Top Five Vendor Financing Companies: A Practical Comparison for B2B SaaS Teams

The Challenge: Payment flexibility has become a baseline expectation in B2B procurement. The problem is that extending terms without a financing partner means absorbing the cash flow gap yourself, and for growth-stage SaaS teams, that gap compounds quickly.

83% of B2B buyers walk away if payment terms are not available.

But even when vendors agree to offer that flexibility, the pressure does not go away.

64% of sellers report delays in getting paid, even after agreeing to terms.

That leaves B2B SaaS companies stuck between buyer expectations and cash flow needs. Vendor financing helps solve that gap. It lets you offer flexible payment terms to buyers while a third-party financing partner helps you get paid sooner.

In this guide, we’ll cover in much detail what vendor financing is, the challenges it solves, and the vendor financing companies you should consider partnering with to boost cash flow on every deal close.

Let’s get into it.

What vendor financing means

Vendor financing is when a seller offers flexible payment terms to a buyer like Net-30 or installments and receives the full payment upfront from a financing partner. The partner financing company takes on the risk, handles the collections, and gives the seller predictable cash flow from day one.

It’s like giving your buyers more time to pay without slowing down your revenue or straining your cash reserves.

We’ve already broken down the full basics: what vendor financing is, how it works, and why it’s so important for SaaS teams in this detailed guide on Vendor Financing for SaaS.

But let’s move past the definitions.

Demand for vendor financing has accelerated significantly in the past two years. Finance teams, RevOps leads, and sales organizations are all looking for ways to offer competitive payment terms without taking on the cash flow risk themselves.

Here's what's driving that shift.

Why More B2B SaaS Teams Are Turning to Vendor Financing in 2026

We talk to a lot of SaaS teams in demos, Slack channels, or finance forums, and one pattern keeps surfacing.

It's not that they don’t want to offer flexible terms. It’s that every time they try, something breaks.

- The deal gets stuck.

- The cash doesn’t arrive on time.

- The finance team panics.

- The growth plans stall.

It’s a cycle. And it’s one we’ve heard about too many times to ignore.

So let’s lay it all out.

Here are the core challenges B2B SaaS teams are wrestling with, the ones that are pushing them toward vendor financing now, not later:

1. Buyers Are Demanding Longer Payment Terms, and it’s Straining Sellers

According to PYMNTS, extended payment cycles are becoming increasingly common in B2B, particularly among large buyers. These extended terms are now actively impacting supply chain stability and putting financial pressure on smaller vendors. Here’s what this looks like on the ground:

SaaS teams are being asked to agree to Net-60, Net-90, or even Net-120 terms just to stay in the deal conversation. And it’s not just a few outliers, it's becoming normalized across industries where procurement has leverage.

In a recent Reddit thread, several business owners shared how even “Net-30” now feels rare.

When that happens, here’s what it means for the vendor: You're delivering your product or service now. Your team is doing the work, onboarding the client, and delivering support. But the cash doesn't hit your account for two or three months. Sometimes more.

This delay ties up working capital, forces finance teams to forecast with uncertainty, and limits your ability to reinvest in growth.

Vendor financing addresses this directly — it allows vendors to agree to extended terms without absorbing the cash flow delay. The financing partner steps in at the moment of contract, not after collections.

2. Most B2B Payments Are Late, Even When Terms Are Clear

According to Financial IT, more than 50% of B2B invoices are paid late, regardless of whether the agreed term is Net-30 or Net-60. This pattern creates recurring gaps in cash flow and disrupts financial predictability for vendors.

This means even when SaaS vendors try to protect themselves with standard terms, the actual payment still arrives late. Sometimes 10 days late. Sometimes 30. And when multiple invoices are delayed across multiple accounts, the financial strain builds fast.

Your product has already been delivered. Your team has moved on to supporting and retaining the client. But your finance dashboard is still waiting for that payment to clear.

This isn’t just an accounting problem. It turns into a strategic roadblock. Forecasting becomes harder. Cash reserves drop. And the cost of capital rises because the money you’ve already earned still hasn’t arrived.

Vendor financing locks in cash flow predictability regardless of buyer payment behavior. The financing partner assumes collections responsibility, removing that operational burden from the finance team entirely.

3. Cash Flow Timing Is Out of Sync With How SaaS Teams Grow

According to Intuit QuickBooks, nearly 73% small and mid-sized B2B companies experience payment delays that impact their working capital. But it’s not just the delays, it’s the mismatch between when revenue is booked and when cash actually arrives.

For SaaS companies, this gap is especially risky.

You spend upfront on sales efforts, onboarding, engineering, and support, but the cash often arrives much later. Even when buyers technically pay “on time,” you’re still carrying the delivery cost weeks or months before money hits your account.

This creates a timing mismatch that slows growth. You want to reinvest into new hires, GTM initiatives, or product development, but you can’t, because your working capital is locked in unpaid invoices.

Finance leaders are forced to choose between slowing momentum and relying on external credit just to stay on track.

This is where vendor financing becomes a strategic lever. It converts contracted revenue into immediate capital at close — eliminating the timing mismatch between when work is delivered and when cash arrives. Finance teams can reinvest in growth without waiting on collections cycles.

4. Offering Custom Terms Creates Operational Drag Across Teams

According to Modern Treasury’s 2025 State of Payment Operations, 68% of financial decision-makers agree their teams waste significant time on payment operations due to system sprawl and manual workflows.

Here’s how it plays out in SaaS teams:

To close a deal, sales offers custom terms, maybe Net-60, milestone-based billing, or a deferred start date. But now the rest of the company has to support that promise.

- Finance is forced to manually create and track unique invoices

- RevOps struggles to forecast with fragmented timelines

- Collections teams chase different buyers across different schedules

It turns what should be a win, i.e., payment flexibility, into an internal operational mess.

Instead of scaling, teams are stuck reconciling spreadsheets, wrangling 6–7 different tools, and trying to avoid billing errors. That’s time lost. Accuracy risk. Burnout fuel.

Vendor financing standardizes this entirely. The financing partner owns the complexity of custom term management — the vendor's internal workflows stay consistent regardless of what terms the buyer receives.

You’d probably agree; payment flexibility has become a must if you want to close B2B SaaS deals faster. But offering it on your own, without a financing partner, can quietly hurt. That’s why it’s worth looking at both sides of the equation: What payment flexibility looks like with (and without) a BNPL partner

5. Requiring Full Payment Upfront Often Slows or Kills Deals

A common pattern in SaaS deal cycles: the buyer is qualified, the product fits, and the deal stalls at procurement because a lump-sum payment isn't feasible given the buyer's budget structure or approval process.

It’s not that your solution isn’t valuable. It’s that your buyer has budget approvals, cash flow timing, or internal policies that make a lump-sum payment unrealistic.

The result? Longer deal cycles. More drop-offs at procurement. And finance leads are pushing back on sales.

Vendor financing restructures the close. The buyer receives terms aligned to their budget cycle — Net-30, Net-60, quarterly, or milestone-based. The vendor receives the full contract value upfront. Payment risk transfers to the financing partner.

If you want to explore this topic deeper, we’ve also broken down the real pros and cons of requiring upfront payment in another Ratio piece.

With those drivers established, the next question is how vendor financing actually works in practice. There are four distinct models (ranging from self-financed trade credit to fully managed BNPL) each with different risk profiles, operational requirements, and fit for different stages of growth.

How Vendor Financing Actually Works: 4 Real Options for SaaS Teams

Not all vendor financing is created equal. Depending on how much control you want, how fast you need cash, and how much risk you’re willing to carry, there are a few ways to give buyers flexible terms without breaking your balance sheet.

Let’s walk through the four main vendor financing models B2B SaaS teams are using today, from DIY to fully automated:

1. Self‑Financed Net Terms (Trade Credit)

What it is:

You offer buyers the ability to pay in 30, 60, or 90 days — but you’re the one waiting to get paid. It’s the default model in B2B, especially in early-stage or low-complexity deals.

Pros:

- Builds buyer trust and deal momentum

- Keeps payment control in-house

- Simple to implement without external tools

- Can improve the win rate when buyers are hesitant

Cons:

- Delays your cash flow — sometimes by 60+ days

- You absorb the risk of late or non-payment

- AR management becomes a time sink

- Chokes working capital during growth phases

Best For:

Early-stage SaaS teams with a limited number of accounts

2. Invoice Factoring (Accounts Receivable Financing)

What it is:

You sell your issued invoice to a financing company (called a “factor”) for a percentage of its value upfront. The factor then collects from the buyer directly.

Pros:

- Unlocks cash quickly from outstanding invoices

- Reduces manual collections burden

- Doesn’t require taking on debt

- Let’s you fund growth from completed work

Cons:

- You lose a portion of the invoice as a fee

- Margins erode with overuse

- Not all invoices are eligible (high-risk buyers often excluded)

- May affect customer relationships if collections feel aggressive

Best for:

SaaS teams with large invoiced deals and delayed receivables

3. B2B Buy Now, Pay Later (BNPL) via Financing Partners

What it is:

A BNPL provider pays you the full contract amount upfront and offers your buyer a flexible repayment schedule (e.g., 3 to 6 monthly installments). The provider owns the repayment and collection risk.

Pros:

- You get paid upfront — no AR drag

- Buyer gets the flexibility they want

- Removes friction from deals that stall due to cost

- Offloads credit checks, collections, and late payment risk

Cons:

- You pay a service fee (usually 2–6%)

- Some tools require integration into your workflow

- Credit decisions might exclude some buyer profiles

- Availability varies across markets or jurisdictions

Best for:

Growth-stage SaaS teams aiming to close faster and eliminate payment friction

4. SaaS-Specific Credit Lines (a.k.a. Revenue-Based Financing or Working Capital Advances)

What it is:

You access capital based on your ARR, MRR, or signed contracts. Unlike BNPL, this financing is for your internal operations — not tied to a specific customer invoice. Providers like Capchase, Arc, and Founderpath underwrite SaaS metrics directly.

Pros:

- Non-dilutive funding without venture capital

- Underwritten based on real-time SaaS metrics

- Scales as you grow (contracts or revenue-based)

- Repayment often flexes with monthly cash inflow

Cons:

- Repayment is still your responsibility

- Can get expensive if revenue fluctuates

- Adds liabilities to your balance sheet

- Not a direct solution for offering terms to customers

Best for:

SaaS companies needing cash to invest in GTM, hiring, or product, not to finance customer deals

Each of these vendor financing models we just explored comes with trade-offs. But the good news: you don’t have to build or manage these models yourself.

Whether you’re looking to offer net terms, split payments, or upfront cash flow against contracts, there are specialist companies designed to handle the complexity for you.

They take care of risk, operations, and compliance so your team can stay focused on growth.

Let’s take a closer look at the top vendor financing companies that bring these models to life for B2B SaaS teams in 2026 and what makes them stand out.

Top Five Vendor Financing Companies for B2B SaaS Teams in 2026

(For B2B SaaS Teams Looking to Close Deals Faster, Get Paid Upfront, and Offload Risk)

The following section evaluates the five vendor financing companies most relevant for B2B SaaS teams in 2026: covering what each platform does, who it's best suited for, and where the trade-offs lie.

This section breaks down the top vendor financing companies shaping how SaaS businesses offer flexible terms, secure upfront payments, and de-risk their cash flow in 2026.

We’ll cover what each platform does, who it’s best for, the model they use (BNPL, cash advance, AR automation, etc.), and what to watch out for — so you can choose the right fit for your sales motion, cash flow needs, and ops maturity.

Here’s a quick look at the companies we’ll cover:

- Ratio

- Capchase

- Pipe

- Tranch

- Resolve

Let’s explore each one by one.

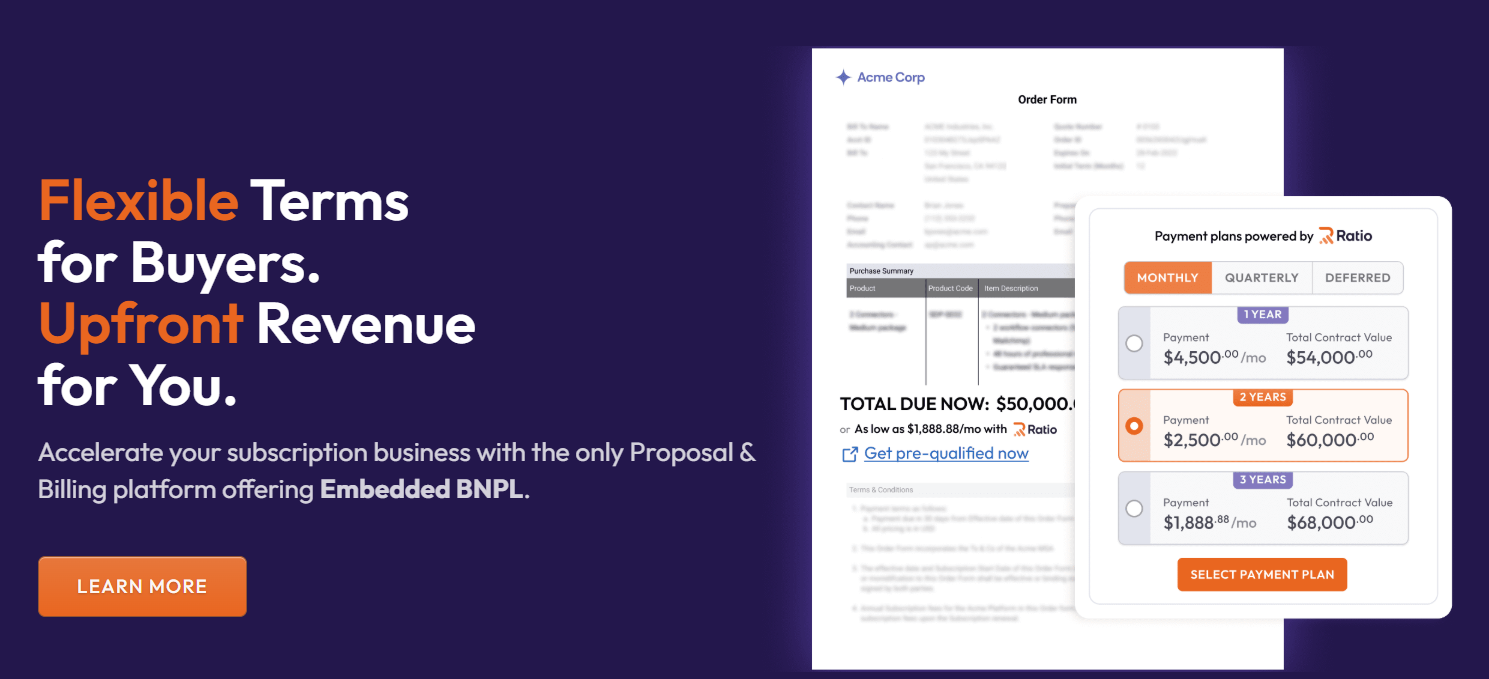

1. Ratio

Ratio is a vendor financing platform built specifically for B2B SaaS revenue teams. Its core product, Boost, functions as a Closing Motion Platform — it integrates at the proposal stage, embeds BNPL so buyers can pay over time while vendors receive full payment upfront, and keeps renewals and collections connected in a single workflow. The result is a reduction in the fragmented handoffs that typically slow the path from signed contract to cash.

Boost isn’t just a financing add-on. It’s a full-stack quote-to-cash engine that integrates into your sales flow, automates approvals, and unlocks cash at the moment of contract — without delays, discounting or dilution.

Best For:

- SaaS, RaaS, and subscription-based businesses

- Sales-led or hybrid GTM teams with long sales cycles

- Finance teams looking to eliminate receivables and optimize cash flow

Business Models Served:

- B2B SaaS

- Robotics / Hardware + Service Bundles

- Channel & VAR sales

- Usage-based or milestone billing models

Strengths:

- Embedded BNPL at quote stage — financing is offered as part of the deal, not after it

- Quick underwriting — 87%+ approval rate for qualified buyers

- Instant cash at close — sellers get almost all contract value upfront

- No buyer disruption — buyers get their flexible terms, sellers get their cash

- True Sale accounting — receivables move off books, risk is offloaded

- Custom term configurations — buyer pays, seller pays, or shared cost

Considerations:

- Primarily focused on U.S.-based SaaS and mid-market+ vendors

- Best suited for teams with some sales volume or quoting infrastructure in place

- Setup works best when integrated with CRM, CPQ, or billing systems

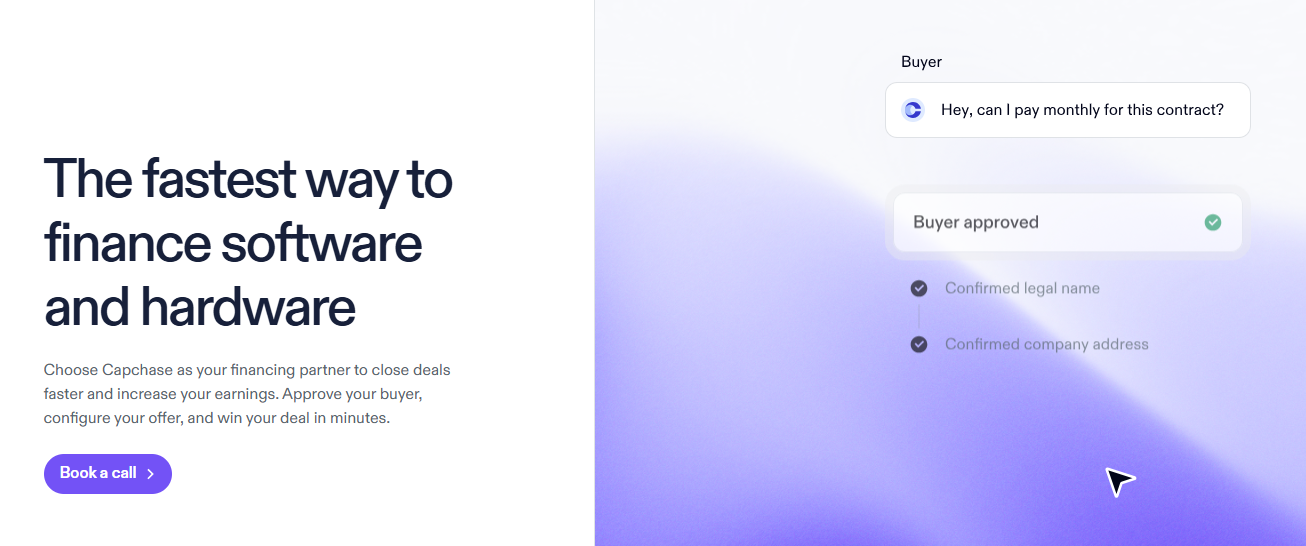

2. Capchase

Source: capchase.com

Capchase is a global embedded financing platform that helps vendors close deals faster by offering flexible payment terms—without delaying cash flow. Through real-time buyer qualification, dynamic deal configuration, and white-labeled financing experiences, Capchase powers everything from monthly payment plans to multi-year contracts.

It’s built for scale and speed — turning what used to be multi-week contract financing into a quick workflow inside your CRM.

Best For:

- Mid-market to enterprise vendors in software, hardware, or IT services

- Sales teams with high volume or high complexity deals

- Companies selling through resellers or partner channels

Business Models Served:

- B2B SaaS and software

- IT hardware and infrastructure

- Reseller and distributor networks

- Multi-year and milestone-based contracts

Strengths:

- Fast buyer approval — qualify buyers in minutes, even during live calls

- Custom financing options — term length, payment frequency, and subsidies

- Embedded inside sales stack — works within Salesforce, Slack, and Teams

- White-labeled experience — build a branded captive financing program

- Multinational coverage — supports vendors and buyers across 9+ countries

- Partner-ready — designed for both direct sales and channel partner deals

Considerations:

- Tailored more toward established teams with high sales motion maturity

- Works best when integrated into CRM and deal ops systems

- May not be as flexible for smaller SaaS teams with leaner workflows

3. Pipe

Source: pipe.com/products/capital

Pipe is an embedded capital platform that helps vendors give their customers fast, flexible working capital—without taking on risk, compliance, or operational overhead themselves. It's built to power growth for both vendors and their customers through white-labeled, multi-draw capital access that feels seamless.

Unlike traditional revenue trading (which Pipe was once known for), the platform now focuses on embedded capital infrastructure. That is letting companies offer financing to their own customers, while Pipe handles eligibility, underwriting, payouts, and collections.

Best For:

- SaaS or tech platforms looking to embed capital offers into their product or sales flow

- Teams that want to offer payment flexibility without holding risk

- Vendors that serve SMBs or mid-market businesses with cash flow constraints

Business Models Served:

- B2B SaaS

- Marketplaces

- Vertical software platforms

- Fintechs enabling financing for their customers

Strengths:

- Embedded financing experience with full white-label control

- Sales-based payments and pre-approved capital offers for your buyers

- Multi-draw & renewal options keep customers funded longer

- 98%+ approval on pre-qualified offers, expanding eligibility

- Full GTM support including onboarding, customer support, and co-selling

- No need to handle compliance, risk, or collections. Pipe manages it all

Considerations:

- More suitable for platforms and marketplaces, not individual vendors

- Integration requires product and ops alignment with your customer journey

- Revenue sharing or pricing models may vary depending on use case

- Best suited for vendors with sizable, recurring buyer traffic or B2B checkout volume

4. Tranch

Source: tranch.com

Tranch is a B2B payments and financing platform helping service providers get paid upfront while offering their clients flexible payment options like Pay Now, Pay Later, or Pay by Card. It’s built to work across industries that often suffer from long payment cycles—like legal, accounting, marketing, and software development firms.

Best For:

Service-led businesses that invoice clients for large, project-based engagements or retainers—especially firms that face delayed payments or prefer not to chase collections.

Business Models Served:

- Law firms

- Accounting & finance consultancies

- Marketing & creative agencies

- SaaS and IT services

- Any high-ticket B2B service business

Strengths:

- Zero credit risk — Tranch underwrites and assumes all credit risk for the “Pay Later” model.

- Flexible payment choices — Clients can split invoices over 2–12 months, pay by card, or choose up-front payment.

- Upfront payouts — Sellers are paid the full invoice value at the time of sale.

- ERP & AR integration — Connects directly with systems like Xero, QuickBooks, and others for reconciliation.

- Improved payment behavior — Tranch claims its partners get paid 40% faster, see a 50% reduction in checks, and work with clients averaging £1.5B in annual revenue.

Considerations:

- Tranch is most optimized for professional services; product-centric businesses may not see full platform fit.

- Limited public information on pricing or approval thresholds.

- Current operations appear UK- and EU-focused, though expansion to other regions is in progress.

5. Resolve

Source: resolvepay.com

Resolve is a B2B net terms and credit management platform that empowers vendors to offer flexible payment terms (like Net-30 or Net-60) while still receiving payments upfront. It's essentially a B2B BNPL (Buy Now, Pay Later) platform embedded with AI-driven accounts receivable automation.

Best For:

B2B vendors looking to scale operations with net terms, automate AR, and reduce credit risk while offering buyers flexible payment options.

Business Models Served:

B2B merchants, manufacturers, distributors, and suppliers operating on invoicing and net terms.

Strengths:

- Instant credit decisions with AI-powered underwriting that delivers real-time approvals for smoother buyer onboarding

- Upfront cash advance where vendors can receive up to 100% of invoice value in just 1–2 business days

- Fully automated AR using AI agents to handle invoicing, collections, and credit monitoring with minimal internal effort

- Embedded in payment stack with easy integration into ERP, ecommerce, and accounting systems

- Boosts revenue by increasing AOV up to 40% and helping clients achieve 20% YoY sales growth

Considerations:

- It’s great for invoice-based businesses but may not suit subscription-heavy SaaS models directly.

- While integrations are strong, implementation might require upfront effort for complex stacks.

- Vendors may need to adjust internal workflows to reflect changes in collections and payment flow.

We’ve unpacked what each of these vendor financing companies brings to the table — but how do they really stack up side by side? A quick comparison can tell.

Quick Comparison Table: Top Vendor Financing Companies for SaaS in 2026

Here’s a side-by-side snapshot of the most important details across the top companies we covered. You can quickly zero in on what fits your business:

From embedded terms to real-time approvals, each company offers something different. But Ratio clearly stands out by treating financing as part of the broader closing motion, helping vendors turn signed deals into cash upfront they can use to keep growth moving.

Why Choose Ratio Over Other Vendor Financing Companies in 2026

Let’s talk about proof.

DearDoc is a B2B SaaS company selling to medical practices — a buyer segment with genuine budget constraints and limited ability to commit to large annual payments upfront. After implementing Ratio Boost, they were able to offer monthly and quarterly payment terms while receiving full contract value at close.

With this closing motion platform Ratio Boost, DearDoc saw:

- 30% faster deal closure

- 25% increase in ACV

Not bad, right?

Several additional capabilities are worth noting for finance and RevOps teams evaluating Ratio:

- Proprietary underwriting engine — real-time risk scoring beyond standard credit checks, with decisions in under one second and an 87%+ approval rate for qualified buyers

- $411M+ in committed funding capacity [VERIFY/SOURCE] — no approval delays at the deal level

- Stack integration — works within Salesforce, HubSpot, CPQ tools, and Slack

- Real-time deal tracking — a single visibility layer across sales, finance, and RevOps

- White-labeled buyer experience — Ratio operates in the background; the vendor's brand remains front-facing

If your team is evaluating vendor financing options and wants to understand how Ratio Boost fits your specific sales motion and cash flow needs, a 15-minute conversation is a reasonable next step.

Book a 15-minute strategy call and see how Ratio Boost helps you turn a buyer’s yes into cash upfront.

Disclaimer: We have compiled this guide using information available on company websites, public materials, and third-party review sources. While we have done our best to keep the information accurate and up to date at the time of writing, product details, pricing, eligibility, and features may change. We recommend visiting each provider’s official website, speaking with their team, and requesting a demo before making a final decision.

.png)