Weigh the Pros and Cons of Upfront Payments for B2B SaaS Companies Before You Demand It

| TL;DR - Upfront payments help B2B SaaS companies get cash in faster but they also slow down deals, create buyer friction, and lead to discounting. This article breaks down the real trade-offs of asking for full payment upfront—and shows how to get paid upfront while still giving buyers flexible terms. |

The Challenge: You believe upfront payments are good for your SaaS business—until you realize they're costing you deals.

SaaS companies love upfront payments. All cash in, risk out. What's not to like?

But in B2B SaaS—where the average deal can run from $4,800 to $220,000—how you ask to get paid can speed things up or stop them cold.

Asking for full payment upfront often leads to the following:

❌ CFO pushback on lump-sum invoices

❌ Procurement demands for installments

❌ Sales discounts just to keep the deal alive

Upfront terms are meant to protect revenue—but today's buyers expect payment flexibility in B2B SaaS without straining their own cash flow. So think clearly about:

📉 Is the cost of insisting on upfront payments worth it?

📈 Or is there a smarter way to get paid upfront—without killing the deal momentum

Get the answers as we discuss the pros and cons of upfront payments and how B2B SaaS companies can unlock more revenue faster.

Let's start here👇

💡What is Upfront Payment & How Does it Work for B2B SaaS Companies?

In B2B SaaS, upfront payments mean a buyer pays most—or all—of the contract value at the start of the term. No installments. No monthly billing. Full cash on day one.

It's most common with annual or multi-year deals, where the vendor invoices for 12+ months in full. Many sellers won't activate onboarding, licenses, or implementation until payment is received.

To the seller, it's clean:

- Revenue secured

- No collections

- Cash in before cost out

This approach often appeals to finance and sales leaders who want predictability, simplicity, and control.

But while upfront payments offer real advantages, they also demand trade-offs to get the deals signed and hurt your business in hidden ways.

Let's look at what sellers actually gain when they ask for payment upfront.

Pros of Upfront Payments (Understand from the Seller's Perspective)

When SaaS sellers receive lump-sum upfront payments instead of monthly installments, they unlock working capital they can put straight into product, marketing, or hiring.

That's more than relief; it's control. No more chasing invoices. No cash flow anxiety. No waiting for value to trickle in.

And it's not just for early-stage companies. Any B2B SaaS seller offering upfront terms can gain real operational leverage.

Here's what upfront payment unlocks when it works:

#1. Improved Cash Flow

🛠️ How it works:

Upfront payment means the full contract value lands in your account on Day 1. No chasing monthly invoices. No payment schedules. Just cash—immediately.

🔓 What it unlocks:

You can invest that capital right away in what matters: hiring, product, marketing, or sales. It gives you control over how—and how fast—you grow.

💡 Why it matters:

According to OpenView's recent SaaS Benchmarks, companies under $1M ARR burn around $50K per month. One upfront deal at that level? That could fund a full month of operations—maybe more if you're lean on spending.

#2. Reduced Customer Non-Payment Risk

🛠️ How it works:

When a buyer pays upfront, the deal is done—payment collected, risk closed. You bypass monthly invoicing or net-60 payment delays. No more chasing invoices. No collection follow-ups.

🔓 What it unlocks:

You avoid the pain of invoicing delays, defaults, or failed payments.

There's no need to underwrite customer credit, assess risk profiles, or hope finance clears it later. Your team can stay focused on growth—not collections.

💡 Why it matters:

Late payments are a significant issue in B2B transactions. 64% of SMBs deal with late payments, and over a quarter delay paying their own vendors because of it. Upfront payments eliminate that entire domino effect.

#3. Increased Operational Simplicity

🛠️ How it works:

Collecting full payment upfront removes the need for monthly billing cycles. No fragmented invoices. No chasing payments across multiple periods. Just one clean transaction per contract.

🔓 What it unlocks:

That simplifies a few key things:

- No recurring invoice reminders

- Easier cash application

- Cleaner reporting for cash-based revenue tracking

It won't replace the whole quote-to-cash workflow, but it will lighten the load.

💡 Why it matters:

Many SaaS teams still manually track collections and reconciliation, causing delays and errors during closing. Upfront payments don't solve everything, but they cut down on repetitive finance tasks that otherwise slow down ops.

#4. Higher Customer Commitment

🛠️ How it works:

When a buyer pays upfront—especially for a full year or more—they've already made a serious investment. That decision doesn't just transfer cash. It signals intent.

🔓 What it unlocks:

Prepaid customers are more likely to fully implement your product. They're less likely to churn early. And they're more responsive to onboarding and success outreach—because they've already paid.

It's behavioral psychology at work: people are more committed to what they've already spent money on.

💡Why it matters:

An industry research found that charging early, i.e., financial commitment, increases follow-through, especially in B2B onboarding and SaaS adoption phases.

Translates to: prepaid customers are stickier.

#5. Favorable Unit Economics

🛠️ How it works:

When you collect full payment upfront, you recover Customer Acquisition Cost (CAC) faster. Instead of waiting 6–12 months for payback, your unit economics shift in your favor from Day

🔓 What it unlocks:

- Shorter CAC payback periods

- Higher gross margins (you're not fronting delivery)

- Stronger cash position on the balance sheet

And there's a bonus: many vendors offer discounts for annual prepayment.

By getting paid upfront, you can do the same with your own expenses—from hosting and tools to software and services.

💡Why it matters:

Early-stage SaaS companies that shorten CAC payback can reinvest revenue faster without diluting equity or taking on debt.

According to OpenView's benchmarks, best-in-class SaaS companies achieve CAC payback in under 12 months. Upfront payments make that timeline much easier to hit.

At this point, upfront payments seem like a clear win—and in many ways, they are. But when the buyer's expectations don't match your terms, even the best intentions can create friction.

If your customer wants flexibility and you insist on full prepayment, that tension can slow deals or kill them entirely.

Let's break down where upfront payments can backfire and where sellers often get stuck.

Cons of Upfront Payments

Now that we've covered the pros, it's just as important to look at the other side before making any decisions. Let's walk through the downsides of requiring upfront payments and where they can create more friction than value.

#1. Lower Conversion Rates

🛠️ How it works:

Upfront payment shifts the financial risk to the buyer before any value is experienced. For many clients, especially SMBs or first-time buyers, that's a tough leap.

From their perspective: "Why should I commit thousands before I know it works?" It feels risky, especially for smaller teams trying to preserve the runway or operate within tight quarterly budgets.

The real hesitation? They're unsure the product will deliver the value promised—and paying upfront makes that uncertainty feel even riskier.

⚠️ What it affects:

Buyers delay approvals. Deals slow down. And some walk away entirely—choosing competitors who offer installment plans, deferred billing, or pay-as-you-go models.

Even great-fit customers can hesitate—not because your product lacks value, but because they haven't experienced it yet. And with your terms, the risk lands on them too early.

#2. Reliance on Discounting

🛠️ How it works:

When sellers sense friction from the upfront ask, they often reach for a quick fix: discounting. "If you pay today, we'll knock off 15%."

But the discount isn't tied to real risk, value, or customer behavior. It's simply a tactic to soften the financial blow.

⚠️ What it affects:

You erode your pricing integrity, shrink your ACV, and set a dangerous precedent: buyers start to expect deals—not because of volume or timing, but because your terms feel heavy.

And once you discount to close, it's hard to reclaim that margin at renewal.

#3. Misaligned Incentives

🛠️ How it works:

In a prepaid model, the sales reps get the reward upfront—regardless of how the onboarding, adoption, or long-term usage plays out.

That's great for short-term revenue, but it misaligns incentives: your team has been paid, but the buyer hasn't seen value yet.

⚠️ What it affects:

It weakens accountability and jeopardizes long-term retention. If onboarding is clunky or value takes months to show up, the buyer may feel buyer's remorse—even before they've truly started.

Must-Read: What SaaS Sales Leaders Need to Know About Clawback Commissions — and How to Minimize Them

#4. Strained Buyer Relationships

🛠️ How it works:

Upfront terms can feel seller-centric—especially to new customers. If you're asking them to pay a large amount before building trust, it can signal inflexibility or arrogance, even if that's unintentional.

Many buyers today expect flexibility baked into the offer—whether it's a CFO managing burn or a procurement lead juggling fixed budgets.

⚠️ What it affects:

Buyers may pause, push back, or choose another vendor who meets them halfway on payment structure—even if your product is stronger.

While the trade-offs of upfront payments are real, they shouldn't be binary. B2B SaaS sellers shouldn't be forced to pick between getting paid upfront and offering buyers the flexibility they expect.

So how do you capture the benefits—without adding friction to the deal? It comes down to balancing both sides.

Delivering the Pros of Upfront Payments—Without the Cons

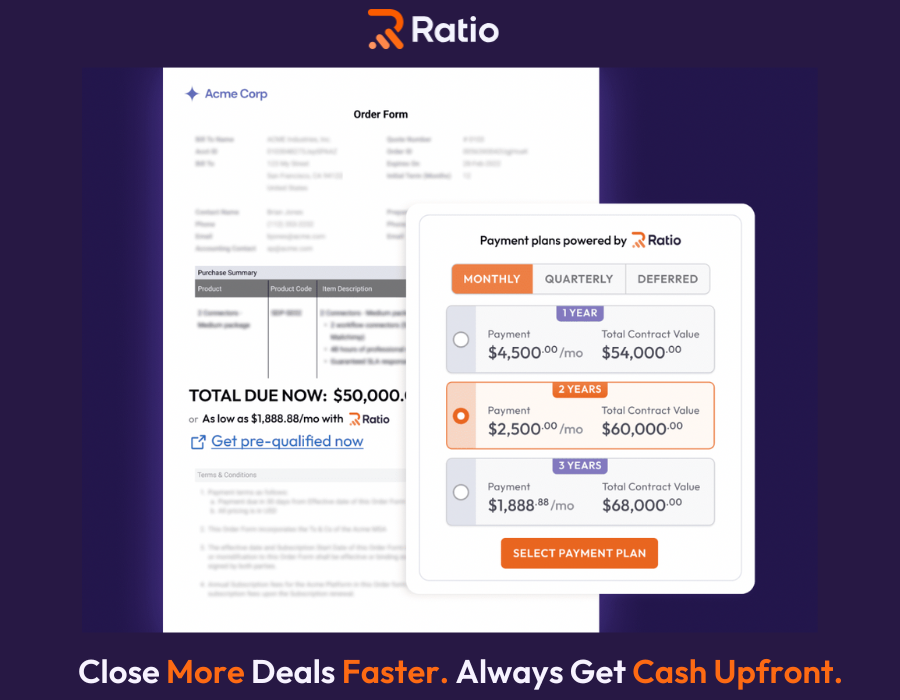

What if you could collect full payment upfront without asking your buyer to pay it all at once? That's exactly what B2B Buy Now, Pay Later (BNPL) makes possible—and Ratio Boost brings it to life.

Built for modern subscription businesses, Ratio Boost is an embedded B2B BNPL and deal-closing platform that preserves the benefits of upfront payments while removing the downsides. Here's how:

1. Cash Upfront—Still Yours

- With Boost, the seller still receives the full contract value upfront, funded by Ratio's lending infrastructure (powered by a $411M credit reservoir).

- There's no need to discount or compromise revenue recognition.

2. Buyers Get Flexibility

- Buyers can pay over time—monthly, quarterly, or custom choices—without requiring the seller to act like a lender.

- Ratio handles billing, collections, and underwriting. Sellers stay focused on growth.

3. AI-Powered Risk and Pricing Optimization

- Ratio's platform uses intent data and historical patterns to determine the right pricing and payment structures for each deal.

- Sales reps can instantly offer approved payment plans during quoting—no back-and-forth with finance teams.

4. Higher Conversion, Better Terms

- Clients like DearDoc saw a 25% uplift in ACV and up to 30% higher close rates by offering Ratio at checkout.

- Instead of offering discounts, sellers can maintain or even raise pricing—buyers say yes because the payment terms match their budget cadence.

5. Fewer Tools, Frictionless Workflows

- With Ratio, sellers consolidate quoting, payment, and collections into one streamlined platform—often replacing 2–3 legacy tools.

- Interactive, B2C-style checkout enables faster decision-making and one-call closes.

6. Zero Seller Liability

- Unlike traditional financing or deferred invoicing, there's no risk transfer to the seller. If the buyer defaults, Ratio absorbs the loss, not you.

In the current buyer-centric world, insisting on upfront payments may signal inflexibility and cost you deals. Yet, ditching upfront payment without a plan can starve your company of vital cash flow.

Ratio Boost provides a third way: upfront cash for sellers, flexible terms for buyers—no trade-offs, no liabilities, no lost revenue.

Want to see what you're leaving on the table? Visit our FAQs for quick answers.

👉 Book a demo to figure out and try Ratio Boost for yourself.

FAQs

1. What are the Downsides of Offering Payment Flexibility on Your Own?

Offering flexibility through manual installment plans or deferred billing might help close a few deals—but it also turns your SaaS company into a lender. You delay revenue, take on default risk, and absorb the operational drag of billing, collections, and credit management.

And as volume scales, that friction compounds—slowing cash flow, clouding forecasts, and pulling finance into sales decisions they weren't built for.

See how payment flexibility, when handled internally, can quietly erode your margins and slow your pipeline in this breakdown.

2. How Should SaaS Sellers Use a B2B BNPL Provider to Get Paid Upfront?

A B2B BNPL provider bridges the gap between seller needs and buyer expectations: you collect full contract value upfront, while your customer pays over time.

The right BNPL partner handles credit underwriting, disburses capital, and manages repayment—so you close deals faster, protect cash flow, and eliminate the collection burden.

Want to see the difference between selling with and without a BNPL partner? This guide walks you through both paths.

3. How can SaaS Companies use B2B BNPL to Strengthen Pricing Power and Deal Strategy?

Used right, B2B BNPL isn't just a financing tool but a revenue accelerator. By embedding flexible payment plans at the quote stage, SaaS sellers can reduce discounting, shorten sales cycles, and preserve pricing integrity.

Advanced platforms like Ratio Boost go further, using intent data and AI-driven risk models to optimize deal structure in real-time. That means sales reps offer payment options that match buyer needs and protect margins without slowing the sales motion.

Learn how top SaaS companies are using B2B BNPL platforms like Ratio Boost in our step-by-step series.

.png)