Top 5 BNPL Companies Compared: Find the Perfect Buy Now, Pay Later Partner for Your SaaS Business

🚨 The Challenge: Most BNPL Tools Break Under SaaS Complexity

Selling SaaS with flexible terms? Then BNPL might seem like the next smart move. A way to close deals faster and unlock predictable cash flow. But most BNPL tools like Affirm, Klarna, and even many B2B providers were built for one-time checkouts, not SaaS.

And SaaS is anything but static.

You’re managing:

🔁 Subscriptions

⬆️ Upgrades

📊 Usage-based billing

🔄 Renewals, churn, reactivation

💸 Flexible terms across long sales cycles

When BNPL companies don’t understand that, things break. You’re left with delayed revenue, accounting messes, and new sales friction.

👇 This guide breaks down common mistakes SaaS teams make when choosing third party BNPL companies for their SaaS sales. You’ll see what to look for in BNPL companies. And most important, how modern providers like Ratio go beyond standalone BNPL and connect financing directly to the sales workflow.

Let’s dive in.

🚫Before You Choose: Where SaaS Teams Go Wrong in Picking BNPL Companies

BNPL can be a powerful growth lever. But only if you understand what it really is.

Many SaaS teams approach BNPL with the wrong assumptions. They treat it like a payments feature, expect zero risk, or assume it works just like eCommerce.

But B2B BNPL, especially for SaaS, is far more than checkout tech. It is financing infrastructure that touches risk, revenue recognition, and customer experience.

When teams misunderstand how it works, they don’t just pick the wrong partner. They create hidden risk in their sales, finance, and RevOps processes.

👇 Let’s break down the three most common mistakes SaaS teams made while choosing BNPL and how to avoid them.

⚠️ Mistake #1: Evaluating BNPL Like a Payments Tool Instead of a Financing Decision

Many SaaS teams evaluate BNPL like a checkout plugin. They focus on buyer experience, speed, or fees. But BNPL is a financing decision, not just a payment feature.

When you use BNPL, you are outsourcing credit risk, cash flow timing, and part of the post-sale relationship. The wrong partner can delay payouts, disrupt your customer experience, or create confusion for your finance team.

✅ Avoid it: Treat BNPL like infrastructure. Ask: Who underwrites the deal? Who owns the contract after checkout? How does the structure affect cash flow and customer experience?

⚠️ Mistake 2: Assuming BNPL Automatically Removes Risk From Your Books

Many SaaS teams assume BNPL eliminates risk entirely. In practice, some providers still tie payouts to buyer repayment. Others introduce clawbacks if customers churn or default.

Some structures also resemble accounts receivable financing rather than a true receivables sale. In these cases, your cash flow may still depend on collections.

✅ Avoid it: Ask direct questions. When do we get paid? Is the structure non-recourse? Are there clawbacks tied to repayment performance?

Recommended Read: Clawback Commissions Explained: Strategies for SaaS Sales Leaders

⚠️ Mistake 3: Ignoring the Complexities of SaaS Revenue

Many BNPL solutions were designed for one-time invoices. SaaS revenue is different.

Customers upgrade plans. They change seat counts. They cancel early or shift usage patterns. Contracts evolve over time.

If the financing model cannot handle these changes, billing mismatches and revenue recognition issues may appear.

✅ Avoid it: Choose a BNPL provider that supports subscription logic, mid-contract changes, and usage-based pricing. Integration with your CRM and billing systems also helps ensure financing mirrors how your revenue actually works.

These are just a few common BNPL mistakes and how to fix them. To make it even easier, we’ve created a quick checklist. Use it to spot if the BNPL companies you are choosing aren't built for SaaS. If several points sound familiar, that’s a red flag.

🔎 Quick Checklist: Signs a BNPL Provider Wasn’t Built for SaaS

If a provider shows one or more of these signs, it may not be designed for SaaS use cases.

- ❌ Only supports fixed, one-time invoices

- ❌ No ability to handle subscription upgrades, downgrades, or renewals

- ❌ Manual underwriting that slows down deal velocity

- ❌ Clawbacks or payment delays tied to buyer churn or default

- ❌ No integrations with your CRM or billing systems

- ❌ Doesn’t support usage-based or variable pricing models

- ❌ Treats contracts as static — not as evolving revenue relationships

🧠 Why it matters: These gaps may not appear during a product demo. But they often surface later in finance operations, cash flow management, and the customer experience.

But let’s shift gears now. Because the best BNPL providers today aren’t just avoiding problems, they’re unlocking real growth.

👇Let’s see what modern, SaaS-ready BNPL companies actually look like.

📌More Than Just BNPL: What Modern BNPL Companies Offer SaaS Teams Today

The early version of BNPL focused on one idea. Let the buyer pay later. For SaaS companies, that alone is not enough.

Today’s best BNPL providers go much further. They help SaaS teams approve buyers instantly, tie financing to real-time product usage, and automate billing, collections, and reconciliation in the background.

And this evolution isn’t just happening quietly; it’s driving massive adoption. According to Bain & Company, embedded finance is expected to exceed $7 trillion in U.S. transaction value by 2026, with BNPL playing a major role.

🤔So what does that actually look like for SaaS teams in practice?

👇Here’s what the most advanced BNPL companies are offering today:

💵 Upfront Capital That Fuels Growth

BNPL isn’t just for your buyer’s flexibility; it’s a working capital unlock for your business.

Modern providers:

- Advance the full contract value upfront

- Let buyers pay over time without delaying your revenue

- Eliminate the need for discounting to close annual deals

📢Why it matters: You improve cash flow, reduce revenue risk, and unlock larger, longer-term deals without compromise.

💡 Embedded Financing Within the Sales Process

Traditional BNPL appears at checkout after the deal is finalized. Modern platforms integrate earlier, embedding financing inside your quote-to-cash flow.

They enable:

- Pre-approved financing options inside CPQ or quoting tools

- Instant decisioning based on buyer profile or contract size

- Automated invoicing, reconciliation, and collections post-close

📢Why it matters: Sales, finance, and RevOps stay in sync and you get paid faster, without manual ops or SaaS tool sprawl.

📊 Revenue-Driven Underwriting, Not Just Credit Scores

Legacy BNPL evaluates risk using outdated models like credit scores and static financials. Modern providers assess risk using live business signals, such as:

- Product usage and engagement behavior

- Contract structure and renewal patterns

- Payment history from your billing system or CRM

- Churn risk benchmarks and industry-specific repayment data

📢Why it matters: You get faster, smarter approvals — aligned with how SaaS buyers actually operate, not outdated credit files.

✨ A Branded Buyer Experience That Feels Native

Old-school BNPL disrupts your buyer journey with external portals and lender branding. Modern solutions embed financing inside your flow — and keep your brand front and center.

They offer:

- White-labeled flows on your domain with your design

- Embedded financing within quotes, invoices, or proposals

- Approval flows aligned to your sales tone and UX

Why it matters: Your buyer never leaves your experience; increasing trust, conversion, and deal velocity.

You’ve seen what the best BNPL providers bring to SaaS teams. But, how do you separate a truly SaaS-ready BNPL partner company from one that just looks good on paper?

👇This scorecard makes it simple.

📝 The BNPL Fit Scorecard: What to Look for in a SaaS-Ready BNPL Company

When SaaS teams evaluate BNPL companies, most stop at surface-level questions — “How fast is approval?” or “What’s the fee?”

But BNPL isn’t just a payment feature. It’s an operational and financial lever. That directly impacts how quickly you close deals, how smoothly you collect revenue, and how healthy your balance sheet looks.

Use this BNPL Fit Scorecard to evaluate whether a partner is truly built for SaaS — and what kind of impact each capability can have on your business:

Note: If a BNPL provider falls short in even one of these areas, the consequences won’t stay hidden. You’ll feel it in slower deal cycles, unpredictable cash flow, and added strain on your team.

You need providers who perform well across these criterias.

So next, let's break down the top BNPL companies for B2B SaaS businesses. Based on this you can make a correct choice of the one that actually fits your needs.

🔎 Top Five BNPL Companies Built for B2B SaaS

By now, you understand what a SaaS-ready BNPL partner should offer and not all BNPL providers are built the same.

Some nail embedded financing but can’t handle contract upgrades. Others promise fast payouts but leave your RevOps drowning in manual work.

That’s why we’ve done the digging for you🕵️♀️.

In this section, we break down five leading BNPL providers and how they perform where it counts: SaaS readiness, integration depth, contract flexibility, risk transfer, and cash flow timing.

Here’s the lineup:

- Ratio

- Capchase

- Tranch

- Resolve

- Balance

Let’s begin with the #1 SaaS-specific BNPL companies:

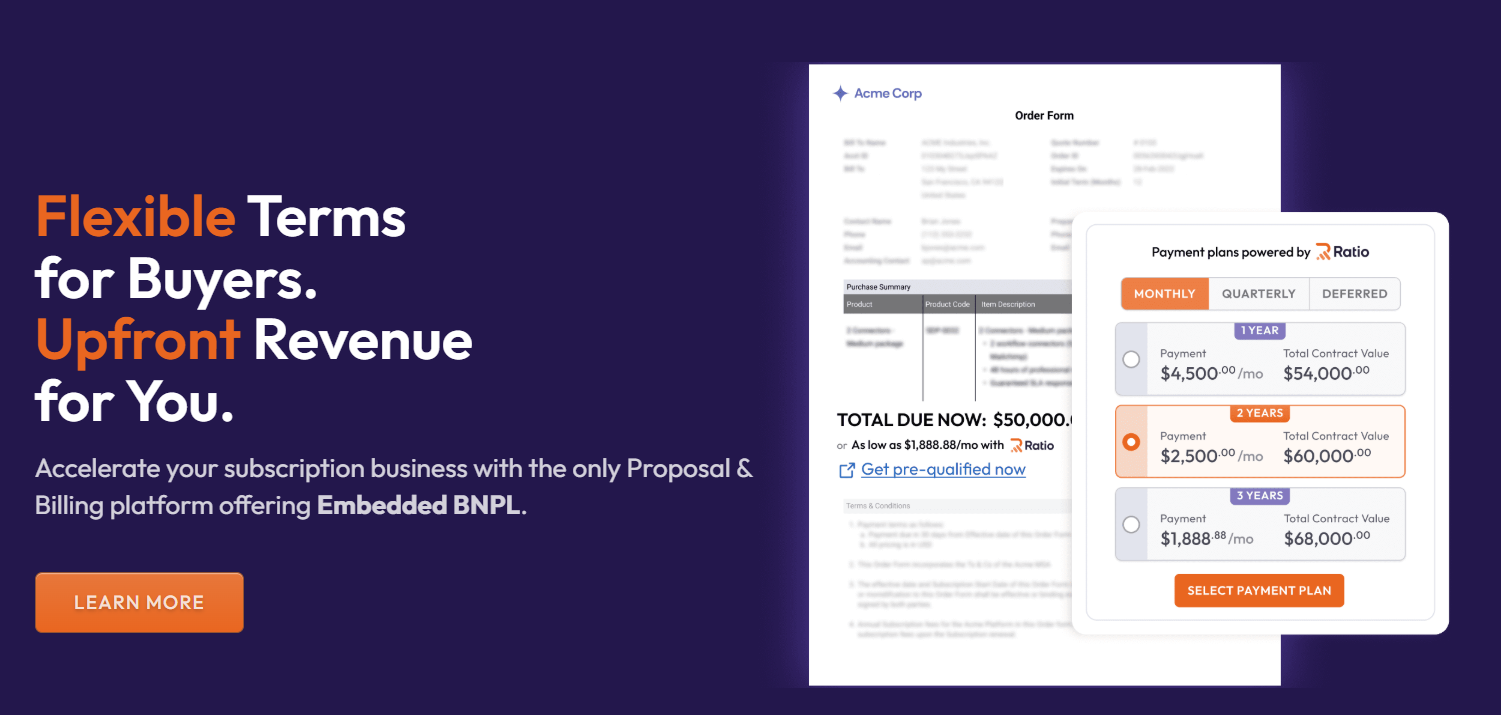

1. Ratio

Ratio is a U.S.-based company building the Closing Motion Platform for B2B technology scale-ups selling subscription or recurring products.

Its product, Ratio Boost, enables buyers to pay over time while sellers can receive cash upfront on approved deals. The platform connects proposals, BNPL payments, renewals, and collections into a single workflow.

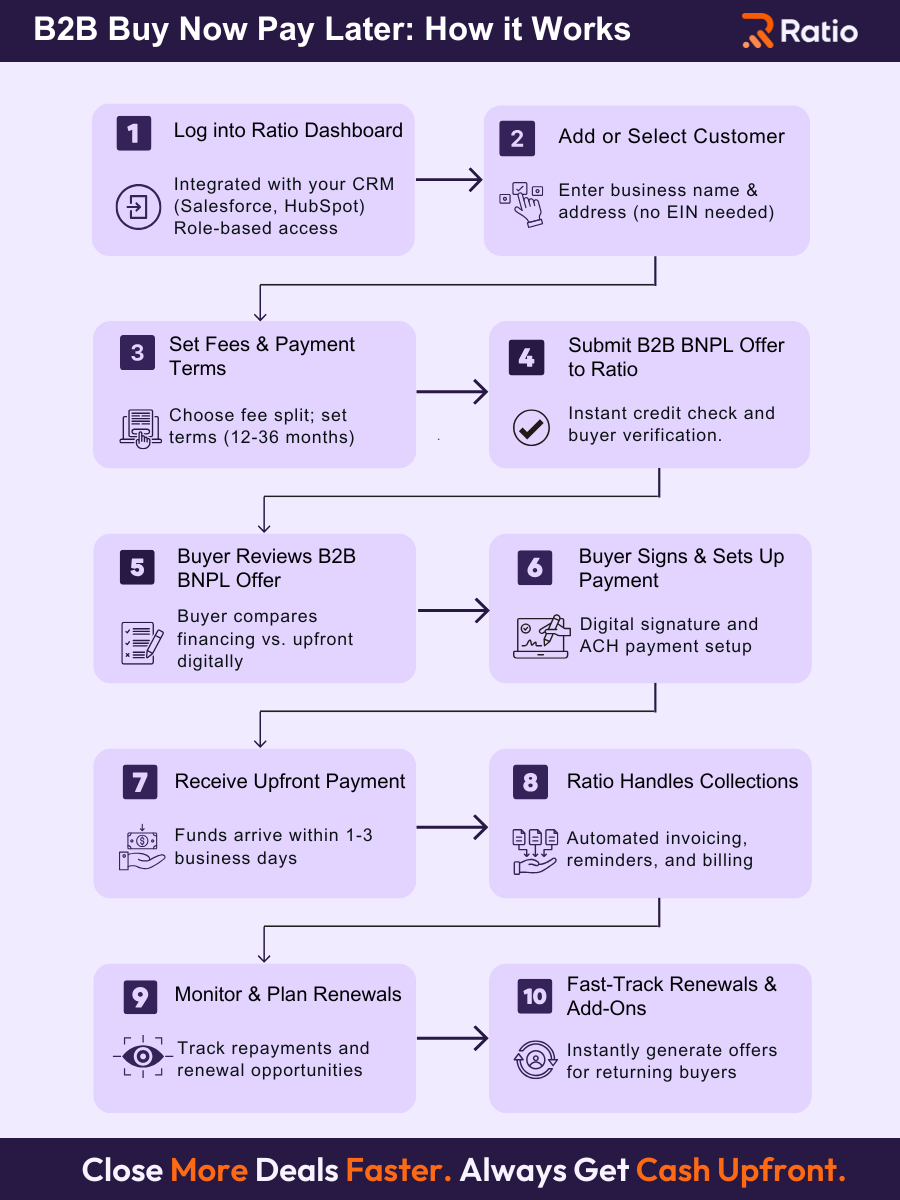

🔍 Here’s how you can implement Ratio Boost in your workflow - with 10 easy steps:

🛠️ Key BNPL Features & Benefits of Ratio Boost

What makes Ratio Boost useful for SaaS and services teams? These are the core features that set it apart:

- SaaS-Ready Contract Support : Built for recurring revenue. Supports subscription contracts, service agreements, renewals, and upsells — not just one-time invoices.

- Payment Flexibility: Buyers can pay monthly, quarterly, or on custom terms aligned with their internal budget cycles. Helps close larger and longer-term deals.

- Configurable Financing Fees: You can decide who covers the financing cost: your company, the buyer, or a 50/50 split. This gives you flexibility in how you position offers and preserve margin.

- Buyer-Friendly Digital Experience : Buyers get a clean, branded experience where they can compare plans and finalize payments digitally. Builds trust and speeds up decision-making.

- Full Upfront Payout: You receive the full contract value within days after the buyer’s first payment clears, improving cash flow without waiting for installments.

- Billing and Collections Management: Ratio manages invoicing, reminders, and collections automatically, removing the operational burden from your finance and AR teams.

- Repayment Tracking Dashboard : Live dashboard shows repayment status and buyer actions. Helps teams time renewals, follow-ups, and upsells with confidence.

📊 Trying to decide between loans, RBF, or BNPL? Use our Funding Comparison Calculator to find the smartest option for your cash flow and margins.

🔌Integrations & Tech Stack Compatibility of Ratio Boost

Ratio Boost integrates with commonly used systems across CRM, billing, accounting, and payments to support existing SaaS sales and finance workflows.

- ✅ Accounting: QuickBooks (Online & Desktop), NetSuite, Xero,

- ✅ Banking: Plaid

- ✅ CRM: Salesforce, HubSpot

- ✅ Subscription Management: Chargebee, Recurly, Chargify

- ✅ Payments: Stripe, GoCardless, ACHQ

🚀 Customer Success Story: A HST customer

A fast-growing SaaS provider was struggling with long deal cycles, deep discounts, and slow cash flow. It adopted Ratio Boost to offer flexible BNPL terms while still getting paid upfront.

Results:

- 60% faster deal closures

- 10% increase in closed deals

- Eliminated heavy discounting

- Improved cash flow with upfront payments

- Higher customer satisfaction and retention

💰 Ratio Boost’s Pricing

- 🆓 No monthly platform fees

- 💸 Only pay a loan/lending management fee when a deal is funded — with full flexibility to either absorb the cost, split it with the buyer, or pass 100% of it to the buyer at checkout.

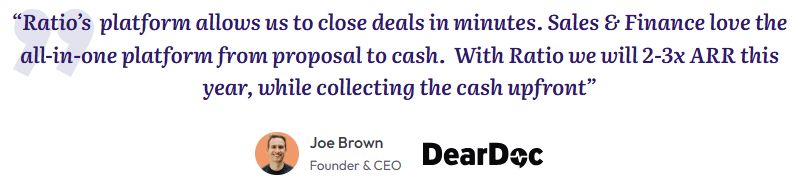

🗣️ Client Testimonial

Early adopters of Ratio are already seeing powerful results.

Take it from Joe Brown, Founder and CEO of DearDoc:

🧪 Demo/Trial Availability

- Personalized live demo and expert consultation available within 24 hours

2. Capchase

Capchase is one of the BNPL companies that focus on B2B SaaS and software vendors. Its product, Capchase Pay, enables sellers to offer extended payment terms—typically up to 12 months—while receiving upfront payment. The product is part of Capchase’s broader financing suite and is designed to reduce friction in the sales process, support cash flow, and provide an alternative to heavy discounting.

Capchase has expanded its capabilities to include embedded financing experiences and more flexible B2B transaction support.

🛠️ Key BNPL Features & Benefits of Capchase

Below is a closer look at what Capchase offers:

- Instant Buyer Qualification: Approves buyers in minutes using basic business info and automated risk checks. This speeds up the sales cycle without heavy underwriting.

- Flexible Payment Terms: Lets buyers pay monthly or quarterly, or on extended net terms (up to 180 days), while sellers still receive the full contract value upfront.

- Upfront Payout to Sellers: Delivers most of the deal value within 1–2 business days after approval, improving liquidity and reducing reliance on discounts.

- Global Availability & Deal Flexibility: Supports deals from $2.5K to 7 figures across 9+ countries—serving both fast-moving SMBs and complex enterprise sales.

- Sales-Integrated Deal Management: Provides a unified view of financed deals, payment schedules, and buyer status for easier revenue tracking.

- Light White-Label Options: Offers branded financing flows, but with limited customization compared to fully white-labeled or embeddable buyer checkouts.

🔌 Integrations & Tech Stack Compatibility of Capchase

Capchase connects with common tools used by SaaS sales and finance teams.

- CRM: Salesforce, HubSpot

- Billing & Payments: Stripe, Chargebee, ACH, credit card, BACS, SEPA

- Accounting: QuickBooks, NetSuite, Xero.

🚀 Customer Success Story: Creyos

Healthcare tech company Creyos adopted Capchase Pay to offer flexible monthly and quarterly payment options to its customers—while still collecting the full Annual Contract Value upfront.

Results:

- 50% increase in average customer size

- Immediate access to full ACV upfront for reinvestment

- Reduced reliance on discounts to secure upfront payments

💰 Capchase’s Pricing

- Capchase charges a flat financing fee for each deal that uses their flexible payment method. You have flexibility in how this is covered, as the fee can be paid by the vendor, paid by the buyer, or split between both parties.

🗣️ Client testimonial

Here’s what one of the clients say:

🧪 Demo/Trial Availability

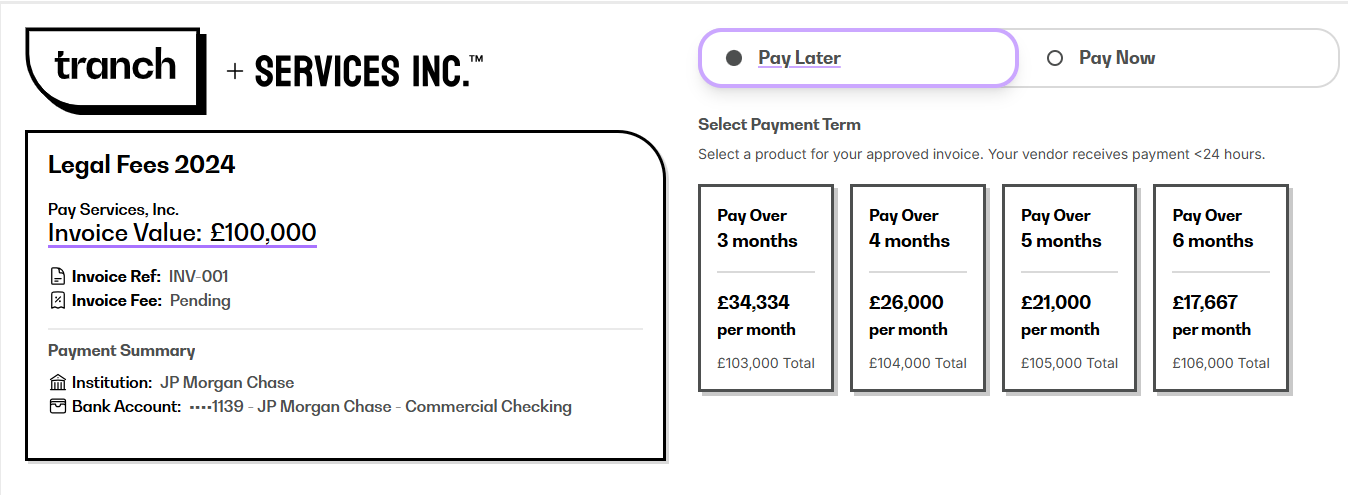

3. Tranch

Tranch is a B2B invoice-to-payments platform designed for enterprises to optimize cash flow by offering flexible, seamless payment experiences to their business clients.

As an Elite company, Tranch focuses on simplifying and accelerating accounts receivables, helping businesses get paid up to 40% faster while eliminating their credit risk

🛠️ Key BNPL Features & Benefits of Tranch

Here’s a closer look at what Tranch offers:

- Flexible Payment Options: Offer up to £500,000 in financing while getting paid upfront — clients pay on their terms.

- Zero Credit Risk: Tranch assumes full repayment risk, so you stay protected from client defaults.

- Fast Payouts: Receive funds within 24 hours of client approval to keep cash flow moving.

- Custom Payment Schedules: Clients choose 3–6 month plans with full cost transparency.

- Smart Credit Technology: Uses Open Banking and financial intelligence for fast, accurate underwriting.

- Recurring Payments Support: Perfect for SaaS — set up and automate subscription or retainer payments.

- AR Automation: Streamline collections and reconciliation with automated workflows.

🔌 Integrations & Tech Stack Compatibility of Tranch

- Supports ERP and accounting integrations via API or SFTP, secure BNPL links in invoices, and easy low-code/no-code deployment.

🚀 Customer Success Story: Gunderson Dettmer

A leading law firm, Gunderson Dettmer, used Tranch’s Pay Later and Pay Now options to modernize its client billing and reduce collection delays.

Results:

- Faster client payments and fewer manual collection efforts

- 25% reduction in invoice discounting

- Onboarded and live in under 48 hours

💰 Tranch’s Pricing

Tranch’s Pay Later product uses transparent, risk-based pricing with a flat fee of about 1% per month, and no subscription or hidden fees.

🗣️ Client Testimonial

Here’s what their clients say:

🧪 Demo/Trial Availability

- Quick demo booking via website

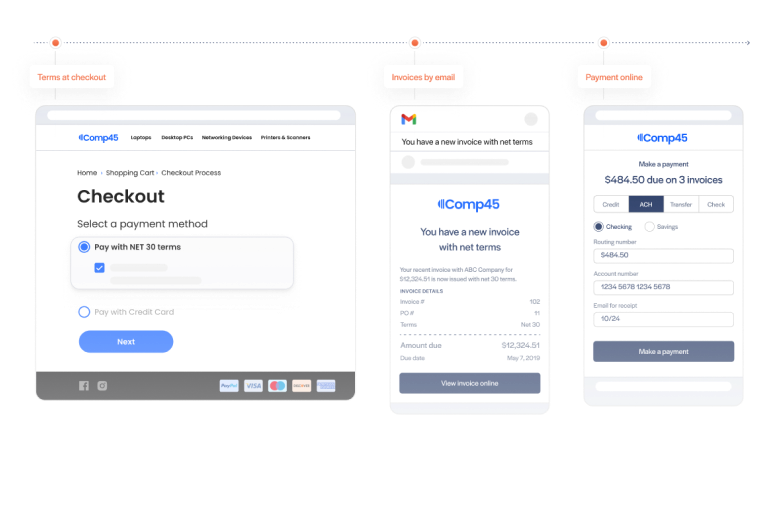

4. Resolve

Resolve is a B2B payments company that offers a B2B BNPL product designed to help businesses extend net payment terms such as Net 30, Net 60, or Net 90 while receiving payment on approved transactions.

The product allows sellers to offer flexible payment terms to buyers while Resolve manages credit checks, invoicing, and collections as part of the platform.

🛠️ Key BNPL Features & Benefits of Resolve

Here is a closer look at what Resolve B2B BNPL offers:

- Net Terms as a Service: Offer Net 30/60/90 terms to boost sales while helping buyers manage cash flow.

- Upfront Invoice Advances: Get paid immediately without waiting for term completion — improve working capital.

- Instant Credit Decisions: AI-driven credit checks enable fast buyer approvals and seamless onboarding.

- Agentic AR Automation & Collections: Eliminate manual AR tasks with end-to-end billing and payment management.

- Multiple Payment Methods: Let buyers pay via ACH, card, wire, or check through a branded, buyer-friendly portal.

🔌 Integrations & Tech Stack Compatibility of Resolve

Resolve syncs bi-directionally with your financial stack

- Accounting integrations: QuickBooks, Xero, NetSuite

- API support: REST APIs for custom platform embedding

- Checkout integration: SDKs and scripts to embed net terms at checkout

🚀 Customer Success Story: SDi Fire

SDi Fire, a global provider of industrial fire alarm testing equipment, partnered with Resolve to overcome cash flow challenges caused by extended payment terms and slow credit approvals.

Results:

- 25% increase in profit margins after adopting Resolve’s net terms solution

- Credit approvals reduced from weeks to hours using Resolve’s automated credit checks.

💰 Resolve’s Pricing

- Resolve charges a risk-based advance fee when a seller chooses to receive early payment on an invoice. The exact fee and advance amount depend on the transaction, and sellers can choose how much of the invoice value to advance..

🗣️ Client Testimonial

Here’s what their clients say:

🧪 Demo Availability

- Instant demo sign-up via website

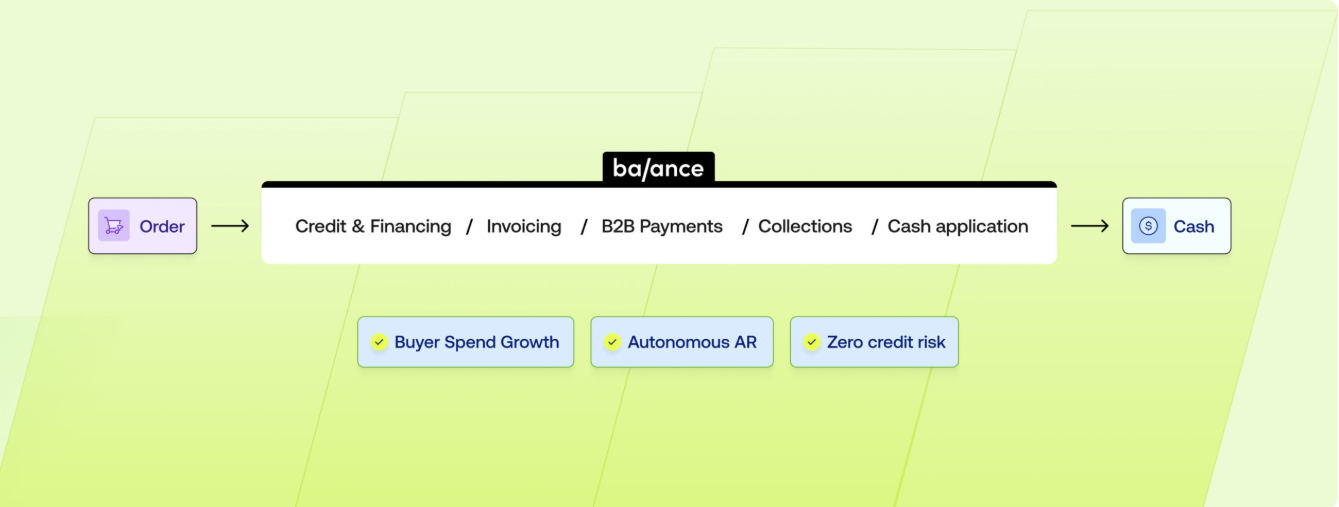

5. Balance

Balance is a digital B2B checkout and payments platform that brings eCommerce-grade UX to B2B transactions. Designed for marketplaces, platforms, and merchants, Balance offers BNPL, invoicing, and flexible terms, all via API or embedded UI.

🛠️ Key BNPL Features & Benefits of Balance

Here’s a closer look at what Balance offers:

- Instant B2B Financing at Checkout: Lets buyers access real-time financing online or in-store, reducing friction and boosting conversions.

- Full Upfront Payment for Sellers: Receive full payment immediately while buyers pay later (up to Net 90), improving cash flow and predictability.

- Zero Credit Risk: Balance assumes all credit risk, allowing you to offer flexible payment terms safely.

- AI-Powered Risk Infrastructure: Uses proprietary and bank data to approve more buyers instantly while maintaining portfolio quality.

- Dynamic Credit Limits: Adjusts buyer credit limits in real time based on purchasing behavior to drive larger and repeat transactions.

- Buyer Insights Dashboard: Gives visibility into transactions and repayment trends, helping identify new growth opportunities.

🔌 Integrations & Tech Stack Compatibility of Balance

- API-first setup for embedding buyer flows, billing, and credit tools

- No-code and prebuilt integrations with major B2B platforms

- ERP/accounting sync for streamlined reconciliation

- Checkout SDK for branded, embedded payment flows

- Commerce platform support: Shopify, Magento, BigCommerce, Mirakl, Adobe Commerce

🚀 Customer Success Story: PNOĒ

PNOĒ partnered with Balance to simplify hardware financing for gyms and health professionals, offering flexible payment options while maintaining cash flow.

Results:

- Reduced purchase friction and improved onboarding

- Boosted sales growth through easier financing options

💰 Balance’s Pricing

- Custom / Quote-Based Pricing: Pricing depends on transaction volume, payment methods, and financing terms, with enterprise merchants required to request a quote.

🗣️ Client Testimonial

Here’s what their clients say:

🧪 Demo/Trial Availability

- Businesses can request a personalized demo through the website.

After reviewing the leading BNPL providers, one thing becomes clear. Most aim to solve the same problem: helping SaaS companies offer flexible payment terms without hurting cash flow.

Where they differ is in how they solve it. Some focus mainly on invoice financing or payment advances.

Ratio, through its product Ratio Boost, approaches this differently. It connects proposals, payments, renewals, and collections in one workflow.

For SaaS teams that want payment flexibility without adding operational complexity, Ratio is one of the BNPL companies worth considering.

Let’s break down why more SaaS vendors are choosing Ratio.

💡Why SaaS Vendors Choose Ratio Over Other BNPL Companies as Their Growth Engine

For many SaaS companies, the hardest part of a deal isn’t getting the buyer to say yes.

It’s turning that yes into cash upfront. That is the closing motion.

DearDoc, a healthcare marketing platform, was facing exactly that challenge. Deals were often slowing down at the final stage because buyers needed flexible payment terms, while the company still needed predictable cash flow to fund growth.

Instead of relying on discounts or long payment cycles, DearDoc adopted Ratio Boost to offer flexible payment options while maintaining cash flow visibility.

🚀The result was simple: buyers gained flexibility, and the sales team could close deals without adding operational complexity.

Hear directly from Joe Brown, Founder & CEO of DearDoc, about how his team uses Ratio Boost.

💬 And here’s something many founders ask next:

🤔Does Ratio Boost Only Support SaaS? What About Agencies, Services, and Tech-Enabled Businesses?

While Ratio was built with SaaS in mind, it’s not limited to software companies. If your business runs on recurring revenue, Ratio fits right in.

It is even ideal for:

✅ Robotics-as-a-Service (RaaS): Perfect for robotics companies moving from one-time sales to subscription or usage-based pricing.

Just ask Sorting Robotics. After adopting Ratio, they started winning deals that previously stalled. As CEO Nohtal Partansky put it:

“Ratio fills a need in the Robotics-as-a-Service industry that no one else does. By providing flexibility to our customers, we’ve landed deals we would have lost to budget constraints.”

✅ Tech-Enabled Services: Companies delivering ongoing managed services, support, or maintenance plans.

✅ VARs Bundling Software + Hardware: If you resell equipment alongside software licenses, Ratio enables flexible financing without putting your cash flow at risk.

Across all these use cases, the story is the same: You get paid upfront. Buyers get flexibility. And your revenue becomes more predictable.

Now, if you are also running a similar business and want to stop chasing payments or discounting to close — Ratio could be exactly what your team needs.

👉 Book your personalized demo call today and see how Ratio can power your recurring revenue model.

Disclaimer: This comparison is based on publicly available information and product capabilities as of March 2026. Features, pricing, and functionality may vary depending on your use case, business model, and implementation. Readers should evaluate each billing solution based on their specific requirements and consult directly with vendors before making a final decision.

FAQs

1. What Minimum Contract Size or ACV Makes a BNPL Partner Viable for a SaaS Vendor?

A BNPL solution becomes viable when your average contract size is at least $3,000–$5,000 annually. It becomes high-impact at $10,000+ ACV.

Below that threshold, the transaction sizes often don’t justify the effort or cost of underwriting, and the benefits (like better conversion or reduced discounting) aren’t meaningful enough to offset platform or financing fees.

What also matters is deal volume. If you're closing dozens of mid-sized contracts monthly, even at lower ACVs, BNPL can still drive significant cash flow benefits and reduce working capital strain.

More importantly, if you're regularly offering discounts just to get annual upfront payments, you're already leaking revenue. That's where BNPL flips the equation: the customer pays monthly, but you collect the full contract value upfront.

2. How Can BNPL Help SaaS Vendors Close Deals Without Increasing Operational Friction for Finance or RevOps?

Modern BNPL platforms eliminate friction by embedding directly into your existing sales and finance workflows.

Your reps can offer flexible payment terms (e.g., monthly or quarterly) at the quoting stage, without involving finance, without creating custom contracts, and without AR needing to manage collections. You still collect the full contract value upfront — BNPL takes on the buyer risk and billing.

Because the buyer pays over time, objections around large upfront payments disappear. And because the BNPL is integrated into your CRM or CPQ, your RevOps and Finance teams don't need to change how they track or report revenue.

The result is higher close rates, reduced discounting, and faster cash collection — with no added overhead.

3. How Do I Evaluate Operational Readiness Before Launching BNPL?

You’re ready to launch BNPL if you meet three conditions:

- You regularly sell annual contracts over $5K ACV.

- You’re seeing discount pressure or delayed closes due to budget objections.

- You have basic sales and billing systems in place — like Salesforce, HubSpot, Stripe, Chargebee, or similar.

Even if you don't have CPQ in place, some BNPL providers (like Ratio) offer light-weight quoting and checkout tools that plug into your CRM or billing platform.

Where BNPL fails is when sellers try to force it into a low-ACV, high-velocity sales model without the infrastructure to support payment orchestration or customer lifecycle management.

If you want a checklist to evaluate readiness, this post breaks it down well: Flexible Financing Options for SaaS.

4. What Exit or Transition Risks Should I Consider If I Choose a BNPL Provider and Later Want to Switch or Stop Using Them?

The three biggest risks are:

- Receivables Control – If the BNPL provider owns the buyer contract, you won’t be able to directly re-engage those customers for collections or renewals if you part ways.

- Data Portability – Make sure you can export your deal, repayment, and customer records easily to avoid system lock-in.

- Customer Expectation Risk – Once buyers get used to payment flexibility, removing it may affect win rates or churn unless you have an alternative.

Look for BNPL providers that offer modular contracts (no long-term lock-ins), support CRM or billing system integrations, and keep you in control of the buyer relationship post-sale.

For a deeper breakdown of how to evaluate these risks, see: Avoid Common P itfalls in B2B Financing Partnerships.

.png)

.png)