranches that sync with SaaS growth curves.

- Horizon Technology Finance – Known for funding post-Series A and B SaaS companies with non-dilutive capital.

- Stifel Venture Lending – A strong alternative for SaaS firms looking for high-limit, low-dilution financing.

By now, you’ve seen how the top five flexible financing options compare. Each has strengths depending on your stage, revenue model, and capital needs.

But if you’re a B2B SaaS founder focused on shortening sales cycles, protecting margins, and unlocking cash without changing how you sell. There’s one model built specifically for that: Quote-to-Cash with Embedded Financing.

It’s flexible for buyers, upfront for you, and embedded in the moment the deal is signed.

At the forefront of this shift is Ratio Boost, the only Q2C platform designed to turn SaaS quotes into working capital, instantly.

And now let’s see why more SaaS teams are choosing Ratio Boost to scale smarter.

Why Ratio Boost Is the Most Scalable, Flexible Financing Option for B2B SaaS Teams

In 2025, Ratio saw 800%+ YoY growth—driven by SaaS companies shifting from delayed cash cycles to a Quote-to-Cash model that delivers capital at the point of sale, not after.

And now, it’s not just monthly or annual plans. Sellers can offer custom payment terms—monthly, quarterly, milestone-based—while still getting paid upfront.

Here’s what sets Ratio Boost apart:

- $411M+ capital pool ready to deploy

Whether it’s 10 contracts or 10,000, you’ll always have cash coverage—without touching your balance sheet. - AI-powered underwriting & deal structuring

Get instant buyer approvals and optimal payment terms recommended based on real-time pipeline data—protecting ACV while speeding up close. - CRM + CPQ-native integrations

No new tools. No workarounds. Ratio embeds into your Salesforce, HubSpot, or quoting flow—automating approvals, billing, and collections. - Coming Soon: AI Co-Pilot for Sellers

Get deal intelligence in real-time—like price sensitivity, buyer risk, and next-best action—based on what’s actually in your pipeline.

Just ask DearDoc, a fast-scaling healthtech SaaS.

They reduced financing approval time from days to under 45 minutes, lifted conversion rates by 20–30%, and consolidated quoting, contracting, and collections into one flow.

“Ratio Boost helped us consolidate quoting, contracting, payment, and collections into a single flow—and close faster as a result.”

— Joe Brown, CEO, DearDoc

And they’re not alone. Taxwell (Drake Software) used Ratio to align with SMB buyer cash flow, eliminate approval delays, and unify sales and finance workflows. Without needing a separate CPQ system.

When you're scaling SaaS, flexibility isn't a feature; it's a funding strategy. And Ratio Boost is how you operationalize it.

Book a Demo to see how Boost fits your motion.

Disclaimer: The information in this blog is intended for general informational purposes only and reflects research, data, and insights sourced from Ratio’s platform performance, customer case studies (including DearDoc), and publicly available competitor analysis. Financial structures, approval times, and performance outcomes may vary by business profile, creditworthiness, and market conditions. This content does not constitute financial, legal, or investment advice. Readers are encouraged to consult their internal finance teams and conduct due diligence before making financing decisions.

FAQs

1. Will Flexible Financing Replace Upfront Payments Entirely?

Not necessarily. Many SaaS teams still offer upfront pricing, but flexible terms like Q2C with embedded financing convert more deals without discounts. The key is to offer options inside the quote.

For a strategic take, see Pros and Cons of Upfront Payments for B2B Companies.

2. Can Flexible Financing Work for SMB or Non-Enterprise Buyers?

Yes. Modern embedded financing platforms like Ratio Boost now underwrite SMBs in seconds and offer tailored term options. This makes it a high-converting flexible financing option even in mid-market SaaS.

For a closer look at SMB use cases, see 5 Benefits of Offering B2B BNPL to SMB Clients.

3. How Can I Layer Flexible Financing With Other Non-Dilutive Capital Tools?

Quote-to-cash financing can be layered with revenue-based financing or contract advances as long as you don’t overextend repayment streams. The key is intentional stacking.

.png)