Five Use Cases of B2B Embedded Finance for SaaS Businesses

SaaS businesses are always in the news for massive fundraising rounds and innovative product developments. However, beneath the surface, keeping SaaS businesses afloat isn't always a smooth sail. And if you're into B2B or enterprise SaaS, you're sailing against the high winds all the time.

An expensive prepaid contract value involves a longer sales cycle and a high drop-off rate. The pursuit of closing the deal faster compels you to offer hefty discounts. This causes a high customer acquisition cost (CAC) and a low annual contract value (ACV). And this is just one among many challenges.

Fortunately, the introduction of embedded finance in the B2B ecosystem has provided a better way for SaaS companies to address these challenges. A research report by Bain & Company predicts that transactions through embedded finance platforms will reach USD 7 trillion by 2026, indicating a tremendous potential for growth.

This article shares five impactful use cases of embedded finance for SaaS enterprises. But first, let's look at the concept of B2B embedded finance.

What Is B2B Embedded Finance?

B2B embedded finance is the integration of financial services, typically offered by banks and other financial institutions, into a non-financial enterprise's offerings and infrastructure within the B2B ecosystem. These financial services include banking, lending, payments, investing, and insurance.

For instance, a B2B embedded finance solution allows SaaS businesses to offer Buy-Now-Pay-Later (BNPL) flexibility to their customers, which can ultimately help them close more deals.

In the B2B SaaS ecosystem, while discounted lump sum pricing may look attractive, startups and SMBs may struggle to make upfront payments. This creates an undue friction point while closing deals.

Embedded finance solutions can offload these heavy upfront investments with various payment options.

Five Embedded Finance Use Cases for SaaS Businesses

A seamless purchase journey, faster deal closing and onboarding, and a smooth customer experience are obvious benefits B2B embedded finance solutions offer to SaaS businesses and their customers.

The rest of the article delves into the top five use cases of B2B embedded finance for SaaS enterprises.

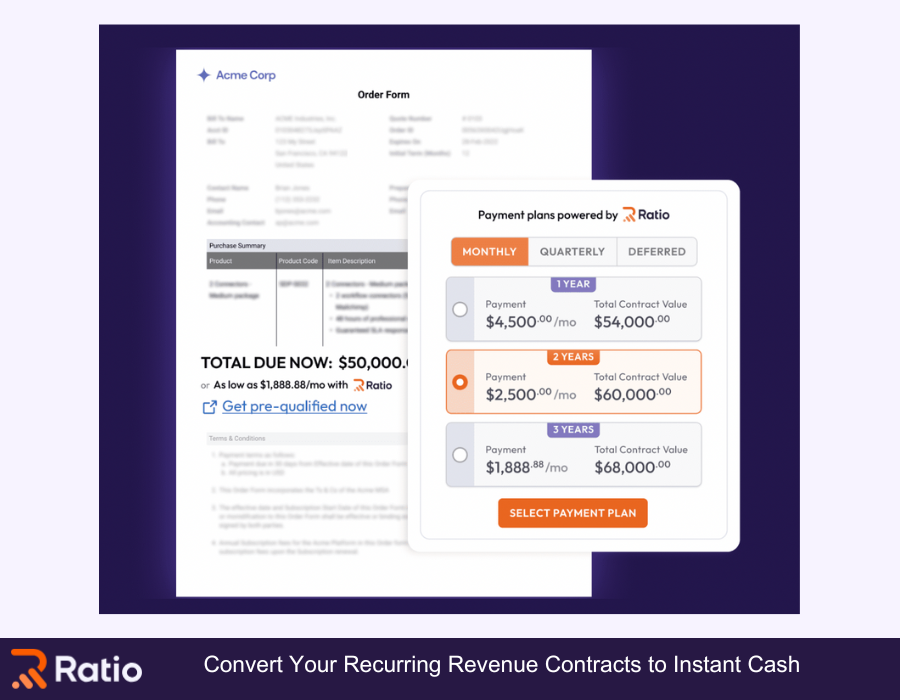

1. Offer Buy Now, Pay Later (BNPL) to Close More Deals

Buy-Now-Pay-Later (BNPL) is a common use case of embedded lending in the e-commerce and B2C space and is rapidly making its headway in the B2B SaaS ecosystem.

While essential, enterprise SaaS applications come with a high price tag. Shelling out thousands of dollars on a suite of products burdens startups and SMBs, creating a classic Catch-22 situation. Customers need your offerings but need the payment flexibility that uniquely matches their specific settings, and you need customers but can't discount to the extent of compromising profit margins.

B2B BNPL providers resolve this issue by allowing customers to pay a partial sum at the time of purchase and pay the remaining amount in monthly or quarterly installments. However, you receive the full contract value at the time of sale. The payment schedule is based on mutually agreed-upon terms and often interest-free.

You can use Ratio Boost, a BNPL platform, to customize an offer based on your client's business credit score, propensity and willingness to buy, probability of default, and debt-to-income ratio.

The customized contract price, payment terms, and schedules allow buyers to act faster, leading to a faster close. The flexible payment options mean you don't need to compromise on the ACV by offering hefty discounts just to close the deal.

BNPL providers are like a jetpack that remove the biggest objection to purchase and help B2B SaaS enterprises close deals faster, manage cash flow effectively, boost customer loyalty, and reduce churn.

2. Automate Billing and Collections

B2B payments are notoriously complicated. Manual payment processing and reconciliation for recurring payments is time-consuming, error-prone, and not to mention a major hassle. Howard Forman (Head of Digital Channels, PNC Treasury Management) calls it the swivel chair problem, where customers have to navigate between multiple systems to complete one task.

B2B embedded finance platforms integrate with accounting, banking, and payment software applications (see the full list of Ratio integrations for examples). This integration makes the embedded finance platform an interface between these three categories of apps. So, every time a customer pays through the banking or payment app, the transaction data is automatically recorded in the accounting system, making the process efficient and error-free.

Since the data is automatically updated, SaaS entrepreneurs always get real-time insights into the company's financial health.

And lastly, since the chances of discrepancies between the invoice and payments are low, the account reconciliation process is a walk in the park.

3. Access Capital at Almost 0% Financing Cost

Startups and SMBs have to plan their budgets carefully. When signing a contract with you, they would readily pick installment payments over an advance lump sum payment at a higher discount.

One of the main advantages of the B2B embedded finance platforms is that they meet both parties where they're at. So, although your customers continue paying monthly installments, you receive the full contract value at the beginning of the tenure.

For instance, if the total contract value is $100k, you receive the full amount right away, whereas the customer might pay $110k over a period of 12-36 months in monthly, quarterly, or bi-annual installments. As mentioned earlier, if you offload the financing fees to your customer, they are responsible for paying the additional fees of $10k. To quantify trade-offs for your situation, use our funding comparison calculator.

4. Opt for Invoice Financing for a Better Cash Flow

Overdue invoices are like the money that is there, but it isn't there. They hinder your cash flow visibility and can topple short-term growth plans or, worse, can stifle day-to-day operations.

For instance, you may have to dip your fingers into cash reserves to pay third-party vendors or freelancers that you had planned to spend on advertising. Small compromises like these create a domino effect that can push back your SaaS company's growth.

In such situations, you can opt for invoice financing or accounts receivable financing. In invoice financing, a B2B embedded finance platform acts as a lender to whom you sell your unpaid invoices. The platform pays 70%-90% of the invoice value to your account within 24-48 hours of receiving the invoice. The platform takes a cut and releases the remaining payment after receiving the full payment from your client or customer.

Similar to BNPL, invoice financing deposits cash quickly and isn't a form of debt financing. However, it's less flexible than BNPL, and the fees depend on the client's creditworthiness, so you pay higher fees if the client is a chronic late payer.

5. Get More Customer Insights

SaaS businesses spend an enormous time sifting through analytics, trying to uncover customer behavior, interests, and purchase patterns.

Working with a B2B embedded finance provider offers SaaS companies one more crucial touchpoint to understand their customers. While the ACV gives a macro view of customer needs, insights from the embedded finance platform enable you to get into the nitty-gritty.

For instance, if a client has opted for BNPL, you can view their tenure, installment frequency (monthly, quarterly, or bi-annual), and installment amount. This can help you understand their current financial situation and spending appetite.

With this information, you can customize the customer experience and plan when to pitch upsell or cross-sell offers. You can also predict at-risk customers if they happen to default on payments.

Being proactive in your approach can help you build a loyal customer base.

Pick Ratio as Your Embedded Finance Solution

Building a growing B2B SaaS has one key objective: streamline the cash flow without relying on venture debt or diluting your equity—use this guide to compare venture debt vs revenue-based financing to see how they stack up. Ratio Boost gives you access to capital by offering the BNPL option to your customers, allowing you to close more deals and optimize the CAC.

If you're wondering why Ratio is the best choice for you, here are a few compelling reasons:

- Availability of a capital pool of over $400M.

- Integrations with widely used banking, payments, and accounting software.

- Flexibility to pick only those customer contracts to sell that fit your needs.

- Top-notch security measures to keep your data safe, including traffic encryption using TLS v1.3 through RSA-2048.

- Peace-of-mind as Ratio bears the underwriting risk and is responsible for the collections.

- Swift approval process as fast as 48 hours due to dynamic underwriting.

While the BNPL process may seem lengthy, Ratio Boost ensures that you get your full contract value upfront as quickly as possible in five steps:

- Extend a customized offer to your prospect based on the payment terms, schedules, and contract price. You can do it through Ratio's standalone portal or embed it in your CRM tool.

- Wait (but not too long) for the contract approval. The dynamic underwriting process evaluates the client against risk metrics and determines the contract price.

- Be privy to the process at every step of the way. You can focus on creating value as the Ratio's self-close process automates deal closing.

- Get paid the full contract value in advance.

- Ratio integrates with your banking, payment, and invoicing applications. Don't sweat the billing and reconciliation process.

If you'd like to know how Ratio fits your needs, book a demo, or better, visit us at app.ratiotech.com!

.png)