The 6 Best Embedded Finance Companies Powering B2B SaaS Growth in 2026

The Challenge: Buyers want payment flexibility. You need cash upfront. That gap is the problem.

You closed the deal. The buyer signed. But the cash? Still not in your account.

The buyer needs Net 60 to clear procurement.

Finance is chasing last quarter’s late payment.

ARR looks solid. Cash flow? Not so much.

That's why more B2B SaaS teams are adding embedded financing — flexible terms for buyers, upfront cash for you, without giving up control over how deals close.

But most platforms weren’t built for B2B SaaS. They bring:

- Rigid APIs that require engineering work to connect to your sales flow

- Limited quote-to-cash support — financing triggers after the deal, not inside it

- Risk that still lands on your balance sheet when buyers don't pay

In this guide, we’ll explain how embedded finance works, compare the top 6 embedded finance companies of 2026, and help you pick the right one to close faster, collect sooner, and scale without friction.

But first, let’s unpack the basics of embedded finance.

What Is Embedded Finance

At its core, embedded finance enables SaaS companies to integrate financial services (such as BNPL (Buy Now, Pay Later), credit, or invoice financing) directly into their sales flow.

Instead of sending buyers to banks, third-party lenders, or slow approval processes, embedded finance gives them instant access to payment options at the point of sale or in a quote.

In practice that means:

- Flexible terms like monthly or milestone-based payments.

- Instant approval without redirecting the buyer.

- Cash upfront to you, no matter how they choose to pay.

For B2B SaaS, this isn’t just a convenience; it’s a way to:

- Accelerate time-to-cash

- Reduce discounting

- Eliminate churn from budget friction

- Free your team from collections

That's what embedded finance does operationally. The strategic impact shows up when you zoom out to the full revenue motion.

To see why it’s become mission-critical for SaaS sellers, let’s look at what they’re up against in 2026.

What Financial Challenges Are B2B SaaS Sellers Facing in 2026

Buyers are slashing SaaS budgets. Sellers are stuck waiting on cash.

It’s a brutal squeeze:

- You increase prices to protect margins.

- Buyers freeze spending or push for Net 90.

- Meanwhile, CAC is rising, and VC patience is wearing thin.

And here’s what’s hitting hardest right now:

Budget cuts are killing net-new deals.

SaaS costs already eat up to 50% of incremental IT budgets, leaving little room for new vendors. CFOs aren’t buying more; they’re cutting overlap. That’s why usage-based models are leaving sellers with unpredictable revenue and limited upsell leverage.

Sales cycles are dragging.

Enterprise deals now stretch 3-6+ months through procurement gates, with finance teams pushing for Net 60 or 90. But while the buyer delays payment, your team is already delivering onboarding, support, and implementation. That cash gap bloats DSO and drains the runway.

Cash flow is buckling under delayed payments.

Buyers want Net 60 or 90. But most sellers aren’t built to be banks. You’re advancing services with 30-50% of first-year revenue tied up in CAC, and you don’t get paid until months later. That model breaks without upfront liquidity.

Embedded finance isn’t just about giving buyers payment flexibility. It’s about giving SaaS sellers the cash certainty and sales velocity needed to scale in 2026’s tighter, slower B2B environment.

Why Do B2B SaaS Sellers Need Embedded Financing

Because waiting 60-90 days to get paid slows everything down. Embedded financing flips the equation.

Your company gets paid upfront, your buyer gets flexible terms, and your sales team closes deals faster. It's not a convenience feature; it's a growth accelerator. When implemented strategically, it unlocks:

Upfront Cash on Every Closed Deal

Get paid upfront, even if your buyer pays monthly.

No more tying up revenue in payment plans or ballooning your DSO.

Faster Sales Velocity

Remove payment friction from pricing discussions.

Reps can offer flexible terms without needing approvals, workarounds, or discounts.

Margin Protection Without Discounting

Buyers get the flexibility they want.

You book the full contract value; no giveaways, no trade-offs.

Predictable Revenue and Cash Flow

Finance gains real-time visibility.

No more chasing payments or modeling uncertainty into every forecast.

No Operational Overhead

Your provider handles underwriting, collections, and risk.

You stay focused on selling, not managing receivables.

Control at Every Stage

Use financing where it helps.

Turn it on per deal, adjust terms, and embed it directly into your quote workflow.

Embedded financing isn’t a “nice-to-have.” For teams selling into tight budgets and longer cycles, it's how you protect margins without discounting and collect cash without waiting.

But not every embedded finance partner delivers these outcomes. Pick the wrong one and deals slow down after signature, exactly when they should be accelerating.

Here's how to evaluate before you commit.

What to Look for in an Embedded Finance Partner For B2B SaaS

A rep closes a large contract. Finance expects cash. Then underwriting slows down, or the buyer doesn't qualify. You're renegotiating terms after signature, delaying revenue or losing the deal outright.

Suddenly, you’re renegotiating terms after signature, delaying revenue, or losing the deal outright. If your current provider can't clear most of these, they're adding friction to your close — not removing it.

On the surface, most providers sound the same: flexible payments, fast approvals, easy integrations.

Here’s what separates deal accelerators from finance friction:

- Flexible Payment Plans: Support for monthly, milestone, or custom billing terms for buyers.

- Upfront Payouts: Full contract value paid upfront, not 90 days later to SaaS sellers.

- Non-Recourse Financing: Credit risk sits with the provider, not your P&L.

- CRM Integration: Financing embedded directly in sales workflows.

- Instant Underwriting: Approvals in seconds to keep deals moving.

- Custom Offer Controls: Let reps toggle financing on/off, tailor terms by buyer.

- AR Automation: Invoicing, collections, and reconciliation off your team’s plate.

- Enterprise Compliance: SOC 2, PCI, KYC, and AML built in.

If your current provider can’t check most of these boxes, you’re leaving cash, control, and close rates on the table.

Now let’s look at the embedded finance companies that are not only checking these boxes, but actively removing sales friction, unlocking cash flow, and driving real revenue impact for B2B SaaS teams.

Quick Comparison of The Top Embedded Finance Companies (2026)

Here’s a side-by-side look at how the top players stack up across the features that matter most to SaaS sellers. Use this table as a shortcut to spot red flags, shortlist winners, and see why Ratio leads the pack.

Top 6 Embedded Finance Companies of 2026

There’s no shortage of vendors claiming to “simplify payments” or “accelerate cash flow.” But when it comes to high-velocity B2B SaaS sales, most platforms weren’t built for your deal structure, risk profile, or sales cycle complexity.

We’ve analyzed the top embedded finance providers through the lens of real SaaS needs (instant underwriting, upfront payouts, CRM-native workflows, and non-recourse financing) and narrowed it down to six worth your time.

- Ratio (Boost)

- Capchase (Capchase Pay)

- Tranch

- Resolve (Affirm B2B)

- ChargeAfter

- Gynger

Let’s break them down, starting with the one built from the ground up for B2B SaaS: Ratio.

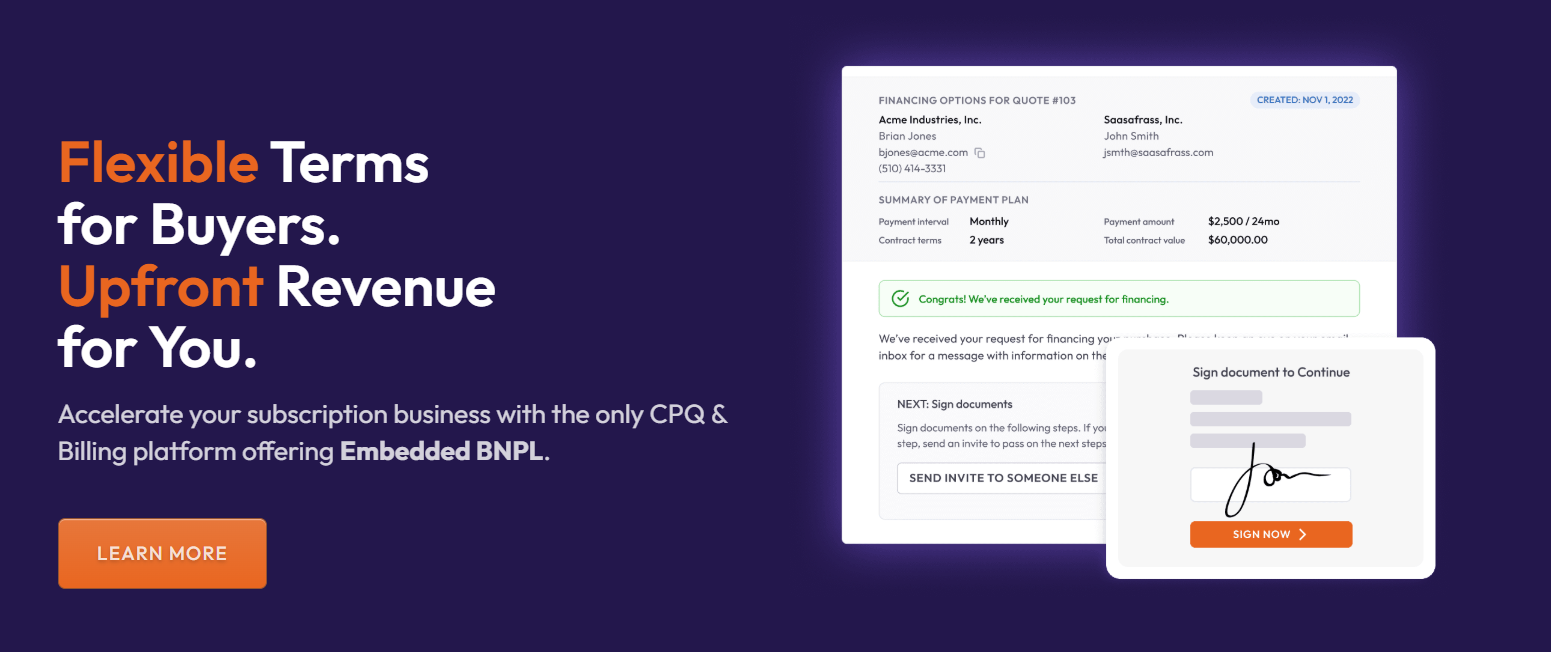

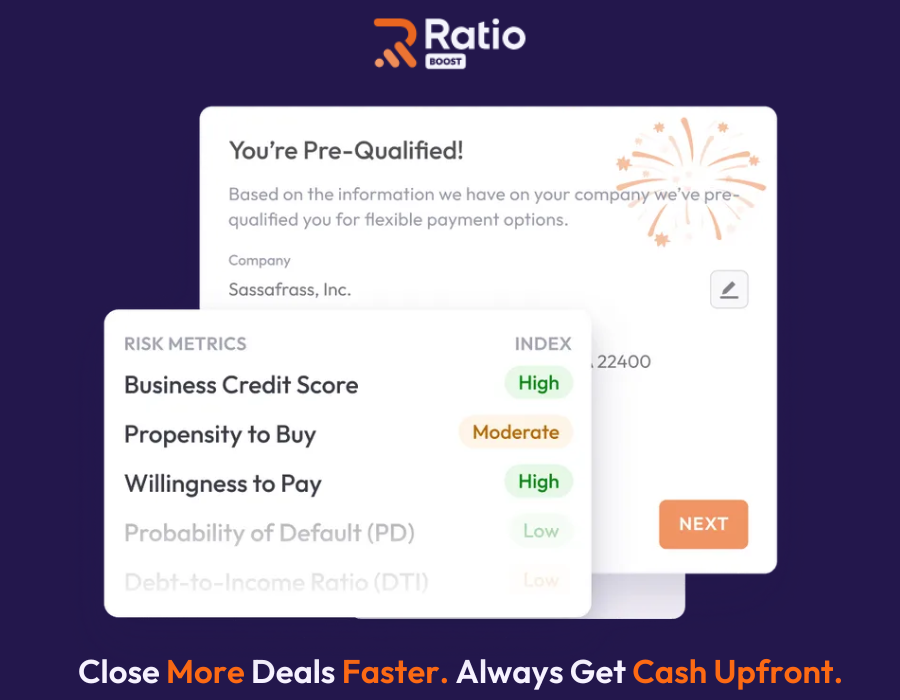

#1. Ratio Boost- Embedded BNPL Built for B2B SaaS Revenue Teams

Many embedded finance tools were built for eCommerce checkout flows or SMB credit; not complex B2B SaaS sales. They allow buyers to split payments. But sellers still wait for cash, or wrestle with broken quote-to-cash workflows.

Ratio Boost was built from the ground up to solve this.

It's an embedded finance platform(and a Closing Motion Platform) purpose-built for high-velocity, high-ACV SaaS teams. Ratio embeds flexible payment options directly into your sales process, delivers upfront cash when deals are financed, and keeps Sales and Finance aligned through the full close.

Key Features and Benefits

Embedded BNPL for B2B SaaS Deals

Ratio offers a Buy Now, Pay Later (BNPL) model tailored for high-velocity SaaS sales teams. Your buyers get flexible options while you get paid upfront.

Just faster closes, healthier cash flow, and more deals across the finish line.

With Ratio, you get:

- Access up to 100% of contract value when deals are approved

- Protect CAC payback and forecast with confidence

- No more working capital drag from long payment terms

Embedded Inside Your Sales Workflow

No portals. No handoffs. No disruption. Ratio lives in Salesforce or HubSpot and is triggered natively from your deal flow.

- Launch offers from CPQ or quote stage to increase chances of deal closures

- Align Sales and Finance with real-time visibility

- Streamline financing approvals and automate collections

- Embed financing terms in the buyer’s contract. Close the deal in one seamless motion: no separate paperwork, no friction, no delays.

Deal-Level Embedded Financing

With Ratio, financing is triggered directly inside Salesforce or HubSpot at the quote stage.

Sales reps can select flexible payment terms per opportunity without rewriting contracts or sending buyers to external applications.

- Launch financing from the opportunity or quote

- View buyer eligibility in seconds before contract finalization

- Enable or disable financing per deal

- Use fallback options like standard net terms for non-qualifying buyers

- Keep Sales and Finance aligned inside the same closing motion

Finance teams can configure approval workflows for non-standard terms, while underwriting thresholds are managed through the platform.

Control Where It Matters: At the Close

Whether it’s a $5K pilot or a $250K enterprise agreement, financing isn’t one-size-fits-all.

- Sales chooses when financing is presented as part of the quote

- Finance sets guardrails around eligibility and cost allocation

- Terms adapt to contract value, duration, and risk tier

- Payment flexibility replaces reactive discounting

Seamless Integration With Your Revenue Stack

Set it up once: then quote, close, and collect without switching tools.

- CRM & CPQ: Salesforce, HubSpot

- Billing: Chargebee, Recurly, Stripe

- Contracts: PandaDoc, DocuSign

- Accounting: NetSuite, QuickBooks, Xero

- Banking and Payments: Plaid, GoCardless, ACHQ

Pros

- Accelerates cash collection without discounting.

- Embeds into sales workflows; no rep behavior change.

- Reduce seller exposure.

- Structured payment schedules aligned to SaaS contracts.

- Fast onboarding and instant approvals.

Cons

- Advanced usage-based pricing may require a custom setup.

- Enterprise buyers with internal financing may opt out.

- Custom deal terms beyond standard formats may need Ratio support.

Pricing

Unlike other embedded financing B2B platforms that charge subscription or platform fees, Ratio has no subscription cost.

Instead, a financing fee applies, and sellers can choose how to handle that fee:

- Cover it themselves

- Pass it to the buyers or

- Split it 50/50

This gives SaaS sellers complete control over how financing affects margins and the buyer experience.

Customer Success Spotlight

DearDoc, a B2B healthtech SaaS company, used Ratio Boost to remove financing friction and bring deals to the finish line faster.

By embedding financing directly into their sales workflow, the company eliminated approval delays and simplified the entire close process—from proposal to payment.

The results?

Financing approvals reduced to 30-45 minutes

20-30% improvement in close rates

25% increase in average selling price (ASP)

And don't just take our words for it. Hear it directly from the DearDoc team:

Ratio powers revenue for many other fast-growing B2B companies across healthtech, fintech, and logistics, including MarketJoy, Lucid Bots, and Taxwell. The company is rated 4.4/5 on G2.

Demo / Free Trial Availability

👇 Ready to see how Ratio fits into your stack?

Schedule a free demo. Let’s walk through your sales flow together.

See how Ratio Boost fits into your existing sales stack. Book a 25-minute demo — we'll walk through your deal flow and show you exactly where embedded financing connects.

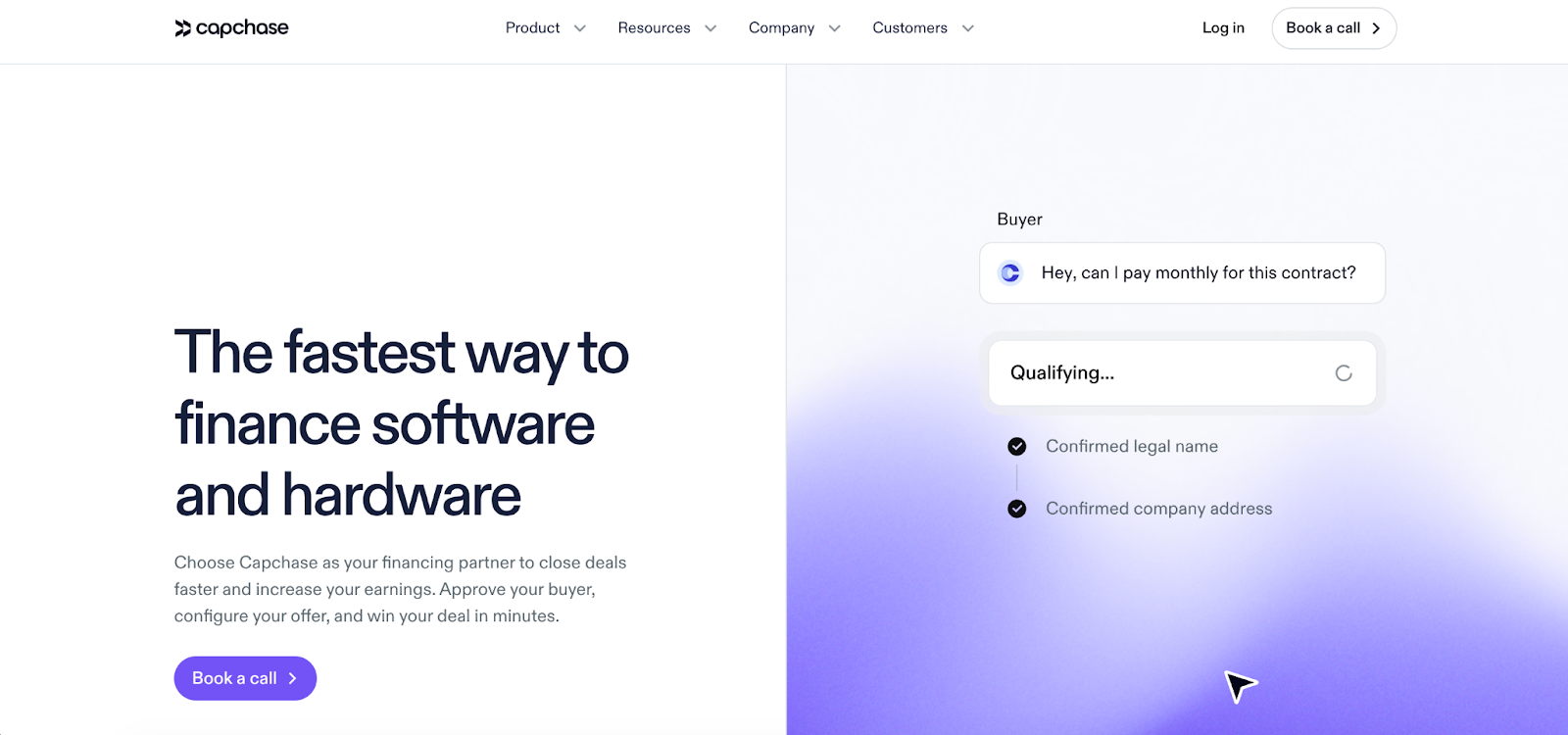

#2. Capchase Pay - Revenue-Based Financing for Growing SaaS Startups

Capchase Pay gives B2B SaaS sellers a fast way to offer flexible payment terms without risking cash flow or margins.

You offer your buyer monthly or quarterly terms. Capchase pays you the full contract value upfront on approved deals and handles collections directly with the buyer, including assuming the risk of payment default. Sellers have no repayment responsibility once funds are disbursed.

For sales-led teams navigating tight budgets and lengthy approvals, Capchase helps reduce payment friction by replacing large upfront-payment discounts with flexible monthly or quarterly terms, without requiring internal credit extensions.

Key Features and Benefits

- Advance a portion of future ARR from signed contracts

- Funds released in monthly tranches or lump sum based on the risk profile

- Visibility into financing activity and payment performance

- Integrates with Stripe, QuickBooks, Xero, Chargebee, and more

Pros

- Access working capital without dilution

- Works well for CFOs managing long contracts and cash flow

- Transparent pricing tied to contract health and risk score

Cons

- Buyer payment experience may feel complex in certain workflows

- Approval amounts may be lower than requested, requiring additional review

- Requires existing, signed contracts to draw funds

Pricing

Custom fee structure based on contract quality, size, and repayment terms. Typically structured as a percentage of capital deployed with clear terms.

Notable Clients

- Capchase Pay is trusted by growth-stage SaaS companies looking for non-dilutive capital.

- Notable users include Rhombus, and Creyos.

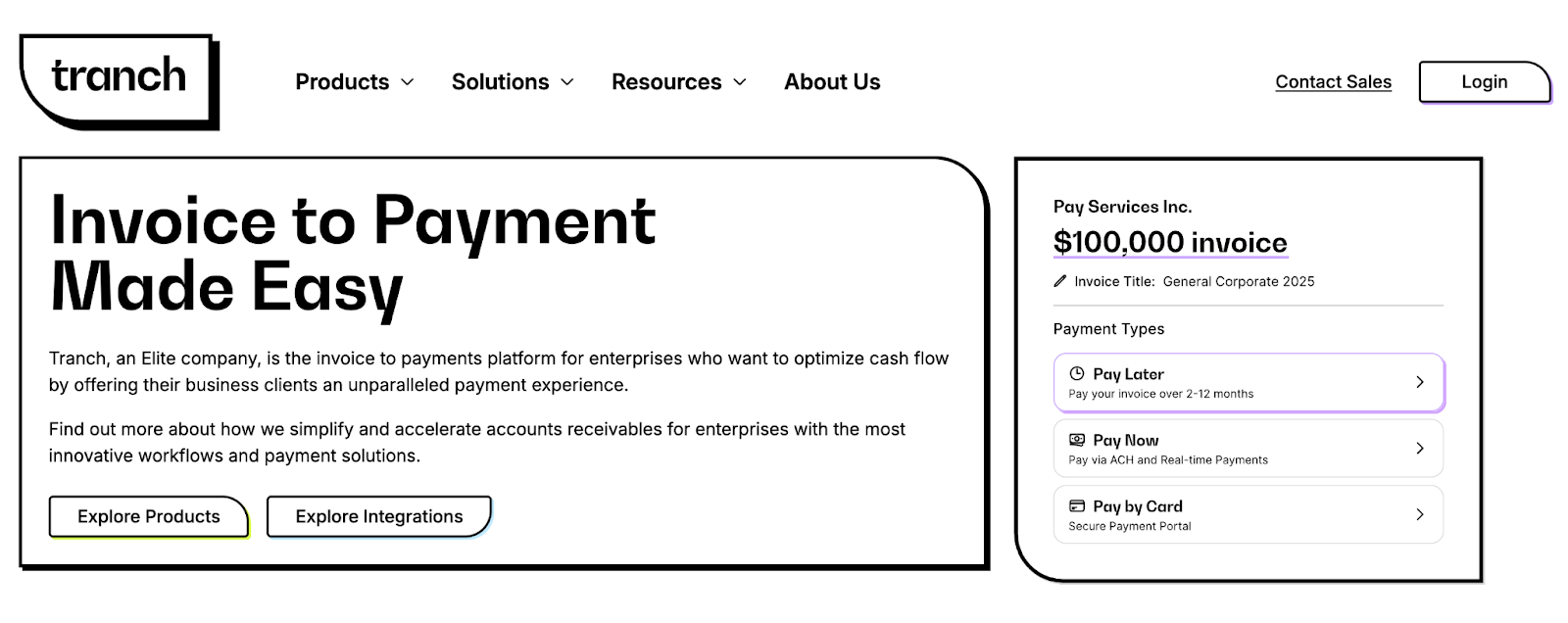

#3. Tranch – Installment-Based BNPL for SaaS and Services Contracts

Tranch is an embedded finance solution that offers BNPL terms to B2B buyers, targeting professional service-based businesses, agencies, and SaaS companies. It lets buyers split large invoices into manageable monthly payments while still paying sellers upfront.

Unlike broader platforms, Tranch is more checkout-focused and best suited for one-time or contract-based transactions rather than recurring SaaS workflows.

Key Features and Benefits

- BNPL terms (up to 12 months) for B2B invoices

- Credit checks and buyer approvals

- Upfront payment to vendors, minus a transaction fee

- Integrates with ERP systems

- Supports API or low-code implementation for invoice and payment workflows

Pros

- Simplifies large-ticket sales with flexible terms

- Seller gets paid upfront, reducing cash flow risk

- Streamlined experience for both buyer and seller

Cons

- Not necessarily designed for CRM or quote-to-cash integration

- Limited support for recurring SaaS or milestone billing

- Better suited for agencies or one-off service deals

Pricing

Specific pricing models are not publicly disclosed; fees typically depend on term length, invoice size, and risk profile (vendors/clients negotiate terms with Tranch)

Notable Clients

- Trusted by mid-market service providers, agencies, and SaaS platforms offering one-time contracts.

- Specific names are not publicly disclosed.

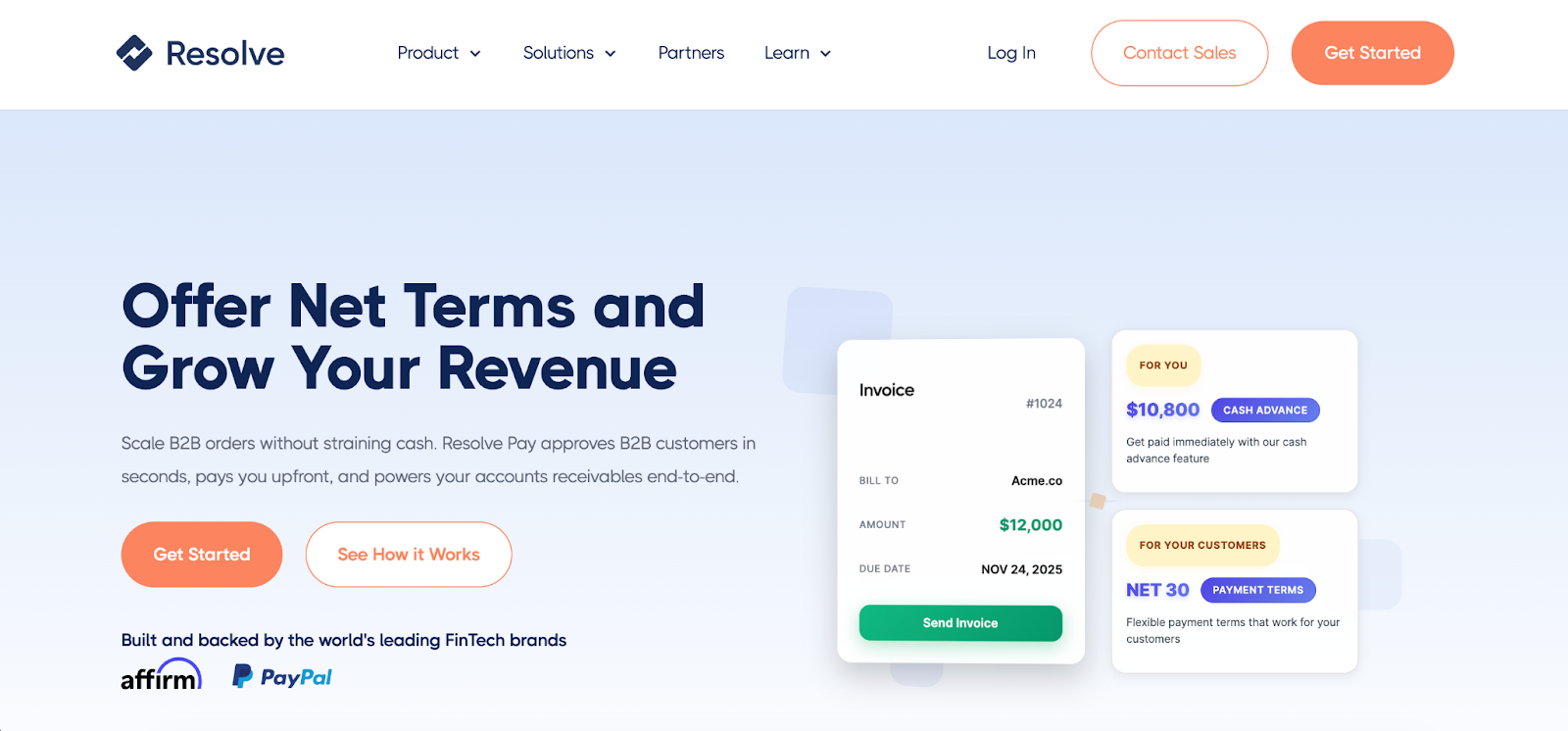

#4. Resolve (Affirm B2B) – Net Terms Management for B2B Invoicing and Trade Credit

Resolve, spun out of Affirm, focuses on offering net terms to B2B buyers, typically at the invoice or checkout stage. It’s designed for B2B merchants and platforms looking to automate credit checks, offer Net 30/60/90 terms, and improve collections without taking on risk.

It’s especially popular in industries like wholesale, manufacturing, and B2B marketplaces. For SaaS sellers, it may be limited by a lack of CPQ, CRM, or contract workflow integration.

Key Features and Benefits

- Net terms financing (30/60/90) with credit checks

- Seller payout with Resolve managing buyer repayment

- Buyer portal with invoice tracking and reminders

- Basic API and eCommerce plugin support

Pros

- Automates credit decisions and collections

- Preserves seller cash flow with upfront payments

- Ideal for transaction-based or product-led B2B businesses

Cons

- Not purpose-built for SaaS workflows

- No CPQ/CRM/contract integration

- Limited customization for complex sales motions

Pricing

- Pricing is risk-based and varies depending on advance rate, term length, and buyer profile.

- Sellers can pass fees to buyers.

Notable Clients

- Used by B2B marketplaces, manufacturers, and distributors.

- Known clients include Flexport and The Good Crisp Company.

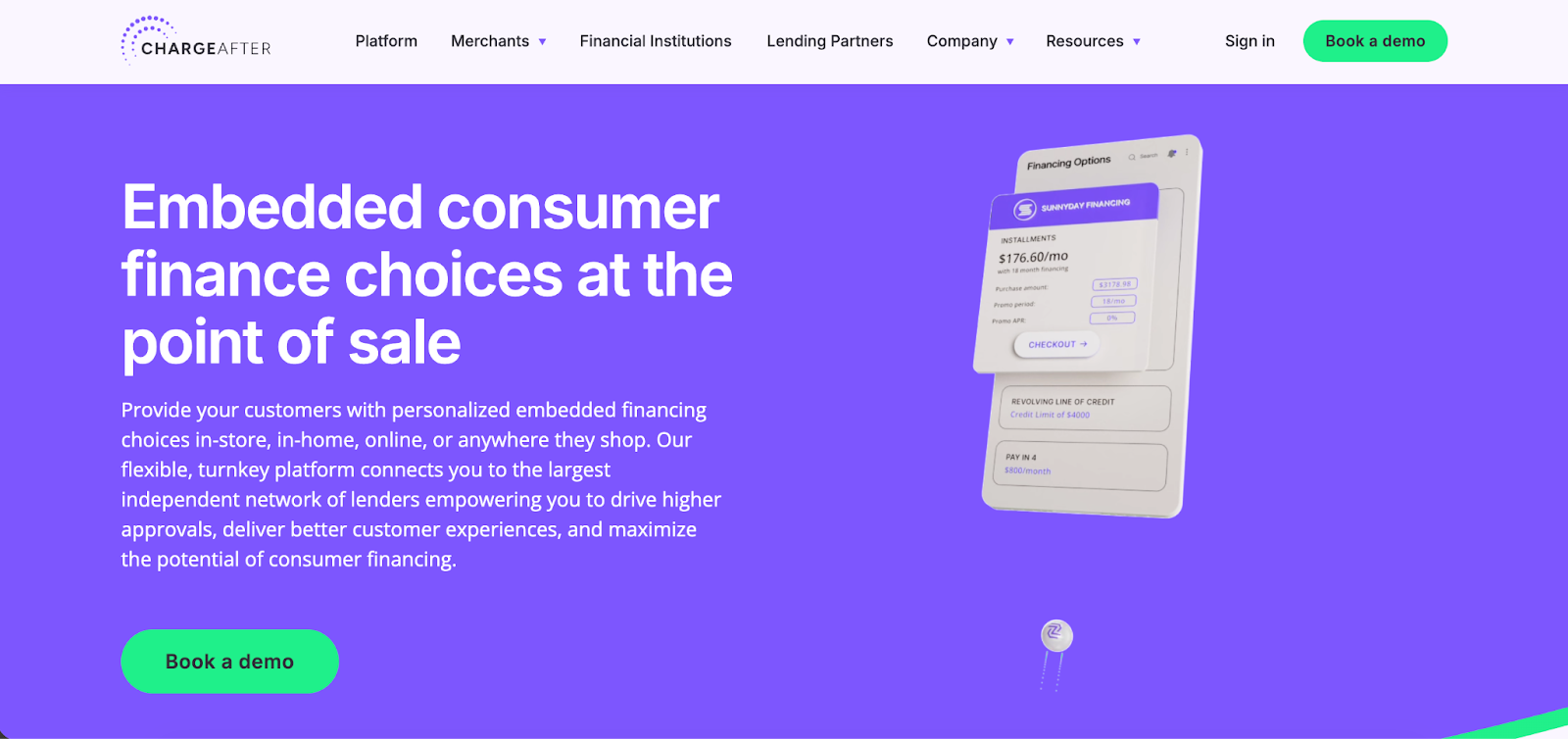

#5. ChargeAfter – Multi-Lender BNPL Platform for B2B eCommerce

ChargeAfter offers a point-of-sale financing platform that connects merchants with a network of lenders. While it’s primarily built for B2C and retail-style B2B purchases, it provides flexible checkout financing with real-time approvals across multiple lenders.

For SaaS sellers, the value is more limited—ChargeAfter lacks native CPQ or CRM integration, and its underwriting is geared toward consumer-style purchases rather than recurring contracts.

Key Features and Benefits

- Multi-lender financing engine with broad buyer approval

- Credit checks and real-time financing offers

- White-labeled checkout experience

- Lender waterfall model to maximize approvals

Pros

- Strong buyer-side flexibility and high approval rates

- Works well for platforms or marketplaces selling bundled SaaS/hardware

Cons

- Not specifically designed as a quote-to-cash CRM/CPQ-native tool.

- No embedded quoting or contract-level financing

- Seller-side controls are limited

Pricing

- Pricing is not published publicly and typically involves per-transaction or partner fees associated with lending products and lender terms.

Notable Clients

- Best suited for B2C and retail-driven B2B.

- Clients include Lenovo, Wayfair, and other consumer brands extending financing at checkout.

#6. Gynger – Buyer-Led Financing for Tech & AI Infrastructure Spend

Gynger offers upfront capital to companies for software and infrastructure purchases. Buyers use Gynger to finance large tech spends over time, while vendors get paid upfront.

However, Gynger operates primarily through its vendor portal rather than as a native embed within a seller’s CRM or CPQ flow.

While sellers can introduce financing during negotiations, the experience typically runs alongside the quote-to-cash process instead of directly inside it. As a result, financing may require coordination outside the core quoting workflow, shaping how reps manage timing, eligibility visibility, and the overall buyer experience.

Key Features and Benefits

- Buyer-initiated SaaS and tech spend financing

- Upfront payments to vendors

- Flexible repayment options for buyers

- Credit lines based on financial profile

Pros

- Helps buyers manage significant tech expenses

- Vendors get paid faster without chasing procurement

Cons

- Not positioned as a quote-to-cash/CPQ-native platform

- Sellers have limited control over when and how financing is offered

- No automation or quote-to-cash integration

Pricing

- Not public; depends on buyer's credit profile and loan terms.

- Typically, the buyer pays the financing cost.

Notable Clients

- Used by tech buyers across mid-market and enterprise to finance software, hardware, and services.

- Less relevant for sales-led SaaS teams.

With so many vendors on the table (each with different strengths, trade-offs, and target use cases) what matters most is finding an embedded finance company built for your revenue model, sales workflow, and growth stage.

Now let’s look at why more SaaS sellers are choosing Ratio to lead that shift.

Ratio Boost: The Embedded Finance Company Modern SaaS Teams Are Partnering With

When B2B SaaS companies rethink how they manage cash flow, close deals, and remove friction from sales, more of them are choosing Ratio.

Behind the company are SaaS operators and finance veterans who’ve lived the pain of slow payments, rigid approvals, and broken quote-to-cash workflows. Ratio exists to solve a systemic problem: the way software is bought, sold, and funded is outdated.

That vision is backed by real momentum.

Ratio recently raised $15.8M and Secures $100M in Lending Capacity, so it’s not just ready to power your next deal, it’s built to solve your cash flow constraints. The company is reimagining embedded finance from the ground up.

And it's working!

SaaS teams using Ratio are seeing faster closes, higher ACVs, better cash flow, and fewer deals lost in procurement limbo.

👉 Join the companies rewriting their revenue playbook. Schedule a free demo today and see what’s possible with embedded financing designed for SaaS.

Disclaimer: All insights in this post are based on publicly available data, vendor websites, and user reviews as of our latest research. While we've prioritized accuracy and relevance for B2B SaaS decision-makers, we recommend validating features, pricing, and fit through vendor demos and tailored consultations before making a final selection.

.png)

.png)