Beyond SaaS Capital: How to Get Cash Upfront Without Traditional Debt

The Challenge: You Treat Signature as the Win. But the Close Is Cash Upfront.

Imagine that you are a B2B scale-up. You’re winning deals, earning conviction, and building momentum. But your cash flow isn’t keeping pace with your ambition.

A buyer says yes. You get the signature. Then come the handoffs: sales to finance, finance to billing, billing to collections. Meanwhile, your bank account stays on hold.

That’s not closing. That’s fragmentation.

Fragmentation turns yes into delay, delay into risk, and risk into lost momentum.

Traditionally, founders patched this gap with credit lines or revenue-based debt from providers like SaaS Capital.

But debt doesn’t fix the system. It just papers over it.

Ratio is the Closing Motion Platform.

We connect the dots between proposal, payment, and collections—turning a buyer’s commitment into cash upfront.

But before you make a choice between SaaS Capital and Ratio, let's learn,

What Is Non-Dilutive Financing?

Non-dilutive financing means getting money to grow your business without giving up ownership. And it's not a niche approach anymore.

The global revenue-based financing (RBF) market is projected to grow from ~$9.77 billion in 2025 to ~$15.86 billion in 2026. Rising adoption among U.S. SMEs and startups signals a clear shift: founders are choosing models that preserve equity and control.

Unlike venture capital, where you sell part of your company in exchange for funding, non-dilutive options let you raise capital while keeping 100% of your equity. You stay in control, and you keep the future upside.

Let’s say you raise $1 million:

- Dilutive (Venture Capital): You get the money, but give up, for example, 10% of your company.

- Non-Dilutive (e.g., SaaS Capital): You get the funds and retain 100% ownership.

Founders use non-dilutive funding to grow, hire, or extend their runway without bringing in new investors or losing decision-making power.

Common Types of Non-Dilutive Capital

Non-Dilutive Is the Outcome. But the Mechanisms Differ.

Not all non-dilutive funding works the same. Some tools give you capital at the company level. Others move cash faster through your sales motion.

- Government grants – Non-repayable, highly competitive, often narrow in scope.

- Loans or credit lines (e.g., SaaS Capital) – Debt-based instruments tied to MRR or ARR, typically with interest, covenants, and manual drawdowns.

- Revenue-based financing (RBF) – Capital tied to future earnings, repaid flexibly as revenue comes in.

Then there’s Ratio. It’s not a financing product, but a Closing Motion Platform. Ratio doesn’t issue loans. It embeds BNPL directly inside proposals so buyers can pay flexibly while sellers receive cash upfront. Invoicing, collections, and recovery are automated, keeping renewals and cash timing connected and predictable.

Now that you know the core difference between types of non-dilutive financing, let’s look at some common SaaS funding mistakes.

What Are Some Common SaaS Funding Mistakes

Even fast-growing SaaS teams make the wrong calls when it comes to funding. And the stakes are actually higher than ever.

In some sectors like life sciences, early-stage risk capital has pulled back, accelerating the shift toward non-dilutive capital models. While not uniform across all verticals, the trend is clear: founders want faster cash with fewer strings.

The problem? Most teams still approach it with an old playbook.

Here’s what we’re seeing most often:

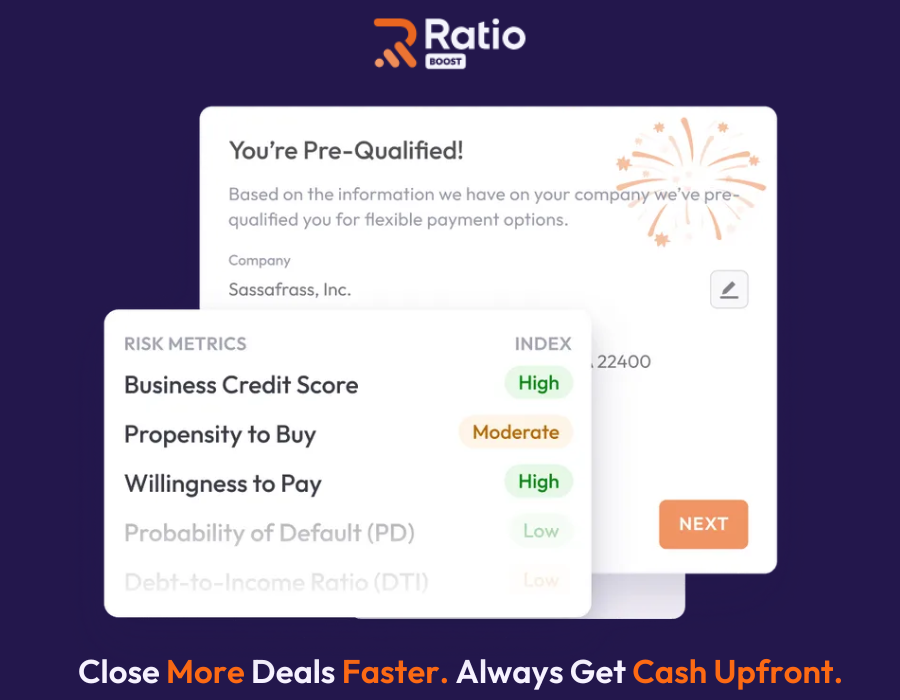

Mistake #1: Thinking Signature = Closed Deal

A signed contract is not cash. The handoff from Sales to Finance to Operations introduces friction, and cash often arrives weeks later, if it arrives at all. A proper closing motion ensures that when a deal is won, cash is activated, not delayed.

Mistake #2: Discounting to Solve Budget Pushback

When buyers hesitate, teams often default to discounting. The result is lower ACV, shrinking margins, and reduced customer lifetime value. In most cases, the real issue isn’t price. It’s payment flexibility. Solving for terms preserves value far better than cutting the number.

Mistake #3: Using Runway Debt to Fix Sales Friction

Credit lines and runway debt can extend operating time, but they don’t help deals close faster. Tools like SaaS Capital operate at the company level, not the deal level. They don’t appear in quotes, change buyer experience, or remove friction from the sales process. Debt is useful for R&D. Closing tools are what improve close velocity.

Mistake #4: Ignoring Renewals and Collections After the Close

Adding capital doesn’t fix operational drag. Manual invoicing, payment chasing, and draw requests still slow teams down. Scaling requires automation across billing, collections, and recovery, not additional administrative headcount.

Mistake #5: Blind to Balance Sheet Impact

Not all non-dilutive funding behaves the same way. Some structures add debt and leverage, while others are designed to keep the balance sheet clean. If a funding tool limits future borrowing or complicates fundraising, it isn’t truly flexible.

SaaS Founder Mistakes from the Field

Other common pitfalls we hear again and again on Reddit:

- Building before validating real demand.

- Launching without a clear marketing motion.

- Hiring for today, not tomorrow.

- Pricing without understanding costs or differentiation.

- Raising too early, without traction.

- Overbuilding MVPs that never ship.

These mistakes cost deals, delay cash, and bloat your team before you’re ready. Avoiding them starts with fixing the way you close and the capital model you close with.

Up next: A quick comparison of the two fairly common non-dilutive paths: SaaS Capital and Ratio.

Quick Comparison: SaaS Capital vs. Ratio

On the surface, both SaaS Capital and Ratio help B2B companies access cash upfront. But how they do it—and what that means for your business—looks very different.

Here’s how the two compare across the fundamentals:

This comparison is based on public data, vendor resources, and our own analysis as of 2026. Features may vary by plan, geography, or direct negotiation. Always speak with each provider’s sales team to ensure it fits your specific use case.

Now, let’s see SaaS Capital and Ratio stack up against each other.

Two Approaches to Solve the Same Problem, But Only One Closes with Upfront Cash

At a glance, SaaS Capital and Ratio seem to solve the same problem: helping B2B SaaS companies access cash. But under the hood, they’re built on fundamentally different philosophies.

SaaS Capital’s core model revolves around an MRR-based line of credit.

Ratio’s core model is the Closing Motion Platform, which turns a moment of “Yes” into cash upfront.

Capital Timing: Lending vs. Closing

For scale-ups, the biggest capital problem isn’t access. It’s timing.

SaaS Capital helps after the deal is done. It's a line of credit sized against ARR, structured as drawdowns. Getting the facility in place takes 5-8 weeks of underwriting and diligence.

Once established, draw requests are funded in 24-48 hours, but the capital still has no connection to your deal flow. It sits at the company level, not the deal level.

Sales closes. Finance chases capital. Cash arrives weeks later.

The result? Cash lags behind sales velocity. Every month, there’s a gap between growth and liquidity.

Ratio fixes the when, not just the how much. It’s not a loan. It’s the Closing Motion Platform. It puts financing inside the deal, not after it.

Ratio is built to deliver cash at the moment of yes—automatically, deal by deal.

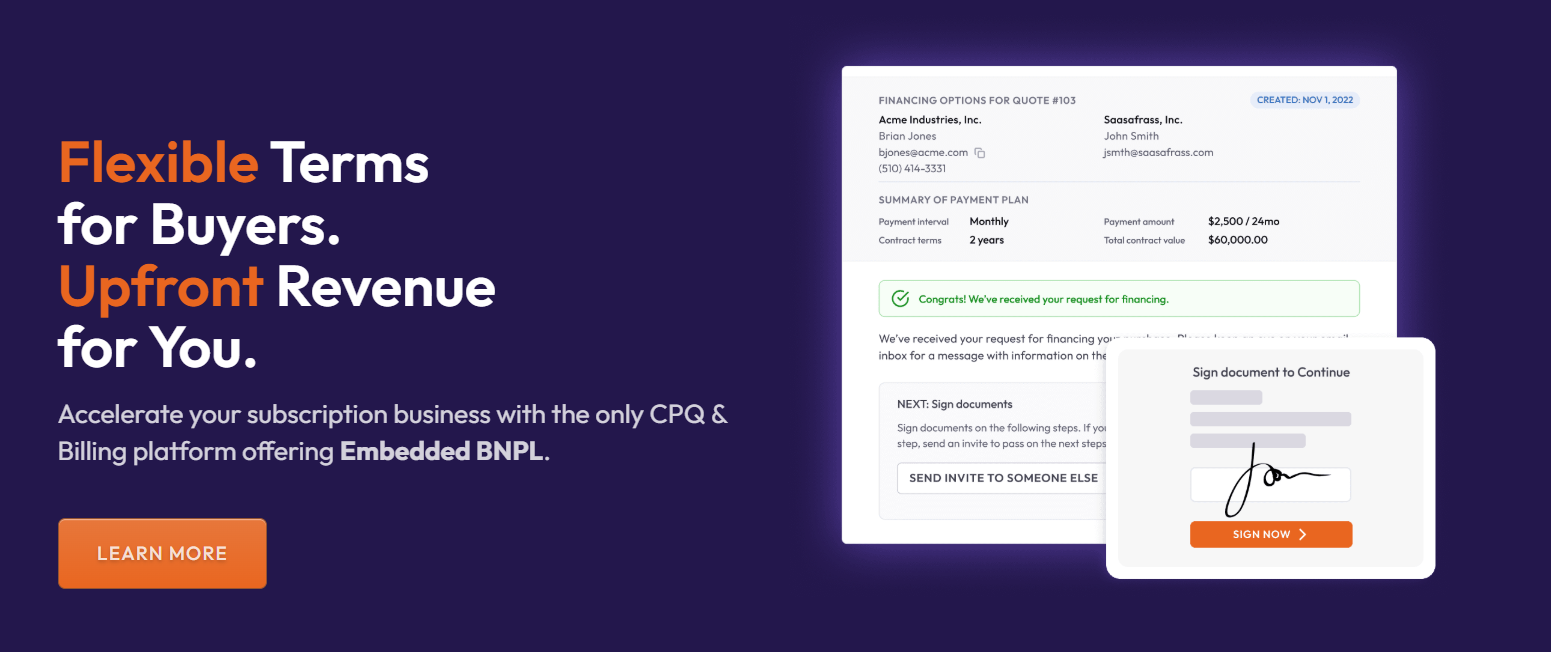

- B2B BNPL is embedded in proposals

- Buyer gets flexible payment terms instantly

- Designed for upfront payout, with cash activated when the buyer commits and the close-to-cash flow is set.

This is crucial at scale. When you’re closing dozens of deals a month, capital can’t trail behind. It has to move with Sales.

🛒 Buyer Experience: Friction vs. Flexibility

At scale, friction at the point of purchase compounds. SaaS Capital is a finance backend, not a buyer experience layer as you need. It doesn’t change the way deals are presented or closed.

Buyers still face large upfront asks, limited payment flexibility, and uncertainty that often requires back-and-forth between Sales and Finance. When budgets are tight, deals stall. When flexibility is needed, timelines stretch.

Tight budget? They stall. Need flexibility? They delay.

But Ratio meets the buyer where it matters: in the quote.

Buyers instantly see:

- Flexible BNPL terms shown in the proposal

- Defer payments for 30-60 days

- Fast, automated approval inside the deal flow

It’s B2B that feels like B2C. No confusion. No back-and-forth on payment terms.

This matters when you’re running a scaled sales engine. The faster buyers say yes, the faster cash hits the system, and the fewer sales have to discount just to close.

Sales Motion: Discount-Driven vs. Deal-Structured

At scale, pricing integrity breaks when Sales has no closing tools. SaaS Capital isn’t designed to help reps close. It’s a Finance tool. So when budget objections hit, reps rely on old tricks:

- Discount the ACV.

- Offer shaky monthly terms.

- Trade margin for speed.

This creates misalignment: Sales wants speed. Finance wants control. No one wins.

Ratio places structured financing directly inside the quote. BNPL options are visible before signature, buyers see terms clearly before negotiation begins, and reps do not have to touch price to move a deal forward.

Suddenly, Sales has leverage that protects value and accelerates the deal. That’s how scale-ups maintain margin while moving fast. You close bigger, close faster, and keep pricing intact—without looping in Finance every time.

Renewals & Collections: Fragmentation vs. Cash Continuity

At scale, what breaks isn’t Sales. It’s what happens after.

With SaaS Capital, the workflow remains fragmented. Sales closes the deal, Finance draws funds, and Operations chases payments. No single system owns the full close-to-cash process, leading to disconnected workflows, missed invoices, increased forecasting risk, and internal finger-pointing.

Ratio bridges the gap between signature and settlement with a connected flow.

- Invoices go out automatically.

- Payment schedules are built-in.

- Failed payments are retried automatically.

- Finance sees recovery in real time.

Sales gets to focus on selling. Ratio handles cash collection and recovery. Finance gets forecast clarity.

Qualification: Board-Level Credit vs. Sales-Stage Enablement

When you’re scaling, you don’t need credit approval—you need deal acceleration.

SaaS Capital offers clean, non-dilutive debt. But it’s gated:

- Strong SaaS metrics.

- Full diligence cycle.

And it takes time. From the first call to funding, SaaS Capital's process typically runs 6 to 8 weeks, involving an on-site meeting, accounting diligence, a technical review, and legal documentation. It’s a board-level decision. Useful for planning, but irrelevant for day-to-day selling.

Ratio flips the script. There’s no traditional company-level credit application or long-form diligence cycle. If you're a scale-up with $5M–$100M in ARR, capital activates at the moment of yes.

- Real-time deal-level underwriting

- Terms shown inside the quote

- Full payout triggered at the moment of yes (cash upfront), not at signature

Your sales team gets a new kind of closing motion. One that turns contracts into upfront cash by automating the underwriting and approval process within the deal flow.

That’s the shift scale-ups need: Not more capital access, but more capital activation at the point of close.

Scalability: Manual Volume vs. Automated Velocity

What kills scale isn’t lack of capital. It’s the cost of closing.

With SaaS Capital, volume increases the administrative load. Credit lines may grow, but drawdowns remain manual. Invoicing and collections still require hands-on work. As revenue scales, headcount follows, and operational overhead grows alongside it.

Revenue scales. Headcount follows. Admin burden explodes.

Ratio is software-first, not finance-admin-led.

- BNPL embedded in proposals.

- Underwriting in real time.

- Cash is released at the moment of yes.

- Collections, renewals, and recovery fully automated.

It’s not just scalable. It’s scalable without adding people. And when you double your pipeline, you need something that doesn’t break. But instead, something that adjusts. That’s what a real Closing Motion Platform does.

Balance Sheet Impact: Liability Load vs. Cash Activation Structure

SaaS Capital gives you a credit line, but it’s still debt.

- It shows up as a liability on your balance sheet.

- It comes with covenants, borrowing limits, and reporting rules.

- If a customer defaults, you're still on the hook.

That’s fine for long-term investments. But if you're using it to fix sales cash flow, you’re layering friction on top of velocity.

Ratio takes a different path: the transaction is structured as a true sale of the contract rather than a traditional loan.

- Customer commitments turn into immediate liquidity.

- Ongoing payment management is handled within the closing flow.

- Growth capital activates without layering traditional debt into operations.

The result is minimal impact on leverage ratios, no covenant pressure, and no need to renegotiate existing financing. Sales get cash at close, Finance maintains clean books, and the business avoids adding structural baggage to fix operational timing problems.

And the whole company avoids the debt trap of solving operational pain with structural baggage.

SaaS Capital adds liability. Ratio activates liquidity by turning customer commitments into cash.

Note: Accounting treatment may vary. Please consult your controller, auditor, or legal advisor for specific guidance on “true sale” qualification and balance sheet implications.

Strategic Metrics: Valuation Signals vs. Velocity Outcomes

SaaS Capital is optimized for boards and investors focused on long-term valuation signals. Its model emphasizes retention, ARR growth over time, and stability, supported by benchmarking tools designed for mature, predictable businesses. This approach works well when the priority is financial optics and long-range planning.

But Ratio optimizes for what actually moves the needle today:

- Closing Velocity — Time from “yes” to cash-in-bank.

- Cash Certainty — % of revenue realized upfront.

- Discount Reduction — ACV preserved without cutting the price.

- Operating Leverage — More revenue, fewer people.

This isn’t about looking good later. It’s about scaling cleanly now. Ratio eliminates the lag between signature and liquidity.

These outcomes change how teams operate. Sales stops discounting to force deals through. Finance stops chasing collections. Leadership stops waiting for signed revenue to turn into usable cash.

You don’t just close faster. You get paid faster, with fewer people, and fewer risks.

SaaS Capital optimizes for valuation optics.

Ratio optimizes for sales efficiency, free cash flow, and margin integrity.

Both are useful. But only one lets you reinvest the same day the deal is signed.

What People Are Saying About Flexible Financing in SaaS

Across real SaaS conversations, one thing is clear: flexible payment options are no longer a luxury. They’re a competitive edge.

- BNPL unlocks higher conversion by removing upfront budget friction.

- Payment flexibility increases accessibility for smaller buyers who would otherwise delay or walk.

- The shift is less about “financing” and more about removing friction at the point of sale.

These aren’t just hypotheticals. They’re reshaping how SaaS companies close.

What Users Say About Ratio

Unlike traditional financing tools, Ratio operates as a close-to-cash infrastructure, showing up inside the deal flow itself. And customers are talking.

On G2, Ratio earns a 4.4/5 rating, with users consistently highlighting ease of use, seamless integration into existing workflows, embedded payment plans, and responsive support.

“Ratio has become our best friend... We collect more cash quicker and offer flexible terms without giving up anything at kickoff.”

“Setup was smooth, and we started using it immediately.”

—4/5, Alioscia C., G2 Reviewer

Customer Highlight: DearDoc

B2B healthtech company DearDoc used Ratio Boost to remove deal friction and close faster. By embedding financing directly into their proposals:

- Approvals dropped to 30–45 minutes

- Close rates jumped 20–30%

- Average selling price rose 25%

Here’s what the founder had to say about us:

Ready to see how it works? Book a free demo and turn every “yes” into upfront cash.

Ratio or SaaS Capital: Which One Do You Need?

SaaS Capital and Ratio address different moments in a company’s growth. Both are non-dilutive. Both preserve equity. But they operate very differently.

Below is a clearer look at the strengths and tradeoffs of each model.

SaaS Capital: The Credit Line Model

Think of this as a flexible credit facility structured around your recurring revenue.

Pros

- Flexible capital pool: Funds are not tied to specific deals. Capital can be deployed for hiring, R&D, acquisitions, or runway extension.

- Non-dilutive: No equity is sold. Founders retain full ownership.

- Familiar structure: Operates as a senior secured credit facility, a model that CFOs and boards understand well.

- Scales with MRR: As recurring revenue grows, borrowing capacity increases.

Cons

- It is debt: Recorded as a liability and typically subject to covenants.

- Risk remains with you: If customers default, repayment obligations remain.

- No sales impact: It does not appear in proposals or influence deal velocity.

- Operational friction: Requires setup time, diligence, reporting, and manual drawdowns.

SaaS Capital is most effective when the goal is structured, company-level capital planning.

Ratio: The Closing Motion Model

Ratio operates inside the sales process. Instead of extending company-level credit, it activates capital at the moment of close.

Pros

- Embedded in the deal: Flexible payment terms are surfaced directly in proposals.

- Accelerates close velocity: Removes budget friction at the point of commitment.

- Preserves pricing integrity: Reduces the need for upfront-payment discounts.

- Automates post-close workflows: Billing, collections, and recovery operate within a connected flow.

- Designed to avoid traditional debt layering: Structured around contract activation rather than loan issuance.

Cons

- Transactional cost per deal: A fee applies to funded contracts.

- Commercial dispute responsibility: If a customer refuses to pay due to product or service issues, that responsibility remains with the vendor.

- Best suited for standardized B2B contracts: Highly bespoke, heavily negotiated agreements may require additional review.

Ratio is built for scale-ups focused on improving closing velocity, cash timing, and operational automation.

Now that you understand how each model works, the real question is simple: do you want capital that waits behind the deal, or capital that activates the moment you close it?

Ratio: The Closing Motion Platform Built for Scale-Ups

Most B2B teams treat close as a signature. The modern close ends with cash upfront.

And when B2B SaaS companies think of cash upfront, they think of Ratio.

We are a team of SaaS and finance veterans who have experienced the challenges of the fragmentation of the close. We believe scale-ups should be able to grow on merit, not on cash timing. That’s why we developed Ratio to ensure cash certainty at the moment of “yes!”

Our approach is gaining measurable momentum.

Backed by $411M in venture funding and a $400M credit facility, Ratio is built for the long game. Our Closing Motion Platform is here to support your long-term goals. We are reimagining embedded finance, so every scale-up can convert customer commitment into cash upfront.

And it's working!

SaaS teams using Ratio are seeing faster closes, higher ACVs, better cash flow, and fewer deals lost in payment term negotiations or internal delays.

Join the brands rewriting their revenue playbook. Schedule a free demo today and see what’s possible with our Closing Motion Platform.

Disclaimer: All insights in this post are based on publicly available data, vendor websites, and user reviews as of our latest research. While we've prioritized accuracy and relevance for B2B SaaS decision-makers, we recommend validating features, pricing, and fit through vendor demos and tailored consultations before making a final selection.

FAQs

1. How Do You Pay Back Non-Dilutive Funding?

Most non-dilutive options—such as venture debt, bank loans, and revenue-based financing—require repayment with interest or fees. While they don’t dilute equity, they still create liabilities.

Grants are the exception. Government grants are typically non-repayable and do not appear as debt.

In Ratio’s case, the structure is designed so that you do not have to repay the funds as a loan. Ratio operates on a structure where customer contracts are sold for upfront cash: you sell a customer contract and receive upfront cash. The customer, not you, repays Ratio over time.

The only exception is if the customer refuses to pay due to a commercial dispute (e.g., product failure or breach of contract). In that case, you may be required to repurchase the contract.

Read more here.

2. What Is the Role of AI in Underwriting?

AI in underwriting automates credit risk assessment by analyzing volumes of structured and unstructured data. This leads to faster, more accurate lending decisions. AI reduces manual work, shortens approval times, and enables real-time risk evaluation across individual transactions.

3. What Are Non-Dilutive Funding Companies?

Non-dilutive funding companies provide capital without requiring equity or ownership. They offer financing through structures like loans, credit facilities, revenue-based financing, or asset purchases. This lets founders retain full control while still accessing funds to grow.

There are two primary types:

1. Line-of-Credit Lenders

These firms lend money based on your recurring revenue (MRR/ARR).

- Structure: Credit facility (debt)

- Repayment: You draw funds manually and repay with interest

- Balance Sheet Impact: Shows up as a liability

- Best For: Runway extension, hiring, long-term investments

2. Closing Motion Platforms (e.g., Ratio)

These companies buy your signed contracts and pay you upfront.

- Structure: True Sale (not a loan)

- Repayment: Your customer pays them back over time

- Balance Sheet Impact: Designed to reduce balance sheet friction

- Best For: Closing deals faster, improving cash flow, and automating collections

Both are non-dilutive, but they serve very different functions.

4. What are Some Recurring Revenue Financing Providers?

Recurring revenue financing is a growing category, and while Ratio leads with embedded, deal-level capital activation, there are other players worth understanding.

Most providers fall into two camps:

- Line-of-credit lenders (like SaaS Capital), who fund based on your aggregate ARR after diligence and underwriting.

- Revenue-based financiers (like Lighter Capital), who offer smaller, non-dilutive advances with flexible payback tied to your cash flow.

Each has different implications for your runway, risk, and how fast you actually get cash in the door. Some focus on capital access. Others, like Ratio, focus on capital velocity.

👉 If you're comparing options, check out our full breakdown of 3 US-Based Recurring Revenue Financing Partners.

5. How Does Embedded BNPL Affect Deal Complexity or Legal Review?

Offering embedded BNPL—like Ratio—typically reduces complexity rather than adding to it.

- Contract Structure: There’s no third-party loan agreement. Buyers sign the vendor’s standard SaaS contract, with flexible payment terms embedded directly (e.g., “Quarterly Payments”). From the buyer’s perspective, there’s no new financing paperwork.

- Deal Complexity: BNPL aligns with procurement workflows. Instead of needing full budget approval upfront, buyers can match payments to their internal cash flow—removing common budget objections and speeding up approvals.

- Legal Review: Since the buyer isn’t taking on debt, there’s no new liability or credit agreement for legal teams to review. Ratio is optimized for standard contracts and minimal redlining.

Bottom line, buyers experience this as flexible terms from the vendor, not as external financing. That keeps the payment conversation aligned with the SaaS deal, ensuring cash flows as soon as the commitment is made.

.png)

.png)